Autocorrelation PowerPoint PPT Presentation

1 / 8

Title: Autocorrelation

1

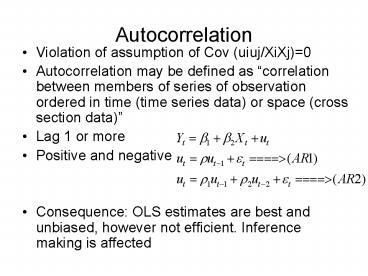

Autocorrelation

- Violation of assumption of Cov (uiuj/XiXj)0

- Autocorrelation may be defined as correlation

between members of series of observation ordered

in time (time series data) or space (cross

section data) - Lag 1 or more

- Positive and negative

- Consequence OLS estimates are best and unbiased,

however not efficient. Inference making is

affected

2

Reasons for autocorrelation

- Inertia inbuilt momentum, nonstationarity

- Specification bias

- excluded variable

- Wrong functional form

- Lags

- Data manipulation

- Variance of OLS Estimator in the presence of

autocorrelation (AR1) is still not efficient

3

Detecting autocorrelation

- Graphical method residuals against time,

- residuals against lag of residuals

- Runs or Geary test non-parametric test

- Signs of the residuals are ordered in time

- Clustering of and are called runs ( R )

- No. of times there is runs are ( N1 )

- No. of times there is - runs are ( N2 )

- N is total no. of observations (N1 N2)

- If R lies outside the limits, autocorrelation

exists.

4

Durbin Watson d test

- Most popular autocorr. test

- As thumb rule, if d is clos to 2, no

autocorrelation. If d is close o 4, negative

autocorrelation. If d is close to 0, positive

autocorrelation - Assumptions

- Regression model includes constant

- No lagged dependent variables on RHS

- explanatory variables are fixed

- Detects first order autocorr only

- Error term is normally distributed

- No missing data

5

(No Transcript)

6

DW decision rules

AutoCorr

- AutoCorr

No decision

No decision

NO Autocorrelation

0 dL dU

2 4-dU 4-dL

4

7

Breusch-Godfrey test

- Lagged regressands, Higher order autocorrelation,

higher order Y lags - If estimated value is higher than critical

chi-sq, reject the null hypothesis of no

autocorrelation

8

Remedial measures

- GLS when p is known( Cochrane-Orcutt two-step

procedure) - Prais-Winsten transformation

- When p is unknown (FGLS)

- Use DW test to estimate p and transform as above

- First difference method

- Newey West SE correction method (HAC) large

sample test

Recommended