Financial Accounting and Accounting Standards - PowerPoint PPT Presentation

Title:

Financial Accounting and Accounting Standards

Description:

Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency. Understand the concept of earning power, ... – PowerPoint PPT presentation

Number of Views:153

Avg rating:3.0/5.0

Title: Financial Accounting and Accounting Standards

1

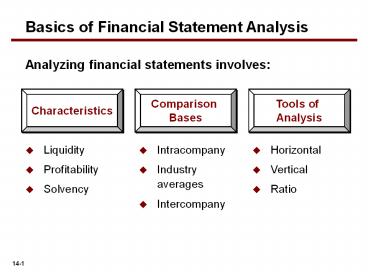

Basics of Financial Statement Analysis

Analyzing financial statements involves

Characteristics

Comparison Bases

Tools of Analysis

- Liquidity

- Profitability

- Solvency

- Intracompany

- Industry averages

- Intercompany

- Horizontal

- Vertical

- Ratio

2

Horizontal Analysis

- Horizontal analysis, also called trend analysis,

is a technique for evaluating a series of

financial statement data over a period of time. - Purpose is to determine the increase or decrease

that has taken place. - Commonly applied to the balance sheet, income

statement, and statement of retained earnings.

3

Horizontal Analysis

Illustration 14-5 Horizontal analysis of balance

sheets

Changes suggest that the company expanded its

asset base during 2009. It financed this

expansion primarily by retaining income rather

than assuming additional long-term debt.

4

Horizontal Analysis

Illustration 14-6 Horizontal analysis of Income

statements

Overall, gross profit and net income were up

substantially. Gross profit increased 17.1,

and net income, 26.5. Qualitys profit trend

appears favorable.

5

Vertical Analysis

- Vertical analysis, also called common-size

analysis, is a technique that expresses each

financial statement item as a percent of a base

amount. - On an income statement, we might say that selling

expenses are 16 of net sales. - Vertical analysis is commonly applied to the

balance sheet and the income statement.

6

Vertical Analysis

Illustration 14-8 Vertical analysis of balance

sheets

These results reinforce that the company is

financing its growth through operations and not

through issuing additional debt.

7

Vertical Analysis

Illustration 14-9 Vertical analysis of Income

statements

Company appears to be a profitable enterprise

that is becoming even more successful.

8

Ratio Analysis

Ratio analysis expresses the relationship among

selected items of financial statement data.

Financial Ratio Classifications

Liquidity

Profitability

Solvency

Measures short-term ability of the company to pay

its maturing obligations and to meet unexpected

needs for cash.

Measures the income or operating success of a

company for a given period of time.

Measures the ability of the company to survive

over a long period of time.

9

Ratio Analysis

A single ratio by itself is not very meaningful.

The discussion of ratios will include the

following types of comparisons.

10

Ratio Analysis

Liquidity Ratios

Measures short-term ability of the company to pay

its bills-debt and to meet unexpected cash needs.

Specific ratios include

- Current ratio (can I pay upcoming bills),

11

Liquidity Ratios

Ratio Analysis

1. Current Ratio

Ratio means that for every dollar of current

liabilities, Quality has 2.96 of current assets.

12

Ratio Analysis

Liquidity Ratios

Measures short-term ability of the company to pay

its bills-debt and to meet unexpected cash needs.

Specific ratios include

- Current ratio (can I pay upcoming bills),

- Acid-test ratio (more refined than current

ratio)

13

Liquidity Ratios

Ratio Analysis

2. Acid-Test Ratio

Illustration 14-13

14

Liquidity Ratios

Ratio Analysis

2. Acid-Test Ratio

Measures immediate liquidity.

15

Ratio Analysis

Liquidity Ratios

Measures short-term ability of the company to pay

its bills-debt and to meet unexpected cash needs.

Specific ratios include

- Current ratio (can I pay upcoming bills),

- Acid-test ratio (more refined than current

ratio) - Receivable turnover (how quick do I collect )

16

Liquidity Ratios

Ratio Analysis

3. Receivable Turnover

17

Liquidity Ratios

Ratio Analysis

Receivable Turnover

2,097,000

10.2 times

(180,000 230,000) / 2

A variant of the Receivable turnover ratio is to

convert it to an average collection period in

terms of days.

365 days / 10.2 times every 35.78 days

Receivables are collected on average every 36

days.

18

Ratio Analysis

Liquidity Ratios

Measures short-term ability of the company to pay

its bills-debt and to meet unexpected cash needs.

Specific ratios include

- Current ratio (can I pay upcoming bills),

- Acid-test ratio (more refined than current

ratio) - Receivable turnover (how quick do I collect )

- Inventory turnover (effectiveness of company).

19

Liquidity Ratios

Ratio Analysis

4. Inventory Turnover

Illustration 14-16

Measures the number of times, (on average), the

inventory is sold during the period.

20

Liquidity Ratios

Ratio Analysis

Inventory Turnover

1,281,000

2.3 times

(500,000 620,000) / 2

A variant of inventory turnover is the days in

inventory.

365 days / 2.3 times every 159 days

Inventory turnover ratios vary considerably among

industries.

21

Ratio Analysis

Profitability Ratios

Measure the income or operating success of a

company for a given period of time. Ratios

include

- Profit margin

22

Profitability Ratios

Ratio Analysis

5. Profit Margin

Measures the percentage of each dollar of sales

that results in net income.

23

Ratio Analysis

Profitability Ratios

Measure the income or operating success of a

company for a given period of time. Ratios

include

- Profit margin

- Asset turnover

24

Profitability Ratios

Ratio Analysis

6. Asset Turnover

Measures how efficiently a company uses its

assets to generate sales.

25

Ratio Analysis

Profitability Ratios

Measure the income or operating success of a

company for a given period of time. Ratios

include

- Profit margin

- Asset turnover

- Return on assets

26

Profitability Ratios

Ratio Analysis

7. Return on Asset

An overall measure of profitability.

27

Ratio Analysis

Profitability Ratios

Measure the income or operating success of a

company for a given period of time. Ratios

include

- Profit margin

- Asset turnover

- Return on assets

- Return on common stockholders equity

28

Profitability Ratios

Ratio Analysis

8. Return on Common Stockholders Equity

Illustration 14-20

Shows how many dollars of net income company

earned for each dollar invested by owners.

29

Ratio Analysis

Profitability Ratios

Measure the income or operating success of a

company for a given period of time. Ratios

include

- Profit margin

- Asset turnover

- Return on assets

- Return on common stockholders equity

- Earnings per share

30

Profitability Ratios

Ratio Analysis

9. Earnings Per Share (EPS)

A measure of the net income earned on each share

of common stock.

31

Ratio Analysis

Profitability Ratios

Measure the income or operating success of a

company for a given period of time. Ratios

include

- Profit margin

- Asset turnover

- Return on assets

- Return on common stockholders equity

- Earnings per share

- Price to earnings ratio

32

Profitability Ratios

Ratio Analysis

10. Price-Earnings Ratio

Measures the net income earned on each share of

common stock.

33

Ratio Analysis

Profitability Ratios

Measure the income or operating success of a

company for a given period of time. Ratios

include

- Profit margin

- Asset turnover

- Return on assets

- Return on common stockholders equity

- Earnings per share

- Price to earnings ratio

- Payout ratio

34

Profitability Ratios

Ratio Analysis

11. Payout Ratio

Measures the percentage of earnings distributed

in the form of cash dividends.

35

Ratio Analysis

Solvency Ratios

- Solvency ratios measure the ability of a company

to survive over a long period of time. Ratios

include - Debt to Total Assets

36

Solvency Ratios

Ratio Analysis

12. Debt to Total Assets Ratio

Measures the percentage of the total assets that

creditors provide.

37

Ratio Analysis

Solvency Ratios

- Solvency ratios measure the ability of a company

to survive over a long period of time. Ratios

include - Debt to Total Assets

- Times Interest Earned

38

Solvency Ratios

Ratio Analysis

13. Times Interest Earned

Indicates ability of the company to meet interest

payments as they come due.

39

Ratio Analysis

Summary of Ratios

Illustration 14-26

40

Summary of Ratios

Illustration 14-26

41

Earning Power and Irregular Items

- Earning power means the normal level of income to

be obtained in the future. - Irregular items are separately identified on

the income statement. Two types are - Discontinued operations.

- Extraordinary items.

42

Earning Power and Irregular Items

Discontinued Operations

- Disposal of a significant component of a

business. - Report the income (loss) from discontinued

operations in two parts - income (loss) from operations (net of tax) and

- gain (loss) on disposal (net of tax).

43

Earning Power and Irregular Items

Illustration During 2014 BD Incorporated Has

income before taxes of 79,000,000.

Discontinued and sold its unprofitable chemical

division. Loss from chemical operations (net of

135,000 taxes) was 315,000. Loss on disposal

of the chemical division (net of 81,000 taxes)

was 189,000. (Assume a 30 tax rate on income).

44

Earning Power and Irregular Items

Discontinued Operations are reported after

Income from continuing operations.

Previously labeled as Net Income.

Moved to

45

Earning Power and Irregular Items

Extraordinary Items

- Nonrecurring material items that differ

significantly from a companys typical business

activities. - Must be both of an

- Unusual Nature and

- Occur Infrequently.

- Must consider the environment in which it

operates. - Amounts reported net of tax.

46

Earning Power and Irregular Items

Illustration In 2014 a foreign government

expropriated property held as an investment by DB

Inc. If the loss is 770,000 before income

taxes of 231,000, the income statement will

report a deduction of 539,000.

47

Earning Power and Irregular Items

Extraordinary Items are reported after Income

from continuing operations.

Previously labeled as Net Income.

Moved to

48

Earning Power and Irregular Items

Reporting when both Discontinued Operations

and Extraordinary Items are present.

Discontinued Operations

Extraordinary Item

49

Earning Power and Irregular Items

Change in Accounting Principle

- Occurs when the principle used in the current

year is different from the one used in the

preceding year. - Accounting rules permit a change if justified.

- Changes are reported retroactively.

- Example would include a change in inventory

costing method such as FIFO to average cost.

50

Earning Power and Irregular Items

Comprehensive Income

All changes in stockholders equity except those

resulting from investments by stockholders and

distributions to stockholders.

Reported in Stockholders Equity

- Unrealized gains and losses on available-for-sale

securities. - Plus other items

51

Earning Power and Irregular Items

Comprehensive Income

- Why are gains and losses on available-for-sale

securities excluded from net income? - Because disclosing them separately

- reduces the volatility of net income due to

fluctuations in fair value, - yet informs the financial statement user of the

gain or loss that would be incurred if the

securities were sold at fair value.

52

Quality of Earnings

A company that has a high quality of earnings

provides full and transparent information that

will not confuse or mislead users of the

financial statements.

- Companies have incentives to manage income to

meet or beat Wall Street expectations, so that - the market price of stock increases and

- the value of stock options increase.

Recommended

CrystalGraphics Presentations