FINANCIAL RATIOS PowerPoint PPT Presentation

1 / 11

Title: FINANCIAL RATIOS

1

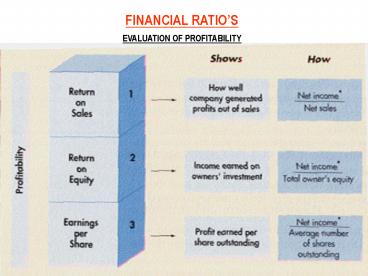

FINANCIAL RATIOS

EVALUATION OF PROFITABILITY

2

EVALUATION OF PROFITABILITY

Profit marginNet Income / Net sales

- Also known as Return on Sales

- Net income is taken after taxes

- Measure of Net Income a company makes per unit of

sales

Asset Turnover Net Sales / Average total assets

- Measure of how efficient a company is using

assets to produce sales

3

EVALUATION OF PROFITABILITY

Return on Assets Net Income / Average total

assets

To measure how much income a company makes for

each of Asset

Return on Equity Net Income / Average

stockholders equity

- Also known as Return on Investment

- Measure of the income earned on owners investment

4

EVALUATION OF LIQUIDITY

5

EVALUATION OF LIQUIDITY

Working Capital Current Assets- Current

Liabilities

- A Measure of liquidity

- Represents current assets remaining after payment

of all current liabilities - The dollar value of Working capital can be

misleading since it may include value of slow

moving inventory. Inventory that cannot be used

to clear a companys short term debt. - The value of Working Capital does not consider

the size of the company.

Caution

6

EVALUATION OF LIQUIDITY

Current Ratio Current Assets/current

Liabilities

- Measure of a firms short term liquidity

- Compares the current debt owed with the current

assets available to pay the debt

Quick Ratio (Cash Marketable SecuritiesAccounts

Receivable)/Current Liabilities

- The Acid test ratio

- Good indicator of firms ability to pay creditors

since inventories are not included

7

EVALUATION OF ACTIVITY

8

EVALUATION OF ACTIVITY

Average Days sales uncollected 365 days /

receivable turnover

- Measure of how many days on average a company has

to wait for Accounts

Receivable to turn to cash

Inventory TurnoverCost of goods sold/Average

inventory

- Measure of how fast a company can convert its

inventories into sales - Quicker the better

- Inventory sitting on shelves implies holding

costs - Risk of inventory becoming obsolete

9

EVALUATION OF ACTIVITY

Receivable TurnoverNet Sales / Average Accounts

Receivable

- Measure of frequency with which a company turns

its accounts receivables to cash - Measure of a companys Credit and Collection

policies - Who qualifies for credit and who does not

- How long customers are given to pay their bills

- How aggressive is the company in collecting its

debts - If ratio is increasing need to determine whether

company doing better job of collection or Sales

going up - If ratio is going down need to determine whether

company lagging in sales or collection efforts

are failing

Caution

10

EVALUATION OF LEVERAGE

11

EVALUATION OF LEVERAGE

Debt to Equity Total liabilities / Total

Stockholders Equity

- Extent to which a business is financed by debt as

opposed to invested capital (Stockholders Equity) - From lenders stand point the lower the ratio

safer the company- since company has less

existing debt - May also imply low growth rate - company may be

financing its growth by using excess cash flow

from operations

Debt to Total Assets Total liabilities / Total

Assets

- Measure of firms ability to carry long term debt

- As a rule of thumb amount of debt should not

exceed 50 of the value of assets

Recommended