Concepts of Equity Method' 1

1 / 17

Title:

Concepts of Equity Method' 1

Description:

When Cost BV acquired, the difference must be identified and accounted for. ... Reporting the sale of an equity investment. 1-14. Concepts of Equity Method. - 15 ... – PowerPoint PPT presentation

Number of Views:59

Avg rating:3.0/5.0

Title: Concepts of Equity Method' 1

1

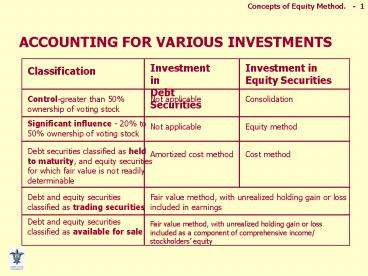

ACCOUNTING FOR VARIOUS INVESTMENTS

Investment in Debt Securities

Investment in Equity Securities

Classification

Control-greater than 50 ownership of voting stock

Not applicable

Consolidation

Significant influence - 20 to 50 ownership of

voting stock

Not applicable

Equity method

Debt securities classified as held to maturity,

and equity securities for which fair value is not

readily determinable

Amortized cost method

Cost method

Debt and equity securities classified as trading

securities

Fair value method, with unrealized holding gain

or loss included in earnings

Debt and equity securities classified as

available for sale

Fair value method, with unrealized holding gain

or loss included as a component of comprehensive

income/ stockholders equity

2

Size (of the Investment) Matters!!!

1-2

Fair Value

Equity Method

Consolidated Financial Statements

0

20

50

100

In some cases, influence or control may exist

with less than 20 ownership.

3

The Significance of the Size of the Investment

1-3

Fair Value

Equity Method

Consolidated Financial Statements

0

20

50

100

Significant influence is generally assumed with

20 to 50 ownership.

4

The Significance of the Size of the Investment

1-4

Fair Value

Equity Method

Consolidated Financial Statements

0

20

50

100

Financial Statements of all related companies

must be consolidated.

5

Criteria for Determining Whether There is

Significant Influence (APB Opinion 18)

1-5

Representation on the investees Board of

Directors

Participation in the investees policy-making

process

Material intercompany transactions.

Interchange of managerial personnel.

Technological dependency.

Extent of ownership in relationship to other

investor ownership percentages.

6

Equity Method

1-6

- Requires that the investor has the potential for

significant influence. - Generally used when ownership is between 20 and

50. - Significant Influence might be present with much

smaller ownership percentages. (The accountant

must consider the particulars!!!)

7

Remember

1-7

- The ability to exert significant influence is the

determining factor in applying the equity method - No actual influence need have been applied!!

8

EQUITY METHODEvidence against Significant

Influence

- Investee opposition

- Investor/investee agreement

- Closely held majority

- stockholder

- Lack of information

- Lack of board representation

9

Equity Method

1-9

- Step 1 The investor records its investment in

the investee at cost. - Journal entry

- Debit Investment in Investee

- Credit Cash (or other Assets/Stock)

Cost can be defined by cash paid or the Fair

Market Value of Stock or Assets given up.

10

Equity Method

1-10

- Step 2 The investor recognizes its

proportionate (pro rata) share of the investees

net income (or net loss) for the period. - Journal entry at end of period

- Debit Investment in Investee

- Credit Equity in Investee Income

This will appear as a separate line-item on the

investors income statement.

11

Equity Method

1-11

- Step 3 The investor reduces the investment

account by the amount of cash dividends received

from the investee. - Journal entry when cash dividends received

- Debit Cash

- Credit Investment in Investee

12

Excess of Cost Over BV Acquired

1-12

- When Cost gt BV acquired, the difference must be

identified and accounted for.

When Cost gt BV acquired, the difference must be

identified and accounted for.

13

Excess of Cost Over BV Acquired

1-13

The amortization of the difference associated

with the undervalued assets is recorded as a

reduction of both the Investment account and the

Equity in Investee Income account.

14

Special Procedures for Special Situations

1-14

Reporting a change to the equity method.

Reporting the sale of an equity investment.

Reporting investee income from sources other than

continuing operations.

Reporting investee losses.

15

Reporting a Change to the Equity Method.

(Retroactive Adjustment)

1-15

- An investment that is too small to have

significant influence is accounted for using the

fair-value method. - When ownership grows to the point where

significant influence is established . . .

. . . all accounts are restated so that the

investors financial statements appear as if the

equity method had been applied from the date of

the first original acquisition. - - APB Opinion

18

?

16

Reporting Investee Losses

1-16

- A permanent decline in the investees fair

market value is recorded as an impairment loss

and the reduction of the investment account to

the fair value.

A temporary decline is ignored!!!

17

Possible Criticisms

1-17

- Over-emphasis on possession of 20-50 voting

stock in deciding on significant influence vs.

control - Possibility of off-balance sheet financing

- Potential manipulation of performance ratios

Recommended

CrystalGraphics Presentations