Pavement Management - PowerPoint PPT Presentation

1 / 61

Title:

Pavement Management

Description:

STRAW POLL TO BE CONDUCTED AT 9:00 P.M. Questions: Please vote just once 1. Do you support the Town Manager s budget as proposed? Yes/No 2. Do you support ... – PowerPoint PPT presentation

Number of Views:27

Avg rating:3.0/5.0

Title: Pavement Management

1

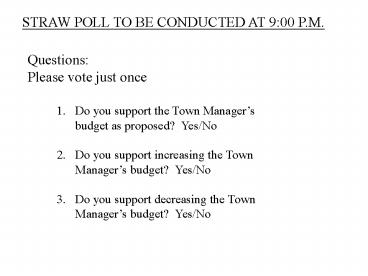

STRAW POLL TO BE CONDUCTED AT 900 P.M.

QuestionsPlease vote just once

1. Do you support the Town Managers budget as

proposed? Yes/No2. Do you support increasing

the Town Managers budget? Yes/No3. Do you

support decreasing the Town Managers budget?

Yes/No

2

TOWN OF TOLLAND

FY 2011-2012 BUDGET PRESENTATION As Proposed by

Town Manager, Steven R. Werbner March 29, 2011

3

BUDGET PROCESS

Development of the budget begins in October with

the preparation of the Board of Education request

and culminates in May with the Town Referendum.

Charter Mandated Process

Superintendent

Board of Education

Town Manager

Town Council

Voters

Referendum is May 3, 2011 and, if the budget is

defeated, votes are every two weeks until a

budget is passed.

4

Public Meetings to Date on Budget

Joint Meeting of Town Council/Board of Education

February 10, 2011Capital Budget Public

Hearing February 17, 2011Community

Conversation on Budget February 24, 2011Joint

Meeting of Town Council/Board of Education

March 8, 2011Budget Review Sessions with Town

Council March 17, 22 23, 2011Public Hearing

on Managers Proposed Budget March 29, 2011

Upcoming Meetings

Town Council finalizes Budget April 5,

2011Annual Budget Presentation Meeting April

26, 2011Budget Presentations at Senior Center

April 27, 2011 _at_ 1230 p.m. Budget

Referendum -- May 3, 2011

5

What is a Budget?

- A financial plan with sets of priorities and

direction that the Town Officials, Town Council

and residents believe accurately reflects the

most important needs of the Town operations.

- In terms of the Board of Education, the Town

Manager and Town Council, by State law, can only

determine a bottom line number. The

allocation of resources is the sole prerogative

of the Board of Education.

6

TOWN MANAGERS BUDGET GOAL FOR FY2011-12

Produce a budget that is realistic in light of

the economic times

THIS BUDGET WILL

Maintain important services

Continue to provide a quality education for our

children

Meet the budget objective of limiting an

increase in taxes to under 3.

7

INTRODUCTIONBUDGET PREMISE

- The premise from which I am working in preparing

this budget is as follows - The Town and Board of Education have legitimate

needs for which the associated cost exceeds our

ability to pay. - The Superintendent and Board of Education do an

excellent job in identifying their needs which

are incorporated into their budget request.? A

quality education is extremely important for this

generation and generations to come. - Town and Board of Education Services are of the

highest quality, yet our cost for such services

are in most cases lower than other comparable

municipalities.

8

? No one wants to see existing programs in

either the Town or Board of Education

eliminated. ? At the local level, REALITY is,

that the property tax will only absorb a limited

amount of the increase necessary to address our

legitimate needs. While some are in a position

to pay more in taxes, many are not. Therefore,

the full amount of expenditures requested from

Departments, including the Board of Education,

are in my opinion not affordable.

9

BUDGET PARAMETERS

How did I arrive at the financial plan I am

proposing?

- Analyzed revenues based on end of last year

results as well as the first six months of this

fiscal year. - Monitored actions taken at the State level to

reduce or at best keep municipal aid flat. - Established in November of 2010 budget

instructions for all departments with a goal of

limiting any tax increase to under 3.

10

BUDGET PARAMETERS (continued)

- Discussed in December of 2010 the budget

parameters I established with the Town Council. - In February of 2011 held a Community Conversation

on the status of revenues and budget parameters

to get public input. - Have continued to monitor local, State Federal

revenues and have continually tested my original

expenditure assumption against potential tax

impact.

Only after determining available resources do I

then establish what I believe to be appropriate

expenditure limits.

11

BUDGET PARAMETERS (continued)

- While approval of the final budget amount at

referendum is not the ultimate factor I use to

establish budget parameters, I feel it is my

Charter mandated responsibility to recommend a

budget to the Town Council which can be supported

from what I perceive to be a reasonable revenue

perspective.

12

LOCAL FINANCIAL CONCERNS GOING FORWARD

- Local government is limited by State law in

regard to its ability to raise funds. Therefore,

we are heavily dependent on property taxes and

State revenues as sources of revenue to fund

local programs.

- The level of State aid to municipalities is

insufficient to meet the growing cost to towns

and cities and places an unacceptable burden on

the local property tax, in particular education. - Local governments cannot continue to provide the

same or an improved level of service unless

property taxes increase for a sustained period of

time.

13

LOCAL FINANCIAL CONCERNS GOING FORWARD (continued)

- Senior citizens on fixed incomes and others in

lower income brackets are finding it difficult to

stay in their homes working people are

continuing to lose jobs government workers in

many communities including Tolland have in the

recent past accepted wage freezes and other

concessions to help reduce expenditures.

- The State of Connecticut continues to impose many

unfunded mandates on towns and boards of

educations. The Town of Bristol recently

calculated that they are spending over 14

million on unfunded or partial funded State

mandates.

14

The State of Connecticut is projected to continue

to have large deficits over the next several

years jeopardizing our level of State aid.

STATE OF CONNECTICUT BUDGET CONCERNS

- Future Projected Operating State Deficits

FY 2011/2012 FY 2012/2013 FY 2013/2014

3.3 Billion 3.1 Billion 3.1 Billion

Future Projected long-term State underfunded

obligations

Bonded Indebtedness 18.0 Billion

State Employee Pensions 9.3 Billion

Teacher Pensions 6.5 Billion

Post Retirement Benefits 26.8 Billion

GAAP Deficit 1.1 Billion

Total 61.7 Billion

15

STATE OF CONNECTICUTBUDGET CONCERNS (continued)

- It is interesting to note that the State is

projecting a positive balance at the end of this

fiscal year in the amount of 57.2 million, but

only as a result of one time windfalls from the

Federal Government and significant borrowing

authorized last year, use of all Rainy Day Funds

plus an additional charge levied on our electric

bills. - Without these one time sources of revenue

Connecticut would have had a 2 billion deficit

at the end of the current fiscal year. - The Governors budget going forward does not rely

on this one time source of revenue or borrowing

for operating expenses which necessitates either

increased taxes, decreased expenditures or a

combination of both.

16

- Impact of Governors Budget on Tolland

- Most Education and Non-Education grants were

funded at the same levels as in the current year.

ECS, our largest State grant for education is

currently budgeted at 10,759,283. State-wide

prior to 2009, this grant was increasing

approximately 5/year. For Tolland that was

approximately 400,000-500,000 additional

dollars annually. The grant has not increased

the past two years and will not increase for the

next two years. - Notable exceptions are Pilot Grant for

Manufacturing Machinery Equipment (MME). This

grant was eliminated State-wide. The loss of

revenue to the Town was estimated to be 80,000

for the next fiscal year. - Transportation Grant was reduced by 90,000.

- New forms of revenue recommended such as a

portion of increased sales tax based on retail

sales in the community, boat tax, tax on hotels,

car rentals, planes and tax on cabarets will have

only a minimal impact on Tolland.

17

Major Concern for the Future Status of ECS Grant

18

Town Revenues2011 - 2012

19

Changes in State Aid and Other Sources of

Revenue for the Next Fiscal Year Over Current

Year Revenues

- State Aid for Education

(104,253)

- ECS 0

- Public School Transportation (104,261)

- Adult Education

8 - Aid to the Blind (0)

- Municipal State and Federal Grants

(132,490)

20

Changes in State Aid and Other Sources of

Revenue for the Next Fiscal Year Over Current

Year Revenues

- Other Non-Tax Revenue

? Charges for current services 6,216 ?

License, Permits and Fees (46,000) ? Interest

and other revenues (30,855)

TOTAL DECREASE IN REVENUE (307,382)

21

Grand List Growth at 1.10

after adjustments for new

construction, elderly exemptions,

MVS and slight

decline in the mill rate and excluding the impact

of the State mandated revaluation 406,355

History of Grand List Growth Percentage

22

(No Transcript)

23

Fund Balance

An increase in the use of Fund Balance by 30,000

to a total of 230,000 is recommended to be used

as a revenue in these difficult economic

times. Rating agencies recommend that Fund

Balance percentage for towns with a AA credit

rating be in a range of 10-15 of operating

expenditures. This is not a revenue source

that should be relied upon in the future. This

is a one time use of funds that may not be able

to be duplicated in future years.

24

FUND BALANCE

2011 estimated 5,654,614 11.19

2010 5,884,614 11.60

2009 5,755,314 11.40

2008 5,175,165 10.9

2007 4,386,381 9.1

2006 4,336,381 9.7

2005 3,906,752 9.3

2004 3,516,564 9.0

2003 3,082,745 8.2

2002 2,521,653 7.0

2001 2,257,148 7.0

2000 2,164,504 7.2

25

With less revenue than the prior year and limited

grand list growth, there is little room for

growth in the budget unless property taxes are

increased.

26

(No Transcript)

27

Expenditures

28

EXPENDITURE SUMMARY

29

Magnitude of Recommended Expenditure Increases

- In the four years prior to FY2009/10 the Towns

average expenditure increase was 487,046. - In the same time period the Board of Educations

average expenditure increase was 1,428,309. - In the current year the Town reduced expenditures

from the prior year by 5,570 while the Board of

Education increased by 334,738. - For the next fiscal year my recommended budget

increases Town expenditures over the current year

by 210,460 while the Board of Education is

increased by 828,896. - Neither the Town or Board of Education can, in my

opinion, operate effectively in the next fiscal

year with an increase or lack thereof at the

levels of the last two fiscal years.

30

(No Transcript)

31

(No Transcript)

32

2011/2012 EXPENDITURES BUDGET 50,527,427

Capital

Municipal Operating

Debt Service

Education

10,832,492

34,637,431

4,751,796

305,708

33

Details of Town Expenditure Request

- Savings

- Negotiated changes to Town employees Health

Insurance Plans have mitigated increases in

health benefits. Whereas overall, health

benefits were calculated to increase 18, the

Towns costs actually decreased by 3.5 due to

the benefit changes. These changes saved the

Town 116,456. - Elimination of Refuse Recycling Coordinator

position for a savings of 25,750. These

responsibilities have been absorbed by the

Director of Administrative Services and other

staff. - Limited Adjustments

- 100 on-call stipend for Part-Time Animal Control

Officers (5,200 annually split by days of the

week worked). This is to recognize the two

part-time employees who must be on call on off

hours each day of the week. In addition, 5,000

for actual hours worked that are currently taken

from personnel contingency. - Administrative Secretary in Fire Department

increased from 35 to 40 hours to be in line with

the operation of the Fire Office (4,988 in

salary).

34

The position of Assistant Public Safety

Supervisor budgeted starting January 1, 2012 at a

cost of 39,444 with benefits for half a year.

During the current fiscal year, the consulting

firm of Field Services Inc. was engaged by the

Town of Tolland to perform a feasibility study of

the Tolland Fire Department and its ability to

provide the current level of service to the Town

in the coming years. The report stressed that

moving forward, the department focus should

primarily be personnel and staffing. Much focus

was placed on the Public Safety Supervisor

position which generally is considered a 40-50

hour position, but in reality works on a regular

basis in excess of 70 hours per week. The

demands of the position to supervise both paid

and volunteer staff are 24 hours a day. The

study concluded that there is considerable

concern that the Fire Chief may be

overstretched. The recommendation is to hire a

second in command who can mirror the

responsibilities of the Public Safety Supervisor

in terms of supervising staff and responding to

evening calls in a command capacity. In

addition, this position would serve as a Deputy

Fire Marshal and be in charge of the Towns

communication function. The Board of Directors

of the Tolland Fire Department Inc. concurs with

this recommendation and has stated The Board

heartily agrees with this conclusion. Volunteer

officers cannot be counted upon to reduce the

workload.

35

- Included within the Fire, Public Safety,

Emergency Management and Law Enforcement budgets

are the cost of the administrative functions

associated with the reverse 911 Everbridge

System. This will allow for telephone messages

to be sent to residents on general topics of

importance (4,050). - Adjust the pay grade level for the position of

Public Safety Supervisor and Public Works

Operations Manager by one grade and increase the

base salary of each position by 5,000 to reflect

increased responsibilities and work levels as

well as hours worked at a cost of 9,000 (partial

offset by State Grant). - Implementation of a Health Wellness Initiative at

a cost of 7,000 paid out of funds available in

the Health Insurance account in the current year.

Industry experts predict that the Town should

see reductions in future health insurance

expenditures at a rate of 3-5 times the

investment made in the Wellness Program. - Increase the cost share for Health Insurance,

which unaffiliated employees of the Town will

pay, from 14 to 16, except for those employees

who participate in the Health Wellness

Initiatives which would reduce the increase by

1.

36

- Re-title the positions of Working Foreman in the

Parks Facilities Department and Highway

Superintendent in the Highway Department to

Public Works Supervisor. Along with the Public

Works Operations Manager, these two supervisory

positions provide oversight and direction for all

Parks and Highway activities. The initial cost

for this reclassification will be an increase of

3,000 to the Working Foreman position however,

there will be a future savings of approximately

15,000 with the adjustment of the Highway

Superintendents position to a lower wage group

when the current employee retires. - 27,000 for the connection fee to tie the Hicks

Municipal Building into the Towns public sewer

system. - The Water Commission and Water Pollution Control

Authority have each authorized the allocation of

15,000 from their funds to hire a 24 hour per

week, non-benefitted Engineering Assistant

position to assist with the many technical

responsibilities confronting the Commission.

This position would work under the direction of

the Town Engineer. - A 38,103 increase in the contractual cost for

Resident State Trooper services.

37

Savings identified total 142,206. The cost for

new items listed is 135,785. Therefore, the

total savings to the Town is 6,421.

38

Board of Education Request

- Board of Education request is reduced from 6.53

to 2.45, which is a reduction of 1,328,676, but

an increase of 828,896 over current year

expenditures. - When factoring in the Board of Education portion

of debt service, the Board of Education-related

expenditures are 71 of the overall Town budget.

39

Basis for BOE Funding Recommendation

- Savings

- 95,060 can be saved based on excess funding of

our OPEB Trust Account. - 90,000 can be saved based on a direct payment in

the same amount which will be made by the State

Department of Education to the Board of Education

for special education expenses. - It is apparent that one could divide the Board of

Education percentage request into two major

components. - Major Cost Components

- Operational Costs Employee Medical

Benefits - The percentage increase requested for operational

expenses is 2.36 after factoring in the

adjustments mentioned previously. My recommended

budget increase for the Board of Education is

2.45, which provides for the full cost of these

expenses.

40

Basis for Recommendation

- The original percentage increase requested for

Employee Medical Benefits is 3.6. This amount

has been reduced by 125,000 based on a reduction

in health insurance premiums from 22 to 18.66.

The remaining 1,095,525 increase cost could be

absorbed without an increase in the health

insurance line item if the vast majority of

teachers and administrators elected the option

currently existing in their contract to move from

their current health insurance plan to a high

deductible (HSA) plan. - A similar HSA plan is currently the only option

for Town Hall, Fire Department and several

non-union employees of the Board of Education. - HSA plans in the future may not be the ultimate

answer to addressing health care inflation, but

currently it is our only option. - The Town and Board of Education are investigating

health insurance pooling and wellness programs as

the primary means of reducing future medical

costs. Such costs statewide are projected to

increase in the 8-10 range for the foreseeable

future.

41

WHAT IS AN HSA? A high deductible Health

Insurance Plan with Health Savings Account

(HDHP/HSA) The first 1,500 for an individual

or 3,000 for a family in medical expenses is

paid for by the employee via a deductible. Once

deductible has been met, coverage is then paid in

full in accordance with plan provisions. Contribu

tions are put into a Health Savings Account

pretax which remains with the employee for life

to be used for eligible expenses and can be

carried over year to year. To encourage

employees to enroll in the Plan, the Town and

non-unionized BOE employees initially have the

deductible subsidized by the employer in the

amount of 75. Therefore the employees cost for

the deductible are 375 for an individual or 750

for a family. The amount of any subsidy is a

negotiable item.

42

The benefits of the HDHP/HSA plan are the same as

the traditional Town Point of Service plan with

the same network for physicians. Example of

POTENTIAL cost savings Expected premium cost

for typical BOE family plan 26,892 per

year. Expected premium cost for HSA plan based

on Town family plan 16,152 per

year. Difference is 10,740 per year, per

person.

43

In the BOE budget there are 308 certified

employees out of a total of 382 employees. If

252 or 81 certified employees chose this option

the approximate savings would be as

follows Cost for current plan -

5,062,462 Cost for HSA plan -

2,964,930 Difference -

2,097,532 Cost for BOE covering 75 of high

deductible assuming 252 BOE employees -

473,625. You must subtract the 473,625 from

the 2,097,532 as well as 20 for employee

contributions (418,706) resulting in a total

potential savings of 1,205,201 to the BOE.

44

WHAT DOES THE EMPLOYEE GET OUT OF THIS? They

pay their cost share amount on a lower premium

base Assume a 20 cost share for employees on an

HSA base vs. traditional plan. Savings to the

employee is 2,148 per year for a family plan.

Employees are responsible for the 750 of the

deductible which must come off the 2,148 cost

share savings for a total savings of 1,398 per

year. Summary The potential is for a million

dollar plus savings in health insurance expenses

for the BOE. Employees could save some 1,398

per year in addition to having the BOE put 2,250

into their health savings account. This could be

a win-win situation under present pricing

scenarios for all involved without significantly

impacting the health insurance coverage for BOE

employees.

45

POSSIBLE FUTURE BOE FUNDING CONCERNS

- Elimination of the BOE Federal Jobs Grant which

provided approximately 600,000 over two years. - Any jobs covered under the grant will have to be

absorbed with local funds or lost. - Teachers salaries will have to be budgeted at

contract rates for FY-2012 and FY-2013. - Health Insurance rates may increase at a rate of

8-10. - Fuel costs may continue to escalate.

46

Towns Commitment to Education

The Town has a strong ongoing Commitment to

Education 68.55 of every tax dollar spent goes

toward funding education. More of our limited

dollars are each year spent for education.

47

? The Town since 1998 has committed substantial

capital dollars to school improvements. Debt

service for the next year is 4,751,796 of which

71 is for schools, particularly the addition to

Birch Grove School and the new High School. This

cost is not included as part of the Education

budget.

- The Town spends approximately 300,000 per year

in staff salaries and materials to maintain all

outside grounds of Board of Education facilities

as well as snow removal services for Board of

Education parking lots. This cost, as well as

any yearly increases is not included in the

Education budget, but rather the Towns Parks

Department.

48

(No Transcript)

49

FY11-12 SIGNIFICANT CAPITAL PROJECTSFUNDED BY

THE GENERAL FUNDTotal Amount 305,708

- Town Administration

- Reserve for current year depreciation for

municipal vehicle replacement - 21,789.

- Board of Education Tolland Intermediate

School

- Sidewalk Paving - 15,000.

- Skylight Replacement - 26,000.

50

FY11-12 SIGNIFICANT CAPITAL PROJECTSFUNDED BY

THE GENERAL FUNDTotal Amount 305,708

- Capital Equipment

- Dump Truck 36 Replacement Parks Facilities

replacement of 1992 one ton Dodge dump truck with

a new one ton truck with plow and all season body

-76,819.

- Fire Department

- 7th and last payment for replacement of Engine

340 - 70,000.

51

FY11-12 SIGNIFICANT CAPITAL PROJECTSFUNDED BY

THE GENERAL FUNDTotal Amount 305,708

- Public Facilities

- Upgrade of Base Station Repeaters located at

Highway, Parks Facilities and the Tower Site

are mandated by FCC to be licensed and operating

in narrowband emissions before 1/1/13 - 20,000

second of three payments. - One additional gas pump and flow fuel part for

recently installed above ground fuel tanks at the

Highway Garage plus removal of the old tank -

25,500.

52

FY11-12 SIGNIFICANT CAPITAL PROJECTSFUNDED BY

THE GENERAL FUNDTotal Amount 305,708

- Drainage

- Infrastructure Drainage designs for Weigold Road,

Baxter Street and Sugar Hill Road systems -

50,600.

53

TOLLAND DEBT SCHEDULE 2011-12 THROUGH 2015-16

change FY11/12 - 4,751,296 1.87

FY12/13 - 4,797,741 .97 FY13/14 -

4,724,537 (1.53) FY14/15

- 4,676,459 (1.02) FY15/16

- 4,691,778 (0.33)

Both Moodys Fitch Financial rating agencies

have indicated thatthe Towns debt is moderate

and manageable and in line with Communities that

have similar credit ratings.

54

DEBT SERVICE FOR BUDGET YEAR 4,751,796

Debt Service Breakdown

29

71

55

MILL RATE IMPACT OF THE FINANCIAL PLAN

Mill rate 29.99 An increase of 0.84 mills

compared to the current mill rate of 29.15.

56

TAX IMPACT

Property Tax Impact of the Town Managers Recommended Budget for Three Average Assessments Property Tax Impact of the Town Managers Recommended Budget for Three Average Assessments Property Tax Impact of the Town Managers Recommended Budget for Three Average Assessments Property Tax Impact of the Town Managers Recommended Budget for Three Average Assessments Property Tax Impact of the Town Managers Recommended Budget for Three Average Assessments

2009 Assessment Equivalent Value Taxes at 29.15 Taxes at 29.99 Difference

121,972 174,246 3,555 3,658 103

196,130 280,186 5,717 5,882 165

375,384 536,262 10,942 11,258 316

Formula to determine tax impactCurrent

assessment x current year mill rate

(29.15) Compared against Current assessment x

Town Managers proposed mill rate

(29.99) Difference equals tax impact

57

APPROVED TAX INCREASE/DECREASE OVER THE PAST 6

YEARS FOR THE AVERAGE RESIDENTIAL HOME

58

CONCLUSIONSustainability is the key to any

financial plan Can the investments we make

today be sustained over time knowing what we know

about the current and upcoming financial

concerns? It is not just I can absorb a tax

increase this year to improve a desired program,

it is can you absorb a tax increase, in an

increasing amount, over a prolonged period of

time, to maintain/improve a program? That is the

budget realities of our economic times, made only

more of a reality by current actions at the State

and Federal levels.

59

(No Transcript)

60

Budget Schedule Important Upcoming Dates

61

(No Transcript)