TimeSeries Analysis PowerPoint PPT Presentation

1 / 10

Title: TimeSeries Analysis

1

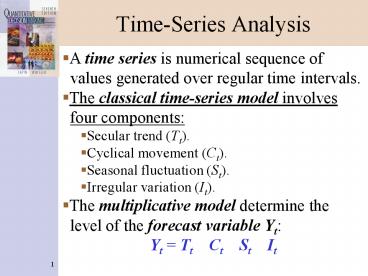

Time-Series Analysis

- A time series is numerical sequence of

- values generated over regular time intervals.

- The classical time-series model involves

- four components

- Secular trend (Tt).

- Cyclical movement (Ct).

- Seasonal fluctuation (St).

- Irregular variation (It).

- The multiplicative model determine the

- level of the forecast variable Yt

- Yt Tt Ct St It

2

Classical Time-Series Model

3

Exponential Smoothing

- Finding the components is difficult.

- A direct approach averages past Yt values by

exponential smoothing. - The forecast value is computed from

- Ft1 aYt (1- a)Ft

- The above involves a single parameter, the

smoothing constant (a) alpha. - All previous time periods are reflected in the

Fs, and greater weight is given to the more

recent.

4

Forecasts with Single-Parameter Exponential

Smoothing

5

Single-Parameter Forecasts

- The preceding slide shows single-parameter

forecasts of Blitz Beer sales. These were

generated by computer. - The level for a was .20. A greater a will assign

more weight to the present. - Quality of forecasts may be measured. Most

common is the mean squared error - which averages errors over all forecasts made.

- Other measures are the mean absolute deviation

(MAD) and mean absolute percent error (MAPE).

6

Two-Parameter Exponential Smoothing

- The smoothing constant can be tuned to the past,

possibly providing better forecasts. - But single-parameter forecasts may still lead or

lag actuals, as seen for Blitz Beer, because the

impact of trends is delayed. - Trend Tt can be incorporated with a second trend

smoothing constant g (gamma) - Tt aYt (1 a)(Tt 1 bt 1)

- bt g(Tt Tt 1) (1 g)bt 1

- Ft1 Tt bt

- That greatly reduces Blitz Beers MSE.

7

Forecasts with Two-Parameters

8

Seasonal Exponential Smoothing with Three

Parameters

- Many time series have regular seasonal patterns

to be incorporated into forecasts. - The three-parameter model incorporates a seasonal

smoothing constant b (beta) - Tt a(Yt /St p) (1 a)(Tt 1 bt 1)

- bt g(Tt Tt 1) (1 g)bt 1

- St b(Yt /Tt) (1 b)St p

- Ft1 (Tt bt) St p1

9

Forecasting withThree Parameters

10

Forecasting withThree Parameters

- The above works for p 4 quarters or p 12

months. - The preceding slide needs 6 quarters to generate

the first (very bad) forecast. - The process settles quickly, providing good

forecasts p periods into the future.

Recommended