StoredAccount Payment Systems - PowerPoint PPT Presentation

1 / 24

Title:

StoredAccount Payment Systems

Description:

... is labeled with two different unique PayPal merchant identifiers ... The user present them to PayPal to prove that he/she is indeed the genuine card holder ... – PowerPoint PPT presentation

Number of Views:126

Avg rating:3.0/5.0

Title: StoredAccount Payment Systems

1

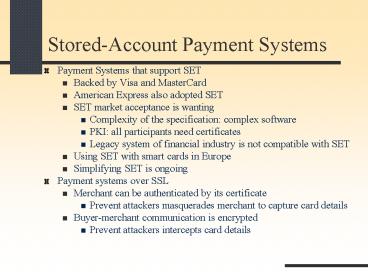

Stored-Account Payment Systems

- Payment Systems that support SET

- Backed by Visa and MasterCard

- American Express also adopted SET

- SET market acceptance is wanting

- Complexity of the specification complex software

- PKI all participants need certificates

- Legacy system of financial industry is not

compatible with SET - Using SET with smart cards in Europe

- Simplifying SET is ongoing

- Payment systems over SSL

- Merchant can be authenticated by its certificate

- Prevent attackers masquerades merchant to capture

card details - Buyer-merchant communication is encrypted

- Prevent attackers intercepts card details

2

Centralized Account Payment

- Both the payer and payee hold accounts at the

same centralized on-line financial institution - The payer securely connects to the bank, and

informs it to move a certain amount from the

payers account into the payees account - The bank subtract an amount from one account and

add the amount to another account - Drawback all participants must have an account

with the same payment system - Centralized account model is popular on the

internet - PayPal, Yahoo! PayDirect, InternetCash, CyberGold

- Used by Amazon.com, eBay, AOL QuickCash

3

Funding the Account

- The on-line accounts are not real bank account

- They are not governed by national banking

regulations - They do not provide the facilities of a real

certified bank - They are typically limited 10,000 or less

- The most popular method of funding an on-line

account is to use a payment card - Credit card or debit card

- Authentication of credit card owner is necessary

- Other methods of funding

- Transfer funds from a regular bank account

- Prepaid card from a physical store

4

Card Owner Authentication

- International credit card owner authentication by

PayPal - The user sign up

- PayPal sends two credit lodgments to the credit

card account - Each deposit is a small random amounts between 1

cent to 99 cents - Each transaction is labeled with two different

unique PayPal merchant identifiers - The user query his/her credit card account

statement to obtain the credit amounts and

merchant identifiers - The user present them to PayPal to prove that

he/she is indeed the genuine card holder

5

Account Transfer Authentication

- User-to-User payment

- Account holder is authenticated using an account

identifier and a password - Email address may be used as account identifier

- All communication is over SSL

- Payment procedure

- Payer log on the centralized account system

- Payer authorize payment transfer

- The payee are notified by email

- A email confirmation is sent to payer

- Payee log on the centralized account system to

verify the payment

6

Account Transfer Authentication (continued)

- User-to-Merchant payment

- Customer shop inside merchants website

- Customer select payment system

- Merchants web server redirect the costumer to

payment system with transaction details - Customer log on payment system and authorize the

payment - Payment system redirect customer to merchants

website and send payment indication to merchants

server - Merchant deliver goods or service

7

CyberCash

- http//www.cybercash.com

- Founded in 1994 to provide software and service

solutions for secure financial transactions over

the Internet - Acquired by VeriSign in 2001

- CyberCash wallet

- A client software runs alongside browser

- Aims to make purchase as transparent as possible

to the user by hiding the details of the payment

steps and message - CyberCash persona

- Unique CyberCash ID and pass phrase for every

user (customer and merchant) - Map the user's private/public key pair

- Unlock wallet

- Emergency close-out in case of fraud

8

CyberCash Model

From Donal OMahony, et al., "Electronic Payment

Systems"

9

Payment steps

Consumer

Merchant

CyberCash Server

Finish shopping

Order form

Credit-card data

Forward details

Authorize clear with bank

Issue receipt

Log transaction

10

Payment steps (continued)

- A CyberCash purchase

- Customer click on "Pay" in a browser

- Payment-Req (PR)

- From the merchant to the buyer to launch the

CyberCash wallet - Contains summary of the order signed by the

merchant - The signature is verified by CyberCash server

later - Credit card payment (CH1)

- From the buyer to the merchant

- Contains card data, a hash code of the order, and

merchant's signature on the order - encrypted by public key of CyberCash server

(PKcs) - Signed by the buyer

11

Payment steps (continued)

- Auth-Capture

- The merchant forward the encrypted data to

CyberCash server - The server verify

- Buyer's signature and card data

- Merchant's signature on the order details

- Charge-Action-Response

- After having authorized and captured the purchase

in the bank network - From the server to the merchant

- Contains unsigned receipts for the merchant and

buyer - Charge-Card-Response (CH2)

- The merchant forwards the unsigned receipt from

the server to the buyer

12

Payment steps (continued)

- Binding credit cards

- A cardholder must register his/her credit card to

CyberCash persona - Message from customer to CyberCash server

- Kdes(card detail), PKcs(Kdes)

- Validation with issuer

- Message from CyberCash server to the customer

- Kdes(Success/Failure, card detail)

- CyberCash plan to update their payment protocol

to be SET-compatible

13

Stored-Value Payment Systems

- What is it?

- Electronic Cash

- Hard-currency systems over an electronic medium

- Pros and cons

- Payment can be instantaneous and potentially

anonymous - Cost per transaction is smaller

- Support low-value transaction

- The proximity of payer and payee is not an issue

for electronic payments - Anonymous but traceable

- Provides privacy of purchases while discouraging

illicit sales

14

Stored-Value Payment Systems (continued)

- High-security risks

- Anonymous payment is the favorite method of all

criminals - The key is to balance upholding individual

privacy with discouraging illicit activities - Counterfeit money is indistinguishable from

e-cash minted by an authorized issuing bank - If it is generate from compromised secret key

- High potential for undetected fraud

- Off-line stored-value payment system double

spending

15

How E-cash works

- E-cash is typically stored in an electronic

device - hardware token

- Secure processor and nonvolatile memory

- Load the token with money

- Connect to bank bank terminal and withdraw from

their own account - Similar to taking cash out of an ATM

- Make payment using e-cash

- Offline transaction

- Buyer's hardware token interface with seller's

device - Buyer's device decrease while seller's device

increase by the equivalent amount - Online transaction

- Buyer's hardware token connect to seller's bank

account - Buyer's device decrease while seller's account

increase by the equivalent amount

16

Securing E-Cash

- Main security concern

- Physical tampering of the device to add value

- Physically shield the device

- Protocol-based attack that mimics a paying device

- Replay attack

- To counter the replay attack secure

authentication protocol by using a key - Symmetric key Encryption

- Symmetric key shared by paying device and

receiving device - Bank issue a randomly generated master key to all

of its hardware devices - The symmetric key for the transaction is a

function of each device's unique identifier and

the master key

17

Securing E-Cash (continued)

- The receiving device can regenerate the symmetric

key based on unique identifier and the master key - Can trace and effectively blacklist compromised

key - To counter replay attack challenge (nonce)

response system - Public key Encryption

- Public key of receiving device for encryption

- Private key of paying device for signature

- To counter replay attack A challenge is signed

by paying device

18

Representing E-Cash

- Register-based cash

- A value stored in a counter of a hardware device

- To counter physical attack

- Encode the data stored in memory

- Electronic coins

- Discrete values of cryptographic tokens

- Each of some denomination

- A unique serial number is assigned to each coin

and signed by the issuing bank - A different signature is used for each currency

denomination - Each coin can only be used one time

- Recipient can no longer spend the coin but can

redeem it with the issuing bank for a new

electronic coin

19

eCash?

- eCash (www.ecash.com)

- A stored-value cryptographic coin system for

internet-based commerce - eCash can withdraw from consumer's bank account,

store in his computer, and transfer to another

person - Double spending

- Digital representation of money can be perfectly

duplicated - Counter double spending issuing bank

authentication - Verify the coins being used in a transaction has

not already been spent before while protect

payer's privacy - Key technique Blind signature

20

Blind Signature

- Sample steps in purchase of eCash

- Customer generate a note number of the eCash,

usually via a random number generator - Consumer mint his/her own eCash

- Bank digitally signs on the note number, after

getting money from customer, this create the

eCash - To protect consumer's privacy, the bank must be

infeasible to know the note number - Blind signature technique is used banks signs

on something he doesnt know the detail !!! - Customer got the eCash

- The value of coin is represented by the bank's

digital signature

21

Using eCash

- Main problem how to prevent double spending

- The bank is involved in order to authenticate

eCash - Trilateral transactions

- Customer sends 'notes' to merchant, (i.e., M)

- Customer does not sign the 'notes'

- Merchant sends 'notes' to bank

- Bank verifies that the 'notes' is not used before

- A global database for spent eCash

- Bank issues new e-cash to merchant, or credit

merchant's account - Bank records customer's 'notes' is spent

- Disadvantages

- needs a global database of spent e-cash, hard to

be cost-effective for micro-payment

22

Using eCash (continued)

- eCash provides the payer anonymity but not

anonymity of receiving eCash - Make purchasing illegal goods or services

possible over the internet with impunity - Cannot identify the purchaser

- Provides little incentive for selling illegal

goods or services - Purchaser knows the note number of the eCash

- Bank records the note number when the payee

authenticates them - The purchaser can indisputable "finger" a seller

of illegal goods and merchandise on the internet - The fingering also implicate the purchaser

23

Perfect Crime with eCash

- Bruce Schneier's description of a perfect crime

- An anonymous kidnapper takes a hostage

- The kidnapper then prepares a large number of

blinded coins - These are sent anonymously to the bank as a

ransom demand - The bank signs the coins due to the hostage

situation - The kidnapper demands that the signed blinded

coins be published in a public place such as a

newspaper or on television - This will prevent the pick-up being traced.

Nobody else can unblind the coins - The kidnapper can safely take the blinded coins

from the newspaper or television and save them on

computer - The coins are then unblinded and the kidnapper

now has a fortune in anonymous eCash

24

Next Session Highlights

- Internet Security

Recommended

CrystalGraphics Presentations