ACCOUNTING MANUAL PowerPoint PPT Presentation

Title: ACCOUNTING MANUAL

1

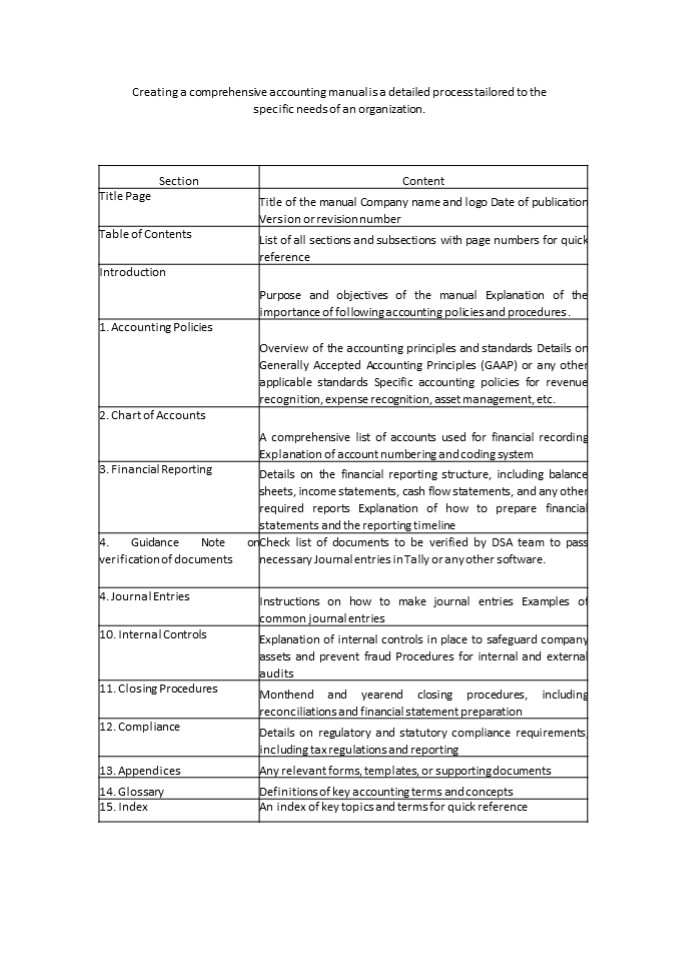

Creating a comprehensive accounting manual is a

detailed process tailored to the specific needs

of an organization.

Section Content

Title Page Title of the manual Company name and logo Date of publication Version or revision number

Table of Contents List of all sections and subsections with page numbers for quick reference

Introduction Purpose and objectives of the manual Explanation of the importance of following accounting policies and procedures .

1. Accounting Policies Overview of the accounting principles and standards Details on Generally Accepted Accounting Principles (GAAP) or any other applicable standards Specific accounting policies for revenue recognition, expense recognition, asset management, etc.

2. Chart of Accounts A comprehensive list of accounts used for financial recording Explanation of account numbering and coding system

3. Financial Reporting Details on the financial reporting structure, including balance sheets, income statements, cash flow statements, and any other required reports Explanation of how to prepare financial statements and the reporting timeline

4. Guidance Note on verification of documents Check list of documents to be verified by DSA team to pass necessary Journal entries in Tally or any other software.

4. Journal Entries Instructions on how to make journal entries Examples of common journal entries

10. Internal Controls Explanation of internal controls in place to safeguard company assets and prevent fraud Procedures for internal and external audits

11. Closing Procedures Monthend and yearend closing procedures, including reconciliations and financial statement preparation

12. Compliance Details on regulatory and statutory compliance requirements, including tax regulations and reporting

13. Appendices Any relevant forms, templates, or supporting documents

14. Glossary Definitions of key accounting terms and concepts

15. Index An index of key topics and terms for quick reference

2

ACCOUNTING MANUAL VERSION -I 2023

3

Sno Name of the section Page number

4

Purpose and Objectives of the Manual

1. Standardization To establish consistent

accounting practices and processes across the

organization. 2. Compliance To ensure

adherence to accounting standards and legal

regulations. 3. Internal Control To implement

effective internal controls for financial

transactions. 4. Training and Onboarding To

provide guidance for training and onboarding

staff. 5. Decision-Making To enable informed

decision-making through accurate financial

data. 6. Transparency and Accountability To

promote transparent financial reporting for all

DSA clients and shall increase internal

accountability. 7. Risk Management To

identify and manage the gaps to retention of

clients.

Importance of Following Accounting Policies and

Procedures

5

Accuracy and Reliability Ensures accurate and

reliable financial data.

1.

2. Legal Compliance Mitigates legal and

regulatory risks. 3. Consistency Facilitates

data comparison over time. 4. Fraud

Prevention Helps prevent and detect fraud. 5.

Accountability Promotes responsibility for

financial actions. 6. Decision-Making

Provides reliable data for informed decisions. 7.

Stakeholder Confidence Builds trust with

investors and creditors. 8. Risk Management

Includes strategies to manage financial risks.

GAAP Principle Definition

Revenue recognition principle Revenue should be recognized when it is earned and realized, regardless of when cash is received.

Expense recognition principle Expenses should be recognized in the period in which they are incurred, regardless of when cash is paid.

Matching principle Expenses should be matched with the revenues they generate.

Going concern principle Financial statements should be prepared on the

6

assumption that the business will continue to operate in the foreseeable future.

Monetary unit assumption Financial statements should be prepared in terms of a common unit of measurement, such as the INR.

Cost principle Assets and liabilities should be recorded at their historical cost.

Objectivity principle Financial statements should be prepared without bias or prejudice.

Full disclosure principle All material information should be disclosed in the financial statements.

Consistency principle The same accounting principles should be used from period to period.

Materiality principle Only material transactions and events should be recorded in the financial statements.

Conservatism principle Anticipated losses should be recorded, but anticipated gains should not be recorded.

CHAT OF ACCOUNTS

Below is the recommended chart of accounts of

Balance Sheets as per the Income Tax Act - I.

EQUITY AND LIABILITIES (1) Shareholders'

funds (a) Share capital (b) Reserves and

surplus (c) Money received against share

warrants (2) Share application money pending

allotment

7

(3) Non-current liabilities (a) Long-term

borrowings (b) Deferred tax liabilities

(Net) (c) Other Long-term liabilities (d)

Long-term provisions (4) Current

liabilities (a) Short-term borrowings (b)

Trade payables (c) Other current

liabilities (d) Short-term provisions II.

ASSETS Non-current assets (1) (a) Fixed

assets (i) Tangible assets (ii) Intangible

assets (iii) Capital work-in-progress (iv)

Intangible assets under development (b)

Non-current investments (c) Deferred tax

assets (net) (d) Long-term loans and

advances (e) Other non-current assets (2)

Current assets (a) Current investments (b)

Inventories (c) Trade receivables (d) Cash

and cash equivalents (e) Short-term loans and

advances f Other current assets Below is the

recommended chart of accounts of Profit Loss as

per the Income Tax Act - I. Revenue from

operations II. Other income III. Total

Revenue (I II) IV. Expenses a. Cost of

materials consumed b. Purchases of

Stock-in-Trade c. Changes in inventories of

finished goods work-in-progress and d.

Stock-in-Trade e. Employee benefits expense

8

f. Finance costs g. Depreciation and

amortization expense h. Other expenses V.

Profit before exceptional and extraordinary items

and tax (III - IV) VI. Exceptional items VII.

Profit before extraordinary items and tax (V -

VI) VIII. Extraordinary Items IX. Profit

before tax (VII - VIII) X. Tax expense a.

Current tax b. Deferred tax XI. Profit

(Loss) for the period from continuing operations

(VII - VIII) XII. Profit/(loss) from

discontinuing operations XIII. Tax expense of

discontinuing operations XIV. Profit/(loss)

from Discontinuing operations (after tax) (XII -

XIII) XV. Profit (Loss) for the period (XI

XIV) XVI. Earnings per equity share a.

Basic b. Diluted

Financial Reporting

Aspect Description/Steps

1. Balance Sheet (Statement of Financial Position) Provides a snapshot of financial position at a specific point in time. - Consists of assets, liabilities, and shareholders' equity. - Formula Assets Liabilities Shareholders' Equity.

2. Income Statement Shows profitability over a specific period. -

9

(Profit and Loss Statement) Includes revenue, expenses, and net income (or loss). - Formula Net Income Revenue -Expenses.

3. Cash Flow Statement Details cash generation and utilization over a period. - Divided into operating, investing, and financing activities.

4. Statement of Shareholders' Equity (Statement of Changes in Equity) Outlines changes in shareholders' equity over time. - Includes items like dividends, share issuances, and retained earnings changes.

5. Notes to Financial Statements (Financial Footnotes) Provides additional information and explanations related to the financial statements. - Includes details about accounting policies, contingencies, and other relevant information.

6. Management's Discussion and Analysis (MDA) A narrative section providing insights into financial performance and future outlook. -Discusses key financial results, challenges, and strategies.

How to Prepare Financial Statements

10

1. Collect Data Gather financial transactions, invoices, receipts, bank statements, and ledgers.

2. Record Transactions Enter and classify transactions into appropriate accounts (revenue, expenses, assets, liabilities).

3. Adjusting Entries Make adjustments (e.g., for depreciation, accruals, prepayments) to ensure financial accuracy.

4. Trial Balance Verify that debits and credits are equal by preparing a trial balance

5. Financial Statement Preparation Balance Sheet List assets, liabilities, shareholders' equity at a specific date. -Income Statement Summarize revenues and expenses for a given period. - Cash Flow Statement Prepare cash flows from operating, investing, and financing activities. - Statement of Shareholders' Equity Summarize changes in equity accounts over the period.

6. Additional declarations Provide additional explanations and analyses in the notes to financial statements

11

Financial Reporting Timelines

Reporting Timeline Reporting Timeline

1. Monthly Reporting (Internal) DSA has to prepare internal financial statements as per the DSA clients deadlines.

2. Financial statements DSA has to sent financial statements for auditor review before the end of 30th June every year.

3. Audit or Review External audit or review by an independent auditor to verify financial statement accuracy.

4. Financial statements infront of Board of Directors DSA has to sent financial statements for Board approval before the end of 31st August, every year

Guidance Note on Verification of documents

12

Revenue from Operations check list.

Checklist Item Description/Notes

Sales Invoices Verify details date, customer, description, quantity, price, total.

Sales Orders or Purchase Orders Review terms, including quantities, prices, and delivery terms.

Delivery Challans or Shipping Documents Confirm delivery details, including dates and quantities.

Customer Purchase Orders (if applicable) Cross-reference with agreed-upon terms.

Transportation Receipts or E-Waybills Verify shipping details, delivery dates, and quantities.

Gate receipt number (GRN) Which is very crucial to make a note on the receipt of goods into Factor and which shall help to count the inventory moment in and out of the factory

Credit Notes (if applicable) Review for returns or adjustments.

Debit Notes (if applicable) Verify additional charges or price adjustments.

Payment Receipts or Bank Statements Confirm payment receipts or bank deposits.

Sales Tax Invoices or GST Invoices Check for tax compliance and accurate calculations like tax rate whether charged correctly or not as per HSN code

Export Documents (if applicable) Review international sales documents (e.g., bills of lading, certificates of origin).

Revenue Recognition Policies Ensure adherence to revenue recognition policies.

Contracts or Agreements Review sales-related contracts for terms and conditions.

Accounting Software Entries Check accuracy of entries in the accounting software.

Internal Approvals Confirm managerial approvals or internal documentation.

Compliance Documents Ensure transactions comply with relevant regulations.

Communication with Sales Department Address discrepancies and resolve issues with the sales team if any

Periodic Reconciliation Verify sales figures and reconcile with records.

Sale invoice adjustment while receiving money For the purpose of accounts receivable and its ageing reports please do the Sale entry as per invoice number and its adjustment towards receipt to be done bill wise so that we can get the automated and correct account receivable ageing report.

13

It is for GST output and respective GST input

treatment, this recognition of transaction is

very much required.

Sample Sale or Normal Sales

Complianc e Documents Ensure transactions comply with relevant regulations. Hyper link for lates TDS and TCS rates

1 Tcs to be deducted on sale if applicable https//incometaxi ndia.gov.in/Pages/i -am/tax-

1 Tcs to be deducted on sale if applicable collector.aspx?kT CS20Rates

2 GST rates to be checked as per HSN Code and make sure the respective goods shall fall under correct HSN code https//cbic- gst.gov.in/gst- goods-services- rates.html

3 If it is a export sale make sure to receive all Export documents as below-

3.1 Export Invoice Date

3.2 Invoice Number

3.3 Seller's Information

3.4 Name and address of the exporter (seller).

3.5 Contact details, including email and phone number.

3.6 Buyer's Information

3.7 Name and address of the buyer (importer).

3.8 Contact details, including email and phone number.

3.9 Shipping Information

3.10 Port of loading (departure) and port of discharge (arrival).

3.11 Mode of transportation (e.g., sea, air, land).

3.12 Vessel or flight details (if applicable).

3.13 Incoterms (shipping terms, e.g., FOB, CIF) agreed upon.

14

3.14 Description of Goods

3.15 Detailed description of the goods being exported.

3.16 Include quantity, unit of measure, and item numbers (if applicable).

3.17 Detailed description of the goods being exported.

3.18 Unit Price

3.19 Price per unit of the goods.

3.20 Currency of the transaction.

3.21 Total Invoice Value

3.22 Total value of the goods being exported.

3.23 Payment Terms

3.24 Specify the agreed-upon payment terms (e.g., Letter of Credit, advance payment, open account).

3.25 Currency of Payment

3.26 Currency in which payment should be made.

3.27 Country of Origin

3.28 The country where the goods were manufactured or produced.

3.29 Country of Final Destination

3.30 The country to which the goods are being shipped.

3.31 Packaging Details

3.32 Describe how the goods are packaged and the number of packages.

3.33 Gross and net weights of each package.

3.34 Shipping Marks and Numbers

3.35 Marks and numbers on the packages for identification.

3.36 Insurance Information

15

3.37 If insurance is included in the transaction, provide details of the insurance coverage.

3.38 Incoterms

3.39 Clearly state the agreed-upon Incoterms (shipping terms) that define the seller's and buyer's responsibilities in the shipment.

3.40 Declaration of Origin

3.41 A statement confirming the origin of the goods (e.g., "The goods originate from country of origin").

3.42 Certifications and Documents to be verified

3.43 List any required certificates or documents, such as Certificate of Origin or Inspection Certificates.

3.44 Bank Details

3.45 Bank account details for payment, including name and address of the seller's bank.

3.46 Authorized Signature

3.47 A signature by an authorized representative of the exporter or seller.

3.48 Additional Notes/Comments

3.49 E-BRC to be get it issued at the earliest possible and to be vigilant on export receivable date limits as per FEMA. https//www.rbi.or g.in/commonperso n/English/Scripts/N otification.aspx?Id 851

16

Other Income check list. Other Income check list. Other Income check list.

Type of Other Income Documents to Verify Notes If any client to client

Rental Income Lease agreements, Rental receipts, Expenses related to rental property

Interest Income Bank statements, Interest certificates, Loan or investment documents

Dividend Income Dividend statements, Records of dividend received

Capital Gains Sale/purchase agreements, Brokerage statements

Royalty Income Contracts or agreements, Documentation of royalty income

Pension Income Pension statements, Retirement plan distributions

Annuity Income Annuity contracts, Annuity payment records

Duty drawback income Shipping bills to be cross verified for duty draw back income

Remission of Duties or Taxes on Export Products Scheme (RoDTEP) / MEIS Scheme RoDTEP and MEIS cannot be claimed simultaneously.

Miscellaneous Income Any other income sources, associated documentation

17

Expense Recognition Policies Simple Explanation

Identification of Expenses We figure out and list all the things we spent money on.

Timing of Expense Recognition We determine when to count the expenses as costs in our books.

Matching Expenses to Revenue We link expenses to the money we made when it's related.

Accrual Basis vs. Cash Basis We decide if we count expenses when we pay or when we owe.

Prepaid Expenses Some costs we pay upfront, so we spread the cost over time.

Depreciation of Assets We divide the cost of long-lasting items over their lifetime.

Amortization of Intangibles Similar to depreciation but for non-physical things we own.

Recognition of One-time Costs Unique or unusual costs get recognized when they happen.

Contingent Liabilities We record potential costs if they're likely and measurable.

Consistency in Expense Policies We stick to the same rules to keep our financials clear.

Disclosure of Policy Changes If we change how we recognize expenses, we tell everyone.

18

Purchase Invoice Entry Checklist Description

Supplier Information Check that you have the supplier's name, address, and contact details.

Invoice Date Verify the date on the invoice is accurate.

Invoice Number Confirm the unique invoice number.

Purchase Description Record a clear description of the goods or services purchased.

Quantity Ensure the quantity of items purchased is correctly stated.

Unit Price Verify the price per unit for each item.

Total Amount Calculate and double-check the total amount for the invoice.

Taxes and Discounts Include any applicable taxes, discounts, or rebates.

Payment Terms Record the agreed-upon payment terms (e.g., net 30, due on receipt).

Payment Due Date Note the due date for payment based on the payment terms.

Terms and Conditions Document any specific terms and conditions mentioned on the invoice.

Invoice Currency Ensure the currency of the invoice is clear and accurate.

Compliance with Regulations Confirm that the invoice complies with tax and regulatory requirements.

Review for Accuracy Carefully review the invoice for any errors or discrepancies.

Approval and Authorization Ensure the invoice is authorized for payment by the appropriate parties.

Attach Supporting Documents Include any supporting documents like purchase orders or delivery receipts.

Sample purchases or purchase being done for resale It is for GST input treatment, this recognition of transaction is very much required.

Credit Notes (if applicable) Review for returns or adjustments.

Debit Notes (if applicable) Verify additional charges or price adjustments.

19

List of Direct expenses check list

Sno Name of the Direct expenses Documents to be verified

1 Cost of Goods Sold (COGS) - Invoices and receipts for purchased goods.,- Records of returns or allowances.

2 Purchase Cost - Invoices from suppliers.,- Purchase orders (if used).,- Delivery receipts or packing slips.

3 Direct Labor Cost - Employee time records or timecards.,-Payroll records showing wages paid to direct labor employees.

4 Factory Overhead - Utility bills, rent or lease agreements for the factory.,- Maintenance and repair invoices for factory equipment.

5 Freight and Transportation - Freight bills or invoices.,- Shipping contracts or agreements.,- Records of transportation expenses.

6 Customs Duties - Customs declarations and related documents.,- Invoices from customs agents or authorities.

7 Packaging Costs - Invoices from packaging material suppliers.,- Records of packaging materials used.

8 Import Fees Invoices for import fees and charges.,-Customs-related documents.

9 Quality Control Costs - Invoices or records of quality control services.,- Reports on quality control inspections.

10 Cost of Raw Materials - Invoices and receipts for raw material purchases.,- Records of raw material inventory.

11 Work-in-Progress Costs - Records showing the value of goods in progress.,- Records of labor and material costs for work in progress.

12 Stock Handling Costs - Invoices for warehouse or storage costs.,-Records of inventory handling expenses.

13 Cost of Production - Records showing the total cost of production.,- Detailed records of labor and material costs.

14 Cost of Subcontracting If any Agreements with subcontractors.,-Invoices or records of payments to subcontractors.

15 Cost of Commissions - Agreements with salespersons or agents.,-Commission records and invoices.

16 Raw Material Handling Costs - Invoices for handling and transportation of raw materials.,- Records of raw material storage costs.

20

17 Direct Freight Costs 18 Customization Costs - Freight invoices related to the movement of goods.,- Records of direct freight expenses. - Invoices for customization services.,-Records of expenses incurred for customization.

List of Employee benefit check list

Document Description and Purpose

Employee Benefits Policy company's policy outlining employee benefits, including details of the benefits offered, eligibility criteria, and the company's contribution.

Employee Records Detailed records of all employees, including their personal information, job title, hire date, and eligibility for benefits.

Payroll Records Payroll data, including salaries, wages, bonuses, and other compensation details for each employee.

Benefit Plan Documents Legal documents that define the terms and conditions of benefit plans, such as health insurance, retirement plans, and stock options.

Enrollment Forms Completed forms that employees use to enroll in benefit plans and make selections regarding coverage and contributions.

Benefit Contribution Records Records of the employer's and employee's contributions to benefit plans, including insurance premiums and retirement fund contributions.

Insurance Contracts Copies of insurance policies, including health, dental, life, and disability insurance policies, outlining coverage and terms.

Retirement Plan Reports Reports on retirement plan contributions, investment performance, and account balances for employees participating in retirement plans.

Declaration Forms Signed documents should be with DSA in respect of employee optiong old regime of tax or new regime of tax and saving details if any along with receipts

Benefit Statements Statements provided to employees detailing their benefit coverage, contributions, and costs for a specific period.

Employee Communications Internal communications to employees about benefit changes, open enrollment, and other benefit-related information.

Termination and Leave Records Records related to employee terminations, leaves of absence, and any associated benefit changes.

21

Benefit Expense Reports Reports detailing the total cost of providing employee benefits, including healthcare, retirement, and other benefit expenses.

Compliance and Regulatory Filings Documents required to ensure compliance with Professional tax returns, Provident fund returns, ESI returns and Form 16 and ITR if required

Audit and Verification Records Documents used for internal and external audits to verify the accuracy and compliance of benefit expenses.

Employee Benefit Summary A summary of employee benefits offered, eligibility requirements, and cost-sharing arrangements.

Employee Handbook The section of the employee handbook dedicated to benefits, outlining policies and procedures.

Benefit Program Contracts Contracts with third-party benefit providers and vendors, including agreements and terms of service.

Privacy and Security Documents Documents outlining the protection of sensitive employee benefit data, including his healthcare information if received by DSA for health care policy

Checklist for Finance cost

Document Type Description

Debt Agreements and Loan Documents Examine loan agreements, bond indentures, and credit facilities for terms, interest rates, covenants.

Bank Statements and Payment Records Confirm actual interest payments from bank statements and payment records.

Tax Returns Check for interest expense deductions on the company's tax returns.

Interest Rate Agreements and Derivatives Examine interest rate swap agreements, hedges, or derivative contracts.

Compliance Reports Ensure compliance with debt covenants and contractual obligations affecting finance costs. like ROC, RBI filings like ECB returns , directors loan etc

External Audit Reports Consider external audit reports and internal audit findings related to finance cost verification.

Regulatory Filings Check regulatory filings with relevant authorities for consistency in reporting finance costs.

Documentation of Finance Cost Calculation Review internal documentation of finance cost calculation methods for accuracy and consistency.

22

Document Type Description

Fixed Asset Register Analyze the company's fixed asset register for details on the cost, useful life, and disposal of assets.

Depreciation rates Check the Companies Act for depreciation rates https//www.mca.g ov.in/Ministry/notifi cation/pdf/AS 6.pdf

Tax Returns Check for depreciation expense deductions on the company's tax returns.

Management Reports and Internal Records Analyze internal management reports and records related to depreciation for consistency with financial statements.

Board Minutes and Resolutions Review board minutes and resolutions related to the acquisition or disposal of fixed assets.

Regulatory Filings Check regulatory filings with relevant authorities for consistency in reporting depreciation costs.

Miscellaneous Expenses Checklist

Expense Category Description Documents to Verify

Utilities Expenses Expenses related to utility services (electricity, water, gas). Utility bills, payment records.

Rent and Lease Expenses Costs associated with renting or leasing office space and equipment. Lease agreements, rent invoices.

Office Supplies Expenses for office materials, stationery, and consumables. Invoices for office supplies.

Repair and Maintenance Costs for maintaining and repairing equipment, facilities, and vehicles. Maintenance contracts, repair invoices.

Legal and Professional Fees Fees paid for legal, accounting, consulting, and professional services. Legal and professional service invoices.

23

Insurance Expenses Premiums for various insurance policies (liability, property, health, etc.). Insurance policies, premium payments.

Advertising and Marketing Expenses for advertising campaigns, marketing materials, and promotions. Advertising and marketing contracts, invoices.

Travel and Entertainment Costs for business-related travel, meals, and entertainment. Expense reports, travel receipts.

Bank Charges and Interest Fees and interest paid on loans, credit lines, and banking services. Bank statements, loan agreements.

Depreciation and Amortization Non-cash expenses accounting for the wear and tear of assets and intangible assets. Asset register, depreciation calculations.

Taxes (Other Than Income Tax) GST and any other incidental taxes Tax returns,tax assessment notices.

Miscellaneous Expenses Various small expenses or items that don't fit into specific categories. Receipts and supporting documentation.

Charitable Contributions Donations made to charitable organizations or causes. Receipts and confirmation from charities.

Bad Debt Expenses Provisions for doubtful accounts and unrecoverable debts. Ageing reports, debt collection records.

Exchange Rate Losses Losses due to fluctuations in currency exchange rates (if applicable). Currency exchange records, financial statements.

Document Type Description

Shareholder Agreements Review shareholder agreements to understand the terms of share issuances and restrictions on share transfers.

Articles of Incorporation Examine the company's articles of incorporation to determine authorized share capital and classes of shares.

24

Board Resolutions Verify board resolutions approving the issuance or buyback of shares and setting the terms and conditions if any

Share Certificates Examine share certificates for issued shares to confirm the number, class, and ownership of shares.

Share Register Review the share register to track ownership changes and ensure it's uptodate and accurate.

Statutory Filings Check with the relevant government authorities for any required filings related to share capital changes.

Shareholder Records Confirm shareholder records and ensure they align with the issued share capital.

Financial Statements Review financial statements for disclosure of share capital and any changes in share capital during the reporting period.

Annual Reports Examine annual reports for information on share capital and changes to the capital structure.

Share Subscription Agreements Analyze share subscription agreements for details of shares subscribed to and terms of payment.

Auditor's Reports Consider auditor's reports to validate the accuracy of share capital entries in financial statements.

Stock Ledger Verify the stock ledger to ensure proper recording of share issuances and repurchases.

Share Premium Account Examine the share premium account to confirm the amount received in excess of the nominal value of shares.

Share Buyback Agreements Review share buyback agreements if the company is repurchasing its own shares.

Legal Counsel Opinions Seek legal counsel opinions to ensure compliance with relevant laws and regulations.

Share Capital Ledger Verify the share capital ledger, including the nominal value and paidup capital of each share.

Registrar of Companies Filings Ensure compliance with registrar of companies' requirements regarding share capital.

Loan Agreements Examine loan agreements that involve the use of share capital as collateral or in connection with financing.

25

Document Type Description

Financial Statements Review the income statement, balance sheet, and cash flow statement to identify and verify the specific reserves and surplus accounts.

Shareholder Agreements Examine any shareholder agreements that specify the treatment of reserves and surplus and any restrictions on their distribution.

Board Resolutions Verify board resolutions authorizing the allocation of profits to specific reserves and surplus accounts.

Articles of Incorporation Confirm that the allocation of profits to reserves and surplus complies with the company's articles of incorporation.

Audit Reports Consider the auditor's reports to ensure that the allocation of profits to reserves and surplus is in accordance with generally accepted accounting principles.

Dividend Declarations Check for records of dividend declarations and ensure that dividends are declared and paid in compliance with applicable laws and regulations.

Financial Statements (Historical) Review historical financial statements to trace the evolution of reserves and surplus over time.

Annual Reports Examine annual reports to disclose the changes in reserves and surplus over the fiscal year.

Dividend Vouchers Verify dividend vouchers and distribution records to ensure the accurate allocation of profits.

Tax Returns Check for previous tax returns to confirm the treatment of reserves and surplus for tax purposes.(Losses if any)

Transfer Entries Review transfer entries in the books of accounts that document the allocation of profits to specific reserves and surplus accounts.

26

Loan Agreements Examine loan agreements that may specify conditions related to the allocation of profits to reserves and surplus.

Registrar of Companies Filings Ensure that any changes related to reserves and surplus are correctly filed with the registrar of companies.

Document Type Description

Share Warrant Agreement Review the share warrant agreement, which outlines the terms and conditions of the share warrant issuance.

Board Resolutions Verify board resolutions authorizing the issuance of share warrants and setting the terms and conditions.

Shareholder Agreements Examine any shareholder agreements that may have provisions related to the issuance and transfer of share warrants.

Articles of Incorporation Confirm that the issuance of share warrants complies with the company's articles of incorporation.

Warrant Certificates Verify warrant certificates, ensuring that they are properly executed and indicate the number of warrants issued.

Share Register Confirm the recording of share warrants in the share register and that it reflects the ownership and transfer of warrants.

Money Receipts Examine money receipts or bank records to verify the actual receipt of funds against the share warrants.

Audit Reports Consider auditor's reports to ensure that the issuance and receipt of funds for share warrants comply with accounting standards.

Legal Counsel Opinions Seek legal counsel opinions to ensure compliance with relevant laws and regulations when issuing share warrants.

Financial Statements Review financial statements to disclose the issuance of share warrants and the funds received against them.

27

Registrar of Companies Filings Ensure that any changes related to share warrant issuances and receipts are correctly filed with the registrar of companies.

Transfer Entries Examine the transfer entries in the books of accounts that document the issuance and receipt of funds for share warrants.

Loan Agreements Review loan agreements if they involve the use of share warrants as collateral or in connection with financing.

Bank Statements Confirm the funds received against share warrants by examining bank statements and transaction records.

Document Type Description

Share Application Forms Review share application forms submitted by investors.

Bank Statements Verify bank statements to confirm that application money has been received and is held in a designated bank account.

Board Resolutions Verify board resolutions authorizing the receipt of share application money pending allotment.

Prospectus or Offering Document Examine the prospectus or offering document for details on the offer and allotment of shares.

Registrar of Companies Filings Ensure that relevant filings with the registrar of companies regarding share application money are complete and accurate.

Escrow Agreement Review the escrow agreement, if applicable, to confirm that application money is held in accordance with the agreement's terms.

Legal Counsel Opinions Seek legal counsel opinions to ensure compliance with relevant laws and regulations related to the receipt of application money.

Audit Reports Consider auditor's reports to ensure that the receipt and handling of share application money comply with accounting standards.

Shareholder Register Confirm that the share application money received is accurately recorded in the shareholder register.

Bank Confirmation Letters Obtain bank confirmation letters to confirm the amount of application money held in the bank account.

28

Investor Communications Review investor communications, such as acknowledgment letters, to ensure that investors are informed about the receipt of application money.

Bank Receipts Verify bank receipts for the deposit of application money and that they correspond to the amounts mentioned in application forms.

Share Allotment Documents Examine documents related to share allotment to ensure that the application money is appropriately accounted for upon allotment.

Transfer Entries Check transfer entries in the books of accounts to confirm the proper accounting treatment of application money.

Share Application Register Review the share application register to track the receipt and handling of application money.

Financial Statements Review financial statements to disclose the amount of share application money pending allotment.

Document Type Description

Loan Agreements Review loan agreements and credit facility documents for terms, interest rates, and repayment schedules.

Bond Issuance Documents Examine bond issuance documents, including indentures, prospectuses, and terms of the bond issue.

Lease Agreements Verify lease agreements for terms and conditions, such as lease payments and lease periods.

Financial Statements Review financial statements to identify and confirm the existence and accuracy of noncurrent liabilities.

Debenture Certificates Examine debenture certificates and other debt instrument documents to validate the amount and terms of the debentures.

Board Resolutions Verify board resolutions authorizing the issuance or arrangement of noncurrent liabilities.

29

Shareholder Agreements Examine any shareholder agreements that may affect the issuance of noncurrent liabilities.

Maturity Schedules Confirm the maturity dates and repayment schedules of noncurrent liabilities.

Legal Counsel Opinions Seek legal counsel opinions to ensure compliance with relevant laws and regulations when issuing noncurrent liabilities.

Audit Reports Consider auditor's reports to ensure that the noncurrent liabilities are accounted for in accordance with accounting standards.

Prospectus or Offering Document Review prospectuses or offering documents if applicable, especially in the case of publicly issued bonds.

Insurance Policies Verify insurance policies that may be used as collateral for noncurrent liabilities.

Amortization Schedules Examine amortization schedules for loans and bonds to track the allocation of principal and interest payments.

Tax Records Check tax records for any deductions or tax implications related to noncurrent liabilities.

Registrar of Companies Filings Ensure that relevant filings related to noncurrent liabilities are correctly submitted to the registrar of companies.

Financial Covenants Review any financial covenants or obligations associated with noncurrent liabilities.

Escrow Agreements Examine escrow agreements, if used, to ensure that funds or assets are held as collateral for noncurrent liabilities.

Document Type Description

Accounts Payable Records Review accounts payable records, including invoices and bills from suppliers.

30

Purchase Orders Verify purchase orders and procurement documents related to current liabilities.

Loan Agreements Examine loan agreements for shortterm loans, lines of credit, or other financial liabilities.

Supplier Agreements Confirm the terms and conditions of supplier agreements, including payment terms and credit agreements.

Credit Agreements Review credit agreements with financial institutions or lenders for shortterm credit.

Financial Statements Identify and confirm the existence and accuracy of current liabilities in the financial statements.

Tax Records Check tax records for any tax liabilities that should be recognized as current liabilities.

Salaries and Wages Records Verify payroll records and accruals for salaries, wages, and employee benefits.

Utilities Bills Examine utility bills and other operational expenses that constitute current liabilities.

Accruals and Provisions Review accruals and provisions for estimated expenses such as warranty claims, legal disputes, and bonuses.

Interest Payable Records Confirm interest payable records for shortterm interest obligations, including interest on loans and credit lines.

Dividend Declarations Check records of dividend declarations, as declared dividends are a current liability until paid.

Bank Statements Verify bank statements and transaction records for outstanding checks, drafts, or other financial instruments.

Legal Notices and Claims Examine legal notices and pending claims that may result in recognized current liabilities.

Credit Card Statements Review credit card statements and outstanding balances that are considered current liabilities.

31

Utility Usage Records Confirm utility usage records and accruals for utilities that have been consumed but not yet billed.

Employee Benefit Plans Verify liabilities related to employee benefit plans, such as health insurance and retirement contributions.

Trade Payables Aging Report Analyze the trade payables aging report to assess the aging of outstanding payables and due dates.

Supplier Confirmations Request supplier confirmations to verify the outstanding balances and terms with suppliers.

Bank Confirmation Letters Obtain bank confirmation letters to validate outstanding loans or credit balances.

Insurance Claims Records Examine records related to insurance claims and any corresponding liabilities.

Customer Advances Review customer advances or deposits, which may be classified as current liabilities until goods or services are delivered.

Document Type Description

Purchase Invoices and Agreements Review purchase invoices and purchase agreements for the acquisition of noncurrent assets.

Title Deeds and Ownership Documents Examine title deeds, ownership documents, or certificates of title for real property or land assets.

Lease Agreements Verify lease agreements for assets that are leased, such as real estate, equipment, or vehicles.

Appraisal and Valuation Reports Consider appraisal and valuation reports to determine the fair value of noncurrent assets.

Depreciation Schedules Review depreciation schedules to track the historical and projected depreciation of assets.

32

Insurance Policies Confirm insurance policies covering noncurrent assets, including coverage amounts and terms.

Maintenance and Service Contracts Examine maintenance and service contracts for assets that require periodic servicing or maintenance.

Financial Statements Identify and confirm the existence and value of noncurrent assets in the financial statements.

Warranty Documents Check warranty documents that may be associated with certain noncurrent assets, such as machinery or equipment.

Transfer and Ownership Records Verify transfer and ownership records when noncurrent assets change hands or are transferred.

Board Resolutions Confirm board resolutions authorizing the acquisition or disposition of noncurrent assets.

Asset Register Review the company's asset register to ensure that all noncurrent assets are properly documented and tracked.

Environmental Compliance Records Examine records related to environmental compliance for assets that may have environmental impact.

Loan Agreements and Finance Records Check loan agreements and finance records for assets purchased with financing.

Equipment Manuals and Documentation Verify equipment manuals and documentation for machinery and equipment assets.

Audit Reports Consider auditor's reports to ensure that noncurrent assets are accounted for in accordance with accounting standards.

Legal Counsel Opinions Seek legal counsel opinions to ensure compliance with relevant laws and regulations regarding noncurrent assets.

Registrar of Companies Filings Ensure that relevant filings related to noncurrent assets are correctly submitted to the registrar of companies.

33

Safety and Inspection Reports Examine safety and inspection reports for assets that require safety compliance and regular inspections.

Customs and Import Records Verify customs and import records for assets that have been imported from other countries.

Land Surveys and Zoning Documents Confirm land surveys and zoning documents for real estate assets.

Document Type Description

Purchase Invoices and Receipts Review purchase invoices and receipts for current assets acquired.

Inventory Records Confirm the accuracy of inventory records for goods and materials.

Bank Statements Verify bank statements and transaction records for cash and cash equivalents.

Customer Invoices and Sales Agreements Examine customer invoices and sales agreements for accounts receivable.

Investment Statements Review investment statements for current investments, such as stocks and bonds.

Supplier Agreements Confirm the terms and conditions of supplier agreements, including payment terms and credit agreements.

Valuation Reports Consider valuation reports for assets that require fair value assessments.

Loan Agreements Check loan agreements for shortterm loans, lines of credit, or other financial assets.

Financial Statements Identify and confirm the existence and value of current assets in the financial statements.

34

Prepaid Expense Records Examine prepaid expense records, such as prepaid insurance or prepaid rent.

Tax Records Verify tax records for any tax refunds or tax assets that are recognized as current assets.

Deposit Receipts Confirm deposit receipts for cash deposits or security deposits held.

Client Contracts and Agreements Review client contracts and agreements that relate to billed or unbilled revenue.

Employee Expense Reports Verify employee expense reports and reimbursement claims.

Audit Reports Consider auditor's reports to ensure that current assets are accounted for in accordance with accounting standards.

Legal Counsel Opinions Seek legal counsel opinions to ensure compliance with relevant laws and regulations regarding current assets.

Registrar of Companies Filings Ensure that relevant filings related to current assets are correctly submitted to the registrar of companies.

Cash and Bank Reconciliation Reports Review cash and bank reconciliation reports to ensure accuracy in cash and cash equivalents accounts.

Credit Card Statements Examine credit card statements and outstanding balances that are classified as current assets.

Customer Advance Records Confirm customer advance records and deposits that are classified as current assets.

Cash Flow Projections Analyze cash flow projections that may include forecasts of future cash receipts from current assets.

Supply Agreements and Contracts Review supply agreements and contracts related to the procurement of current assets.

Instructions to pass Journal entries

35

Sno Name of the point to be checked Description of work

1. Date Write the transaction date.

2. Account Title Identify the accounts involved (at least one debit and one credit

3. Debit Record the amount in the debit column for the account receiving value (increases assets and expenses, decreases liabilities and equity).

4. Credit Record the amount in the credit column for the account giving value (increases liabilities and equity, decreases assets and expenses).

5. Description Provide a brief explanation of the transaction.

6. Calculate Totals Ensure total debits equal total credits.

7. Review Carefully review the entry for accuracy and adherence to accounting principles.

8. Post to General Ledger Transfer the entry to the appropriate accounts in the general ledger.

9. Prepare Trial Balance Verify that the trial balance shows equal total debits and credits.

10. Generate Financial Statements Use the general ledger data to create financial statements.

Examples of Journal entries-

Nidhi shall do it

36

Internal Controls for Book-Keeping and client

handling

Aspect Instructions

Transaction Identification Identify the financial transaction in question.

Document Verification Refer to the accounting manual to confirm the checklist of required documents for the specific transaction.

Foreign Exchange Transactions If the transaction involves foreign exchange (e.g., exports or imports), ensure entry to be review by the Assistant Manager.

Balance Sheet Transactions Transactions related to balance sheet items must be verified by the Manager.

Client Queries All client queries should be discussed with the Manager. After the Manager's review, the response

37

Aspect Instructions

can be sent to the client.

Employee Declarations Annually, obtain signed employee declarations and confirm in writing with the client whether they prefer the new or old taxation regime.

Document Storage Safely store final receipts of employee investment proofs in a designated OneDrive folder.

Email Management Save important client emails in a dedicated Outlook folder named after the respective client name.

Client Information Management Follow the policies set by DSA to save all client information in a designated OneDrive folder.

Assistant Manager Responsibilities Assistant Managers are responsible for various monthly tasks, including MIS, signed financials, audit workings, tax-related returns, and other important matters, all to be saved in a OneDrive folder.

Non-Compliance Consequences Failure to follow the above procedures will result in accountability for Assistant Managers and ultimately, the Manager of CAS (Client Accounting Services).

Client Engagement Letter Review the client engagement letter with DSA and ensure that all listed services are understood and agreed upon.

Additional Services If additional services are requested or identified, inform the Assistant Manager promptly.

Client User ID and Passwords Provide clients with their user IDs and passwords related to regulatory departments.

Government Notices Associate should immediately inform the Assistant Manager upon receiving any notice from government authorities.

Manager-Client Communication Manager should communicate any government notices to clients, if applicable on the second day of the receipt of notice.

Reconciliation Regularly reconcile bookings with other records, such as invoices and payments, to identify discrepancies and errors.

Monthly MIS Review Assistant Managers verify monthly MIS reports, followed by a final review by the Manager.

Client Calls Assistant Managers and Managers must attend all client calls.

Meeting Agenda Discuss the meeting agenda for client calls among the team before the call.

Quarterly Reconciliations Manager is responsible for verifying reconciliations every quarter for each client.

38

Aspect Instructions

Time Tracking Ensure every employee fills out a timesheet detailing time spent on client work.

Time-sheet Supervision If immediate supervisors do not receive timesheets, they must provide written explanations to management. After two failures, the third instance is to be decided by management.

Discrepancy Resolution Implement a process to investigate and resolve discrepancies, minimizing the impact of fraud or errors.

Non-Compliance Consequences In cases of non-compliance, associates, Assistant Managers, and Managers should provide written explanations as appropriate.

In the first week of second week of November

client should be informed with the following

email. Subject Request for Your Input on

Upcoming Fiscal Year Updates Dear Client's

Name, I trust this message finds you well. As we

approach the upcoming fiscal year, we are

reaching out to request your valuable input and

updates regarding various aspects of your

organization's financial operations. Your

insights and updates are crucial in ensuring that

we continue to provide you with the best possible

service and support. Here are some specific areas

where your input would be greatly appreciated 1.

Change in Accounting Codes If there are any

planned changes or updates to your accounting

codes, kindly inform us. This will help us ensure

that our systems and records remain synchronized

with your financial structure. 2. MIS Format

Changes If there are any modifications in your

Management Information System (MIS) formats,

sharing these with us will enable a

seamless transition and reporting process.

39

3. Changes in Board of Directors or Approval

Authorities If there are any changes

in your board of directors or approval

authorities, please keep us informed. This will

help us maintain accurate records and ensure

compliance. 4. Authorization of Bank Payments

Any alterations in the individuals or entities

authorized to initiate, approve, or oversee bank

payments on behalf of the organization should be

communicated to us. This includes changes in

signatories, approval processes, or any

adjustments in the personnel responsible for

handling financial transactions. Accurate and

up-to-date information in this area is essential

for maintaining the integrity of your financial

operations and ensuring that all payments are

properly authorized. 5. Purchase of Fixed

Assets If there are any changes or developments

in your organization's fixed asset procurement,

we request that you inform us promptly. This

includes information about new acquisitions,

disposals, or significant alterations to the

existing fixed asset portfolio. This notification

helps us in maintaining an accurate record of

your organization's assets, facilitating

financial planning, and ensuring compliance with

relevant accounting and tax regulations. 6.

Alterations in Business Activities or

StrategiesIf your organization intends to extend

its services nationwide in India or is

considering the adoption of new strategies such

as international trade (export/import) or

globalizing its business operations, we kindly

request that you provide us with these details.

This information is crucial for us to assist you

in addressing any potential regulatory

obligations or necessary registrations from an

Indian company

perspective. Our team at DSA is ready to offer

prompt support.

40

Keeping us updated on these matters allows us to

provide you with efficient financial

management and support. Please do not hesitate to

reach out if you have any questions or require

further assistance in these areas. Your proactive

communication on these matters will enable DSA to

plan and adapt our services accordingly, ensuring

a smooth and compliant transition into the new

fiscal year. If you have any updates or

information to share, please feel free to respond

to this email or get in touch with your dedicated

account manager. Your cooperation in providing

this information is highly appreciated and

contributes to our ongoing commitment to

delivering the best possible support for your

financial needs. Thank you for your continued

partnership with DSA. We look forward to hearing

from you and working together to make the

upcoming fiscal year a successful one. Warm

regards, Your Name Your Title Monthly and

Qtly Closing Procedures List of

Reconciliations-

Sno Name of the Report Date of the Report

1. Monthly closing report in DSA client format Data should be ready for reporting by last day of the month and MIS format to be planned in linking and fixed formats only data to be incorporated rest of the files

41

and figures automated.

2. Qtly TDS TCS reconciliation 30th June, 30th Sept, 31st Sept, 31st March.

3. Qtly PF and ESI reconciliation 30th June, 30th Sept, 31st Sept, 31st March.

4. Qtly Payroll reconciliation 30th June, 30th Sept, 31st Sept, 31st March.

5. Qtly Professional tax reconciliation 30th June, 30th Sept, 31st Sept, 31st March.

6. Qtly GSTR-1, 3B , reconciliation 30th June, 30th Sept, 31st Sept, 31st March.

7. Qtly Reconciliation between, purchase and 30th June, 30th Sept, 31st Sept,

GSTR3B and Electronic ledger input balance. 31st March.

8. Qtly Form 26As reconciliation 30th June, 30th Sept, 31st Sept, 31st March.

Check list of the workings and reconciliations to

be done for the purpose of audit

S. No. Description

General General

1 Draft financials FY 2023-24 as Schedule 3

2 General Ledger, TB (Opening, debit, credit, closing) and should be matched with the dump

3 Related Party Transactions (RPT) balances confirmation

4 Forex rate chart used during the year

5 TP study (if any)

Share Capital Share Capital

1 Signed List of directors Shareholders as on 31-03-2024

2 DIR-8 For all directors as on 31-03-2024

3 MBP-1 for all directors as on 31-03-2024

42

4 Signed minutes of the board meeting conducted during the year.

5 Secretarials forms filed during the FY 2023-24

6 Signed minutes of AGM held during the FY 2023-24

7 Form AOC-4 and challan details of FY 2022-23

8 Form MGT-7 and challan details, FY 2022-23

9 Minutes of subsequent Board Meeting from 1 April 2023 to FS date

Long term Short Term Borrowings Long term Short Term Borrowings

1 ECB Loan Details (updated)

2 ECB return March 2024

3 Parent Loan Agreement (addendum, if any to the same)

4 Interest working of both loans

Long term provision Short term provision Long term provision Short term provision

1 Acturial report ( Gratuity and leave encashment )

2 Data sent to actuary for the purpose of acturial valuation

3 HR policy-Grautity

Trade Payables Trade Payables

1 MSME return

2 Details of new MSME added, if any (MSME certificates)

3 Balance confirmation of trade payables and advance paid to creditors once we receive the item no 4 then we share the sample for the confirmation required

4 Invoice wise ageing along with MSME and non MSME bifurcation and list of credit period allowed by the vendors

5 DSA agreement -Updated

Other Current Liabilities Other Current Liabilities

1 TDS, TCS , PT related challans, returns, workings

2 Employee related payables working

3 GST returns 1 , 3B, electronic credit ledger and electronic cash ledger

4 TDS conso File for all quarters

Trade Receivable Trade Receivable

1 Ageing as per schedule III

2 Balance confirmation as on 31 March 2024

3 Provision for bad debts, if any (Policy of the same and provision made during the year )

Investments Investments

1 Confirmation from subsidary

Inventory

1 Inventory register for the FY 2023-24

2 Month wise Stock details received from Plant

3 Stock reco with the financials

4 Stock Ageing/ movement of inventory (In quantity and amount)

43

5 Once we receive the item no 1, we will share the samples for NRV and FIFO testing.

loans and advance loans and advance

1 Loan agreement approval Mails Confirmation

2 Details of capital advances

3 AIS / TIS, form 26AS downloaded from IT Portal, details of advance tax paid (Challan copies)

4 Copy of Refund application for GST paid on export of services

5 GST reconciliation statement

Other Non Current Assets Other Non Current Assets

1 Listing of security deposits along with the agreements (if any)

Cash and Bank Balance Cash and Bank Balance

1 Direct Bank Confirmation of HSBC and YES Bank (Please check the annexures for reference)

2 Cash balance confirmation

3 Bank Statements For the whole year of all banks

Revenue

1 PO details,Export Bills,Shipping bills,Gate inward outward,Transportation details of the samples we share with you

1 Sales register for FY 2023-24

2 Sales register for first quarter of FY 2023-24

Other incomes Other incomes

1 Details of export incentives, related documents

2 Policy on scrap sales

Employee benefit exp Employee benefit exp

1 Salary register for the FY 2023-24

2 Details of new joinees, existing employees, resignees during the year along with their agreements

3 PF, esic returns and challans

Finance cost Finance cost

1 Working of Interest on ECB loan

2 Working of interest on domestic loans from related parties

Property , plant and equipments Property , plant and equipments

1 Fixed assets register for the FY 2023-24

2 Physical verification report

Other exp Other exp

1 Once we receive the GL, we will share the samples for the purpose of test of details

2 Schedule of legal and professional along with nature and agreements

3 Rent agreement (if renewed)

4 Working of foreign exchange gain/loss

44

Purchase Purchase

1 PO details,Export Bills,Shipping bills,Gate inward outward,Transportation details

2 Purchase register for the FY 2023-24

Notes to Accounts Notes to Accounts

1 Statement of earning in foreign currency

2 Statement of expenditure in foreign currency

Formats to be used for Schedule 3 financials-

A company shall disclose Shareholding of

Promoters as below

Shares he Id by promoters at the end of the year Shares he Id by promoters at the end of the year Shares he Id by promoters at the end of the year Shares he Id by promoters at the end of the year Change during the year

S, No Promoter name No, of Shares of total shares

Total Total

FB. Trade payables due for payment The following

ageing schedule shall be given for Trade payables

due for payment- Trade Payables ageing schedule

(Amount in ?)

Particulars Outstanding for following periods from due date of payment Outstanding for following periods from due date of payment Outstanding for following periods from due date of payment Outstanding for following periods from due date of payment

Particulars Less than 1 year 1 -2 years 2-3years More than 3 years Total

(i) MSME (ii) Others (iii) Disputed dues -MSME (iv) Disputed dues - (v) Others

similar information shall be given where no due

date of payment is specified in that case

disclosure shall be from the date of the

transaction. Unbilled dues shall be disclosed

separately

45

(iv) For trade receivables outstanding, following

ageing schedule shall be given

Trade Receivables ageing schedule (Amount in ?)

Particulars Outstanding for following periods from due date of payment Outstanding for following periods from due date of payment Outstanding for following periods from due date of payment Outstanding for following periods from due date of payment Outstanding for following periods from due date of payment

Particulars Less than 6 months 6 months -1 year 1-2 years 2-3 years More than 3 years Total

(i) Undisputed Trade receivables -considered good (ii) Undisputed Trade Receivables - considered doubtful (iii) Disputed Trade Receivables considered good

Relevant line item in the Balance sheet Description of item of property Gross carrying value Title deeds held in the name of Whether title deed holder is a promoter, director or relative of promoter / director or employee of promoter/direct or Property held since which date Reason for not being held in the name of the company

PPE Land Building " " "also indicate if in

46

STATUTORY FILING DUE DATES-

Annexure 1 Compliance calendar

S. No.

Compliance area

Compliance description Frequency

Due Date

1 Corporate Income tax Advance tax payment (Federal) Quarterly 15th day of June, September, December and March of every tax year

1 Corporate Income tax Return of income (Federal) Yearly 31 October 2024 (30 November 2024 in case transfer pricing is applicable)

2 Withholding taxes Withholding tax payments (Federal) (Salary and Non-Salary) Monthly 7th of the subsequent month except for March which is due by 30 April 2024

2 Withholding taxes Withholding tax returns (Federal) (Salary and Non-Salary) Quarterly 31 July - first quarter 31 October - second quarter 31 January - third quarter 31 May - fourth quarter

2 Withholding taxes Withholding tax certificate (Federal) (Form-16A Non-Salary) Quarterly 15 August - first quarter 15 November - second quarter 15 February - third quarter 15 June - fourth quarter

3 Tax audit (applicable in case of turnover above INR 10 crore) Filing of prescribed information in Form No 3CD, accompanied by tax auditor's certificate in Form No 3CB Yearly 30 September 2024(31 October 2024 in case transfer pricing applicable)

4 Transfer pricing (applicable in case of foreign related party tr

Recommended