Users: - PowerPoint PPT Presentation

1 / 16

Title:

Users:

Description:

... end, must zero-out FOH: transfer. balance to Cost of Goods Sold ... than actual costs incurred (credit balance) Underapplied FOH amount allocated is less than ... – PowerPoint PPT presentation

Number of Views:44

Avg rating:3.0/5.0

Title: Users:

1

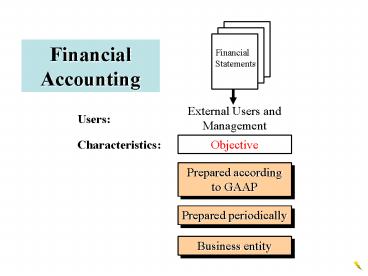

Financial Accounting

Users

Objective

Characteristics

Prepared according to GAAP

Prepared periodically

Business entity

2

Managerial Accounting

Users

Objective and subjective

Characteristics

Prepared according to management needs

Prepared periodically or as needed

Business entity or segment

3

What is a Cost?

- Managers rely on management accountants to

- provide useful cost information to support

decision - making

- Cost - a payment of cash (or a commitment to pay

- cash in the future) in order to generate revenue.

A - cost provides a benefit

4

Manufacturing Cost Terms (1)

- Direct Material costs costs that 1) are an

integral part of the product being made and 2)

are significant - Indirect Material costs costs that are not a

significant portion of total product costs (part

of Factory Overhead) - Direct Labor costs salaries/wages that 1) are

directly involved in the manufacturing process

and 2) are significant - Indirect labor costs salaries/wages not

directly involved in the manufacturing process

(part of Factory Overhead)

5

Manufacturing Cost Terms (2)

- Factory Overhead costs costs other than direct

materials and direct labor incurred in the

manufacturing process - Product costs direct materials direct labor

factory overhead - Conversion costs direct labor factory

overhead

6

Cost Accounting Systems

- Purpose used to accumulate product costs

- Used by managers to

- Establish product prices

- Develop Financial Statements

- Control operations (by supply of data on costs

incurred by each manufacturing department or

process)

7

Types of Cost Accounting Systems (1)

- Job Order Cost System a separate record

- is maintained for the cost of each quantity of

- product that is made

- Custom goods

- Special orders

- High dollar items

8

Types of Cost Accounting Systems (2)

- Process Cost System costs are

- accumulated for each department or

- process within a factory products are

- indistinguishable from each other

- Food products

- Oil/chemical products

- Office supplies (pens, paper clips, etc.)

9

Overview of Job Order Costing

Costs Expenses

Product Costs

Balance Sheet

Materials Purchases

Income Statement

Finished Goods Inventory

Period Costs

Selling and Administrative

10

Journal Entries (1)

11

Journal Entries (2)

12

Ledger Accounts (1)

13

Ledger Accounts (2)

14

Allocation of Factory Overhead

- End-of-Month wait until all costs are recorded

for - month, then allocate to WIP using some Activity

- Base

- Predetermined Rates calculate rates in

- Advance, per some Activity Base, then

- allocate to WIP as needed

- Estimated total Factory Overhead

costs - Rate -------------------------------------------

-------- - Estimated Activity Base

15

Disposal of FOH Balance When Using Predetermined

Rate

- Balance in FOH is carried forward from

- month to month as Deferred debit or credit

- At year-end, must zero-out FOH transfer

- balance to Cost of Goods Sold

- Overapplied FOH amount allocated is greater

- than actual costs incurred (credit balance)

- Underapplied FOH amount allocated is less than

- actual costs incurred (debit balance)

16

Other

- Activity-Based Costing method of accumulating

and allocating FOH costs to products using many

different overhead rates - Period Costs expenses used in generating

revenue but not involved in the manufacturing

process - Selling Expenses

- Administrative Expenses

Recommended

CrystalGraphics Presentations