Canadian Debt Markets - PowerPoint PPT Presentation

1 / 25

Title: Canadian Debt Markets

1

- Canadian Debt Markets

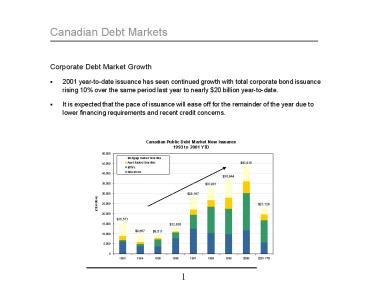

- Corporate Debt Market Growth

- 2001 year-to-date issuance has seen continued

growth with total corporate bond issuance rising

10 over the same period last year to nearly 20

billion year-to-date. - It is expected that the pace of issuance will

ease off for the remainder of the year due to

lower financing requirements and recent credit

concerns.

2

- Canadian Debt Markets

- Corporate Debt Market Trends

- The corporate sector is becoming increasingly

important in the benchmark index, now

constituting 25 of the index vs. only 10 in the

late 1980s. - Corporate issuance has grown at an annual rate of

25 since 1993. - Growth in Canadian corporate issuance this year

has not kept pace with the doubling of U.S.

corporate issuance this year the greater pace of

which has been due partly to refinancings of

early redemptions. - Corporate BBB securities are becoming an

important part of the Canadian bond market. - Increased corporate issuance is not only a

function of decreased government issuance, but

due to an increased demand for spread product by

institutional money managers as we look for new

ways to add value.

3

- Canadian Debt Markets

- Debt Market Trends

- New issue trends in 2001 in the Canadian market

include - Continued emphasis on infrastructure issuers,

totalling 1.7 billion so far this year,

including 3 issues by GTAA. - Continued issuance of Bank Tier II innovative

capital securities, i.e. BaTS, CaTS, BoaTS, etc. - 800 million BMO BoaTS issued this year

- First bond issue by a Canadian university

- University of Toronto 160 million 30-year bullet

bond at spread of 27 bps over Ontario (65 over

Canadas), higher rated than the province. - Anticipating additional 140 million from UofT,

and new issues from other universities including

UBC. - Introduction of CMBs by CMHC

- Canadian Mortgage bonds 2.2 billion 5 year

bullet bond backed by pool of NHA insured

mortgages - Spread at issue was 16 bps, compared to 15 bps

for CMHC credit, which had widened from 7 bps

before the new issue was announced, and MBS at 33

which tightened from 38 before the announcement.

4

Canadian Debt Markets

- BBB issues are 17 of all new corporate issues

so far in 2001, continuing the development of

this market in Canada - but the Canadian market remains dominated by A

rated issuers.

5

Canadian Debt Markets

- The Canadian corporate market continues to be

dominated by bank and other financial issuers,

but infrastructure continues to grow in the

Canadian market. - Banks issued 3 billion, or 18 of all new

corporate issues so far in 2001, including 800

million in hybrid securities.

6

- Canadian Debt Markets

- Corporate Debt Market New Issues 2001

7

- Canadian Debt Markets

- Corporate Debt Market New Issues 2001

8

- Canadian Debt Markets

- Credit Spreads

- Global credit concerns have resulted in a general

upward trend in Canadian credit spreads, nearing

3-year highs (spreads generally widened an

additional 10-15 bps after the events of

September 11 and are likely to continue to face

widening pressure in the face of continued

uncertainty) - This trend had been less severe for

infrastructure, insurance, and banks until the

recent tragic events.

9

- Canadian Debt Markets

- Corporate Liquidity

- Institutional investors desire greater liquidity

from corporate issues as they become a greater

part of the portfolio. - Average new issue size this year is 303 million,

compared to 210 million in 2000 and 110 million

in 1996, partly due to large infrastructure

financings. - Total issuance has been on the rise, but the

total number of issues has been declining since

1998 as larger issue sizes dominate, particularly

for infrastructure and financial institutions. - Issue size of at least 250 million is now

considered the minimum for reasonable secondary

market liquidity. - New issues have been hot this year, generally

significantly oversubscribed resulting in

fractional fills. - Medium term notes now make up the majority of new

issues, compared to only 10 in 1993.

10

- Offering Process

- Overview of Canadian Corporate Issuing Options

- In the Canadian market, most corporate bonds are

issued through a public process. - The private market is generally used for smaller

unrated issues which are placed with a small

number of insurance companies, and a few other

institutional investors. Private placements

cannot be sold to retail investors. - The Canadian market for A and better rated

issuers is well established. - The BBB market is growing, but many BBB issuers

still consider cross-border issuance. - High yield debt is generally issued in the U.S.

market, although there have been some high yield

deals recently in Canada.

11

- Offering Process

- Overview of Public Issuing Options

- For a one-time or first financing in the Canadian

public market, issuers take advantage of

short-form issuer status if available and follow

the public debenture process. - However, should the issuer wish to establish a

long-term debt issuance platform, there are

several options available - debt shelf

- MTN shelf or

- combination thereof.

Canadian Issuing

Fully Registered

Debt Shelf

Issue by Issue filings(short form)

MTN Shelf

Pricing Supplement only

MTN Program

Debentures

Prospectus Supplement only

Pricing Supplement only

12

- Offering Process

- Private vs. Public Markets

- the issuer can issue long term debt through

either a public offering or a private placement

of debt securities in Canada or in the U.S., or

both. - The determination as to which form of

distribution is optimal is a function of the

issuers requirements and priorities.

13

- Offering Process

- Private vs. Public Markets

14

- Offering Process

- Overview of Public Issuing Options

- The issuer can enter the Canadian public debt

market through a discrete marketed underwritten

debt issue via a POP (short-form) prospectus, or

under a shelf prospectus. - Under a shelf, either an MTN offering or a

discrete marketed underwritten issue is possible. - An MTN program is a continuously offered term

debt issuance platform which is a further

refinement of the short form filing arrangements

and goes a step further in removing the

documentation process from the issue process. - An MTN program requires the filing of a debt

shelf with an MTN carve-out or a dedicated MTN

shelf. Both contemplate borrowings over a two

year period. - Typically, MTNs are distributed on an agency

(best efforts) basis. - Although historically some issuers have used the

MTN process to complete their first or second

issues, investor response to this format has been

inconsistent. Investors view MTN programs as

being less supported by dealers and as a result

are more likely to not participate. - Savings on an MTN program for a 10 year are

approximately 4 bps. This small differential in

cost is usually insufficient for new or

infrequent issuers to absorb the additional risk

of an MTN process. A Shelf filing is most

appropriate for high quality, frequent issuers to

the market. - First time issuers generally use a discrete

marketed underwritten process via POP prospectus

with a book building phase to ensure maximum size

and ensure a successful deal.

15

- Offering Process

- Corporate issuance of MTNs has grown

dramatically during the past five years. - MTNs offer

- Considerable flexibility in terms of amount, term

and timing - Rapidity of execution

- The possibility for reverse inquiry

- A platform for structured notes

- Cost savings on commissions compared to

conventional public debentures - MTNs disadvantages include

- Limited access to the retail distribution network

- An MTN program is most effective for

opportunistic access - a debenture process is

better suited to needs of required sizing or

timing - Considerable time spent fishing with accounts

on reverse inquiry - Continuous issuance potentially hurts spreads.

Large number of maturities and issues dont trade

as well in secondary market

16

- Offering Structure

- Issuer

- Determine the issuing entity to maximize the

rating, with guarantees from parents or

subsidiaries as needed. - Issue Size

- Issuers generally launch an initial benchmark

debenture issue of 150 - 200 million, with

potential follow-on issuance. For recent

infrastructure deals larger initial issuance size

has been common. Initial issue size was more

typically just 100 million a few years ago. - To best determine the issue size, the issuer

often establishes a size range and then build a

book through the marketing process. At the

completion of the marketing program, the issue

would then be sized.

17

- Offering Structure

- Term to Maturity

- Most common terms to maturity in the public

debenture market are 5, 7, 10 and 30 year

bullets. - A 5 year term is most in demand by investors and

offers the best pricing and lowest execution

risk, particularly for first time BBB issuers. - If the issuer has significant initial financing

needs a multi-tranche issue would be used. - Covenant Pattern

- The Canadian public debt market covenant pattern

is very flexible - negative pledge

- cross-default (can be monetary cross-default,

non-monetary cross-acceleration). - The above pattern offers considerable increased

flexibility versus bank loans. - Private issues generally contain more covenants,

which can include both incurrence and maintenance

tests based on various financial ratios.

18

- Offering Structure

- Issuance Process

- MTNs are generally issued on an agency basis

and different issuing procedures are available - Use of exempt lists spreads are posted through

the dealers with distribution on the basis of an

exempt list - The allotment approach spreads are posted

through dealers on an allotment basis. Any

allotments unsold after a specified period of

time are reallocated to dealers with excess

demand - Jump ball where the issue is sold on a first come

first served basis - Reverse inquiry/lead orders driven by investor

demand

19

- Offering Structure

- Issuance Process

20

- Offering Structure

- Marketing

- Regardless of whether the issuer chooses to

launch an MTN program directly or issue

underwritten debentures, we generally recommend a

fully marketed conventional syndication process

including exempt coverage, a lead bookrunner and

a defined syndicate, and retail participation for

first time or infrequent issuers. - Marketing generally consists of luncheon

presentations for debt investors in Toronto and

Montreal and possibly, Winnipeg and Vancouver.

These are generally complemented by one-on-one

presentations with key investors, and conference

calls for those unable to attend personally. - This process is similar for private placements,

although the number of potential investors is

much smaller, so often only one group

presentation is scheduled, or the issue is

launched entirely through one-on-one

presentations. - Subsequent tranches of MTNs are issued with no

marketing since the MTN platform provides

continuous disclosure about the issuer and MTNs

are often issued based on reverse inquiry I.e.

an investor or group of investors indicates an

interest in a particular maturity or a specific

structure.

21

- Offering Structure

- Syndicate

- One of the keys to success for a public debt

issue in Canada (debentures and/or MTNs) is a

strong syndicate, defined as market-leading

investment dealers with strong distribution

capability (both retail and institutional) who

will provide consistent trading support, research

coverage and on-going market intelligence and

advisory services. - Issuers generally use a syndicate consisting of 3

- 4 dealers with a lead or two co-leads. - The syndicates are increasingly determined by

participation in bank lending to the issuer.

This is also true in the U.S. market. - Cross-Currency Swap

- The issuer may choose to swap a portion to U.S.

dollars to effectively create a U.S. dollar

obligation to hedge some U.S. dollar revenues.

22

- Offering Structure

- Timing

- The public short-form debenture issuance process

takes approximately 6 weeks. Long-form (required

for first time issuers that are not already

reporting issuers) takes approxiately 10 weeks.

23

- Offering Structure

- Budget and Documentation

- Principal documentation includes

- MTN Shelf Prospectus

- Covenant Package

- Selling Agency Agreement

- Rating agency presentation

Counsel 35,000 - 75,000 Printing (Prospectus,

Certificate) 15,000 Rating Agencies

Fees 50,000 Trustee 15,000 Filing

Fees 20,000 CDS

5,000 140,000 - 180,000

24

- Offering Structure

- Rating Agency Process

25

- Canadian Fixed Income Money Management

- Who are the investors?

- Insurance Companies

- Pension Funds (mostly managed by investment

counsellors, except - OTPP

- OMERS

- Caisse de Depot

- Other government and a few private pension plans

- Mutual Funds

- Investment Counsellors

- Pension money

- Endowment money

- Insurance Money

- Private Wealth

Recommended

CrystalGraphics Presentations