IDAHO DEPARTMENT OF EDUCATION Public School Finance - PowerPoint PPT Presentation

1 / 61

Title:

IDAHO DEPARTMENT OF EDUCATION Public School Finance

Description:

IDAHO DEPARTMENT OF EDUCATION. Public School Finance. Contacts: Tim Hill, Deputy Superintendent 332 ... Greg Berg, Coordinator 332-6840 GDBerg_at_sde.idaho.gov ... – PowerPoint PPT presentation

Number of Views:48

Avg rating:3.0/5.0

Title: IDAHO DEPARTMENT OF EDUCATION Public School Finance

1

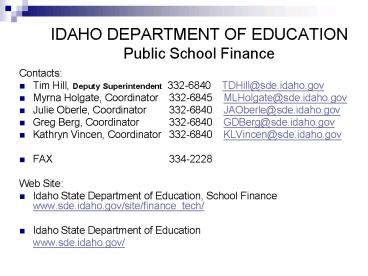

IDAHO DEPARTMENT OF EDUCATIONPublic School

Finance

- Contacts

- Tim Hill, Deputy Superintendent 332-6840

TDHill_at_sde.idaho.gov - Myrna Holgate, Coordinator 332-6845

MLHolgate_at_sde.idaho.gov - Julie Oberle, Coordinator 332-6840

JAOberle_at_sde.idaho.gov - Greg Berg, Coordinator 332-6840

GDBerg_at_sde.idaho.gov - Kathryn Vincen, Coordinator 332-6840

KLVincen_at_sde.idaho.gov - FAX 334-2228

- Web Site

- Idaho State Department of Education, School

Finance www.sde.idaho.gov/site/finance_tech/ - Idaho State Department of Education

- www.sde.idaho.gov/

2

Public School Finance

- IFARMS

- Other State Funding on Line 6 of the Foundation

Program Calculation Worksheet - Indirect Costs

- Tuition Rates

- Calendars (separate presentation)

- School Facility Maintenance (separate

presentation)

3

IFARMS

- Idaho Financial Accounting Reporting Management

System (IFARMS) - IFARMS Annual Report is a summary of the

financial activity (revenue and expenditure) by

fund for each district and charter school

statewide - IFARMS Manual is available on the School Finance

website under FORMS

4

IFARMScontinued

- IFARMS Annual Financial Report

- Forms sent electronically to districts and

charters in April / May - Documents will be available online in April

- Memos

- Annual Report Forms, with and without totals

- Balance Sheet Codes, Revenue Codes, and Fund

Number/Function Program/Object Codes - (Once on the School Finance website, click on the

Forms link on the far left side of the webpage.)

5

IFARMScontinued

- IFARMS Annual Financial Report

- Report due to School Finance by October 31st

- Report can be submitted electronically (cd,

diskette, email) or on paper

6

IFARMScontinued

- General Fund Revenue / Expenditures

- GF enhancements often reported as state special

projects - Idaho Reading Initiative

- Limited English Proficiency

- National Board Certified Incentives

- Gifted Talented

- Will recode as General Fund activity

7

(No Transcript)

8

IFARMScontinued

- General Fixed Assets

- Report on page 100 of the Annual Financial Report

at their historical cost - If your capital outlay thresholds differ between

the district records and audit report, use the

lower threshold when reporting amounts on page

100 - If possible, report amounts separately for

elementary, secondary, administrative, and other - Data used in the calculation of tuition rates

9

IFARMScontinued

- Before submitting your annual report

- Reconcile your annual and audit reports prior to

submitting - Compare beginning and ending fund balances by

fund - Compare revenues and expenditures by fund

- Compare balance sheet information by fund

- Reasonableness check

10

IFARMScontinued

- Audit report is currently due by November 10th

per Idaho Code 33-701(6) - November 15th payment may be delayed if audit

report not received by due date

11

IFARMScontinued

- Once we have the annual and audit reports, we

- Enter the data into our database

- Compare the IFARMS annual report balance sheet,

revenue, expenditure, and fund balance data to

the audit report data by fund - If there are differences, we call for an

explanation

12

IFARMScontinued

- Once a districts financial data has been

reconciled, we generate the yellow page - A copy of the yellow page is sent to each

district for review - The yellow page is included in the Financial

Summaries report available on our website

13

Example of a Yellow Page

14

IFARMScontinued

- Financial data from the districts

- Generates the Financial Summaries

- Included in the School Profiles Report

- Used to complete federal surveys

- Ranks Idahos educational spending as compared to

other states - Allocates Title I dollars to the State of Idaho

15

IFARMScontinued

- Financial data from the districts, continued

- Basis for determining in-state and out-of-state

tuition rates - Used in the calculation of several of the tuition

equivalencies - Used by SDEs Special Education and Child

Nutrition divisions - Basis for calculating Indirect Cost Rates

- Basis for determining maintenance of effort

- Lots of public inquiries

16

IFARMScontinued

- It is very important you use the correct fund

numbers, revenue codes, and function/program

codes when recording your financial activity - Call if you are unsure how to code a transaction

17

IFARMSconcluded

- Questions?

18

Line 6 of the Foundation Program Calculation

Worksheet

19

Line 6 Funding May Include

- District to Agency Contracts

- Special Education Tuition Equivalency

- Court-Ordered Tuition Equivalency

- Juvenile Detention Center Tuition Equivalency

- Summer Juvenile Detention Center Tuition

Equivalency - Serious Emotional Disturbance (SED) Allowance

20

District to Agency Contracts

- Idaho Code 33-2004

- Received when a district contracts with a public

or private agency to educate exceptional students - Payment

- Best 28 Weeks ADA

- x Prior Year Per Pupil State Support

- District to Agency Contract Reimbursement

21

District to Agency Contractscontinued

- Prior Year Per Pupil State Support

- (Prior Year Base Support Prior Year Benefit

Apportionment) / Best 28 Weeks ADA - Initially paid with the February 15th payment and

final payment is made July 15th - Nine districts were paid 123,640 on 2/15/09

- In FY 2008, 219,608.48 was paid to 11 districts

22

District to Agency Contractscontinued

- So you have qualifying kids, now what?

- Contact the SDE Special Education Bureau (Lester

Wyer, 332-6916) - Specific forms must be completed (available

online) - Special Education Bureau reviews the forms and

forwards the necessary data to School Finance - School Finance receives a list of districts, the

educating agency, and the number of students - School Finance pulls the attendance data needed

from the attendance forms submitted each period

23

Exceptional Child Tuition Equivalency

- Idaho Code 33-1002B(3)

- Received when a district is educating a student

who - 1) is on the 12/1 Special Education child count

- 2) resides in a licensed facility due to the

nature and severity of the disability and - 3) whose parents live in another Idaho district

24

Exceptional Child Tuition Equivalency continued

- Payment

- Number of Qualifying Students from the 12/1

Child Count - x (42 of Prior Years Gross Annual Tuition Rate

Prior Year Excess Cost Rate) - Exceptional Child Tuition Equivalency

- Paid with the February 15th payment

- 19 districts were paid 1,292,453 on 2/15/09 11

districts received 993,058 in FY 2008 22

districts received 1,418,512 in FY 2007

25

Exceptional Child Tuition Equivalency continued

- So you have qualifying kids, now what?

- Work with SDEs Special Education Bureau (Lester

Wyer, 332-6916) - Special Ed has an application available online

that must be completed (students are listed

individually) - Special Ed reviews the application and verifies

that students listed are on the 12/1 child count - School Finance receives a summarized list of

districts and the number of qualifying students

26

Excess Cost Rates

- Determined annually using Special Education

expenditure information taken from the annual

financial reports and the 12/1 child count - 2007-2008 Excess Cost Rate 7,401

- 2006-2007 Excess Cost Rate 6,853

- 2005-2006 Excess Cost Rate 6,437

- 2004-2005 Excess Cost Rate 6,124

- 2003-2004 Excess Cost Rate 5,612

27

CourtOrdered Tuition Equivalency

- Idaho Code 33-1002B(1)

- Received when a district educates students placed

into a licensed home or facility by an Idaho

court-order - Beginning with the 2001-2002 school year, Idaho

Code was amended to include licensed homes, which

includes foster homes - 1,100,842 paid to 51 districts in FY 2008

1,213,994 paid to 45 districts in FY 2007 and

1,229,003 paid to 48 districts in FY 2006

28

Court-Ordered Tuition Equivalencycontinued

- To receive payment, a district must submit the

court-ordered tuition equivalency form - The form will be emailed to districts in April

- The form should be returned AFTER the last day of

school or after the eligible child(ren) is no

longer living in the licensed home or facility - Forms returned prior to the last day of school

showing perfect attendance through the end of the

school year will be returned

29

Court-Ordered Tuition Equivalency continued

- The form must include the number of days present

for each student, their grade level, and the name

of the home or facility - Talk to your school counselors

- Contact your regional Health and Welfare office

- Paid with the July 15th payment

- Funding is in addition to the regular

support-unit funding for these students

30

Court-Ordered Tuition Equivalency continued

- When contacting your regional Health and Welfare

office - DO NOT wait until the end of the school year to

contact HW and expect an immediate reply - Be specific in your request (names, dates)

- HW needs time to compile the listing of students

- Once you receive the listing, you need to

determine - Was the student attending school in your

district? - If the student was attending in your district,

how many days of attendance did that student have

for the school year while in foster care

31

(No Transcript)

32

Court-Ordered Tuition Equivalencycontinued

- Once School Finance has received the completed

form, we - Calculate the total days of attendance for

elementary students - Calculate the total days of attendance for

secondary students - Multiply the total number of attendance days by

the applicable elementary or secondary prior

years daily tuition rate - Daily rate 42 of the gross monthly tuition

rate divided by 20 days

33

Juvenile Detention Center Tuition Equivalency

- Idaho Code 33-1002B(2)

- Received when a district educates students placed

into a juvenile detention facility by an Idaho

court-order - To claim the equivalency, submit the long-form

attendance report along with the other

attendance reports due that period - Calculation is very similar to the Court-Ordered

Tuition Equivalency calculation - 581,403 paid for the 2007-2008 school year,

68,202 paid for the 2008 summer session

34

Juvenile Detention Center Tuition

Equivalencycontinued

- Payment

- -Regular Juvenile Detention Center Tuition

Equiv. - Multiply the total number of days by

42 of the prior years gross monthly tuition

rate (elementary or secondary) / by 20 days - -Summer Juvenile Detention Center Tuition

Equiv. - Multiply the total number of days by ½

of 42 of the prior years gross monthly tuition

rate (elementary or secondary) / by 20 days - Regular Tuition Equivalency paid with the July

15th payment - Summer Tuition Equivalency paid with the February

15th payment

35

Serious Emotional Disturbance (SED) Allowance

- Idaho Code 33-2005

- Received when a district is educating a higher

than average percentage of SED students - To receive a SED payment, a district needs only

to submit an accurate 12/1 child count to the

Special Education Bureau (Lester Wyer)

36

Serious Emotional Disturbance (SED)

Allowancecontinued

- Special Ed determines the statewide SED

- Total SED students statewide (from the 12/1

child count) / Total statewide enrollment SED - Special Ed then multiplies that by the

districts enrollment to determine the expected

number of SED students for that district - If the actual number of SED students at the

district is higher than the expected number of

SED students, the excess is multiplied by the

prior years excess cost rate - 36 districts received 2,562,597 on 2/15/09 40

districts received 2,204,819 in FY 2008 35

districts received 1,971,010 in FY 2007 and 29

districts received 1,841,853 in FY 2006

37

Serious Emotional Disturbance (SED)

Allowancecontinued

38

Other State FundingConcluded

- Questions?

39

Other Indirect Costs

- An indirect cost rate is a reasonable means of

determining the of allowable general

administrative expense that each federal grant

should cover - Now issuing 2009-2010 indirect cost rates to

those schools requesting the rate - An indirect cost rate is the ratio of total

indirect costs to total direct costs, based on

actual expenditures, exclusive of items such as

capital outlay and debt service - A manual is available on our website under Forms

at www.sde.idaho.gov/site/finance_tech/forms.htm

40

Other Tuition Rates

- We will be calculating 2009-2010 rates in the

next few weeks using 2007-2008 financial data - Idaho Code 33-1405 requires a district to charge

out-of-state student tuition to those students

whose home district is outside of Idaho - Can request a waiver from the State Board of

Education for any portion of the tuition rate - Waiver must be submitted before April 1

41

CALENDARS

- Required by Idaho Code 33-512

- Due to School Finance by May 15th for the

2009-2010 school year - 2009-2010 calendar forms and a Calendar Manual

are available on our website at

www.sde.idaho.gov/financeandtechnology/forms.asp - Forms were emailed to Superintendents on January

26, 2009 - Include a copy of the school calendar given to

patrons - Call 332-6840 with any questions

42

Minimum Instructional Hours asRequired by Idaho

Code 33-512

- Grades 9-12 - 990 instructional hours

- Grades 4-8 - 900 instructional hours

- Grades 1-3 - 810 instructional hours

- Kindergarten - 450 instructional hours

43

Instructional Hours May Be Reduced For Staff

Development

- Up to 22 hours for actual qualified staff

development activities (11 hours for

kindergarten) - Staff development is time set aside for the

training of teachers to allow for the development

of teaching skills - Teacher prep days, work days, parent teacher

conferences, and mentor time are examples of

activities not considered to be staff development

activities - Staff development hours are not limited to the

length of the normal school day and may occur

prior to the first day and after the last day of

school for students - You can have as many staff development hours as

you want, but only 22 hours count as

instructional time

44

Instructional Hours May be Reduced for Emergency

Closures

- Up to a total of 11 hours for emergency school

closures due to adverse weather conditions and

facility failures - For instructional hour purposes only, a closure

due to widespread sickness is not a qualified

emergency closure

45

Instructional Hours may be reduced for Grade 12

Students

- Up to 11 hours for grade 12 students ONLY

- Many districts end the school year earlier for

grade 12 students - If your district elects to reduce the amount of

instructional time for grade 12 students, a

separate calendar must be completed for grade 12 - A calendar for grades 9-12 as well as a calendar

specifically for grade 12 students is included in

the packet of calendars emailed to your district

46

(No Transcript)

47

(No Transcript)

48

(No Transcript)

49

When Planning a Shortened Session

- For Calendar purposes, ANY day shorter than your

regular day of instruction is considered a

shortened session and should be marked on your

calendar with a circle - All shortened days should be listed in the grid

at the bottom of the calendar

50

When Planning a Shortened Session continued

- For Attendance reporting purposes, a full day of

attendance (1.0 ADA) is reported for students

under instruction at least 4.0 hours (excluding

recess, passing time, breaks, lunch, etc) - For Attendance reporting purposes, a half-day of

attendance (.5 ADA) is reported for students

under instruction at least 2.5 hours but less

than 4.0 hours - For Attendance reporting purposes, kindergarten

cannot have half-sessions of attendance the

students are either under instruction a minimum

of 2.5 hours or they are not counted in ADA

51

When Planning a Shortened Session continued

- To maximize ADA, a district might want to keep

instructional time for shortened sessions to at

least 4.0 hours for grades 1 12 students and

2.5 hours for kindergarteners - Bussing schedules and other issues may preclude

this from occurring - Any day with less than 2.5 hours of instruction

will still be counted towards the minimum

instructional hours required, but no attendance

would be reported for that day

52

Calendars

- Notify School Finance of any changes made to your

calendar during the school year - Submit the Certificate of Closure with your

attendance reports for any emergency closures you

had during that attendance period along with a

copy of your board minutes authorizing the

emergency closure - Please call with any questions you may have when

completing the calendars

53

School Facility Maintenance and Repairs

- Idaho Code 33-1019

54

Idaho Code 33-1019 - Allocation for School

Building Maintenance (HB 743)

- Must allocate or spend at least 2 of the

replacement value of student-occupied buildings

for qualifying maintenance and repairs - Replacement value square footage of

student-occupied school buildings x 81.45

replacement value (for FY 2009)

55

Idaho Code 33-1019 - Allocation for School

Building Maintenance (HB 743)

- Square footage information collected each summer

for the upcoming school year - Exclude the square footage of student-occupied

buildings less than one year old on the first day

of school - Square footage needed to calculate the state

match - If the full 2 allocation is not spent, the

unspent dollars must be reserved for future years - Excess expenditures may be carried forward in

certain circumstances

56

Coding of Expenditures

- Qualifying expenditures may be coded to any

governmental fund using Function Codes 664 810 - Function Code 664 Maintenance Student

Occupied Buildings - Function Code 810 Capital Assets Student

Occupied Buildings (Qualifying Expenditures) - Non-qualifying repairs and maintenance

expenditures and non-qualifying capital asset

activities should be coded using Function Codes

663 811 - Function Code 663 - Maintenance Non-Student

Occupied - Function Code 811 Capital Assets Non-Student

Occupied ( Stud. Occ. Non-Qualifying

Expenditures)

57

Maintenance and/or Repairs for Serious or

Imminent Safety Hazards on the Property

- Maintenance and/or repairs outside the building

must be formally declared serious or imminent

safety hazards (Idaho Code 39-8004) by the

Division of Building Safety to be qualifying

expenditures - Think you have a serious or imminent safety

hazard? Call the Division of Building Safety at

334-3950

58

Excess Expenditures

- Expenditures exceeding twice your required

allocation (4 floor) may be carried forward

for up to 15 years to reduce future year

allocations - Expenditures greater than the required allocation

but less than twice your required allocation may

be used to reduce prior year unexpended

allocations carried forward

59

School Building Maintenance Report

- Due December 1

- Requesting the due date be changed to later in

December or early January - Must include

- Square footage of student-occupied school

building floor space - The funds and fund sources allocated for school

building maintenance and any unexpended

allocations carried forward from prior fiscal

years - Projects on which moneys were expended, including

the amounts and categories - The planned uses of the next years school

building maintenance allocation

60

In Summary

- You must allocate (not deposit) an amount equal

to 2 of the replacement value of school

buildings for qualifying school maintenance and

repairs - If qualifying school maintenance and repair

expenditures dont equal the 2 replacement value

of school buildings, the difference must remain

allocated for the purposes of IC 33-1019(3) - Consider using Fund 240 or Fund 430 to

carry-forward unspent maintenance dollars

61

(No Transcript)