Group Example 1: JEs to Financial Statements - PowerPoint PPT Presentation

1 / 33

Title:

Group Example 1: JEs to Financial Statements

Description:

In a payroll, record salaries to professional employees, $7,000; payable next period. ... Cash 30,000 Salaries payable 7,000. Accounts rec 10,000 Owners' Equity ... – PowerPoint PPT presentation

Number of Views:22

Avg rating:3.0/5.0

Title: Group Example 1: JEs to Financial Statements

1

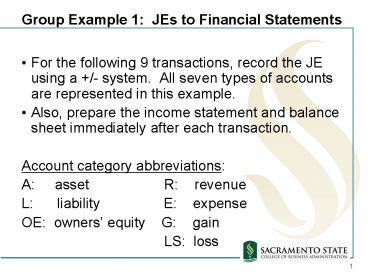

Group Example 1 JEs to Financial Statements

- For the following 9 transactions, record the JE

using a /- system. All seven types of accounts

are represented in this example. - Also, prepare the income statement and balance

sheet immediately after each transaction. - Account category abbreviations

- A asset R revenue

- L liability E expense

- OE owners equity G gain

- LS loss

2

Continued

- Issue common stock for 40,000.

- Purchase equipment for 10,000 on account.

- Pay the account payable from the equipment

purchase 30 days later. - Provide services to a client who is billed

10,000. - In a payroll, record salaries to professional

employees, 7,000 payable next period.

3

Continued

- Purchase investments in stock for 1,200.

- Sell investments in stock costing 400 for 700.

- A component of the equipment fails the cost to

replace it is 2,000. - Dividends of 300 are declared and paid at

year-end.

4

Continued

- 1. Issue common stock for 40,000.

- Cash 40,000 (A)

- Common stock 40,000 (OE)

- Net assets (A-L OE) have increased 40,000.

- Often this is among the first transactions for a

corporationshareholders must provide equity

capital before lenders provide debt capital.

5

Continued

- Balance Sheet

- Assets Liabilities

- Cash 40,000 Owners Equity

- Common

stock 40,000 - Tot assets 40,000 Total Liabs OE

40,000 - (We have skipped the posting step normally JEs

are first posted to the accounts in the ledger.

Then those balances are transferred to the

financial statements.)

6

Continued

- 2. Purchase equipment for 10,000 on account.

- Equipment 10,000 (A)

- Accounts payable 10,000 (L)

- No change in net assets (A-L).

7

Continued

- Balance Sheet

- Assets Liabilities

- Cash 40,000 Accounts pay

10,000 - Equipment 10,000 Owners' Equity

- Common

stock 40,000 - Total assets 50,000 Total Liabs OE 50,000

8

Continued

- 3. Pay the account payable from the equipment

purchase 30 days later. - Accounts payable -10,000 (L)

- Cash -10,000 (A)

- No change in net assets (A-L).

9

Continued

- Balance Sheet

- Assets Liabilities

- Cash 30,000

- Equipment 10,000 Owners' Equity

- Common

stock 40,000 - Total assets 40,000 Total Liabs OE 40,000

10

Continued

- 4. Provide services to a client who is billed

10,000. - Accounts receivable 10,000 (A)

- Service revenue 10,000 (R)

- This transaction increases net assets 10,000.

- It also is the first transaction affecting

earnings.

11

Continued

- Balance Sheet

- Assets Liabilities

- Cash 30,000

- Accounts rec 10,000 Owners' Equity

- Equipment 10,000 Common stock 40,000

-

Retained earns10,000 - Total assets 50,000 Total Liabs OE 50,000

12

Continued

- The balance shows the immediate effect on

retained earnings (OE). But in practice,

retained earnings is not updated until the

nominal accounts are closed in the closing JE. - Retained earnings is an OE account that houses

total income to date less total dividends to

date. It is the account which causes the balance

sheet to remain in balance when income is

recognized.

13

Continued

- Income Statement

- Service revenue 10,000

- Again note that we would not prepare an income

statement after only one transaction. - To this point, there are no recorded expenses.

14

Continued

- 5. In a payroll, record salaries to professional

employees, 7,000 payable next period. - Salaries expense 7,000 (E)

- Salaries payable 7,000 (L)

- This transaction decreases net assets 7,000.

15

Continued

- Balance Sheet

- Assets Liabilities

- Cash 30,000 Salaries payable

7,000 - Accounts rec 10,000 Owners' Equity

- Equipment 10,000 Common stock 40,000

- Retained

earns 3,000 - Total assets 50,000 Total Liabs OE 50,000

16

Continued

- Income Statement

- Service revenue 10,000

- Salaries expense (7,000)

17

Continued

- 6. Purchase investments in stock for 1,200

- Investments 1,200 (A)

- Cash -1,200 (A)

- No effect on net assets (A-L).

18

Continued

- Balance Sheet

- Assets Liabilities

- Cash 28,800 Salaries payable

7,000 - Accounts rec 10,000

- Investments 1,200 Owners' Equity

- Equipment 10,000 Common stock 40,000

- Retained

earns 3,000 - Total assets 50,000 Total Liabs OE

50,000 - No effect on income statement.

19

Continued

- 7. Sell investments in stock costing 400 for

700 - Cash 700 (A)

- Investments -400 (A)

- Gain on investments 300 (G)

- This transaction increased net assets 300.

- The sum of () amounts is not equal to the sum of

(-) amountsthis is a hint for why we need a

better recording system.

20

Continued

- Balance Sheet

- Assets Liabilities

- Cash 29,500 Salaries payable

7,000 - Accounts rec 10,000

- Investments 800 Owners' Equity

- Equipment 10,000 Common stock 40,000

-

Retained earns 3,300 - Total assets 50,300 Total Liabs OE

50,300

21

Continued

- Income Statement

- Service revenue 10,000

- Salaries expense (7,000)

- Gain on investments 300

- Although GAAP often requires reporting an item as

a gain or loss rather than a revenue or expense,

the rules are not complete with respect to this

classification issue.

22

Continued

- This leads to firms often acting on their

reporting preferences, which are the following - report a large negative item as a loss rather

than expense so that users will not consider the

item as being representative of future results. - report a large positive item as a revenue rather

than a gain, for just the opposite reason.

23

Continued

- 8. A component of the equipment fails the cost

to replace it is 2,000. - Loss on equipment 2,000 (LS)

- Cash -2,000 (A)

- This transaction reduces net assets 2,000.

- Losses are distinguished from expenses in that

the former have no benefit.

24

Continued

- Why isnt the equipment account increased, rather

than recording the loss? - Recall the definitions of asset, and loss.

25

Continued

- Balance Sheet

- Assets Liabilities

- Cash 27,500 Salaries payable

7,000 - Accounts rec 10,000

- Investments 800 Owners' Equity

- Equipment 10,000 Common stock 40,000

-

Retained earns 1,300 - Total assets 48,300 Total Liabs OE

48,300

26

Continued

- Income Statement (Final)

- Service revenue 10,000

- Salaries expense (7,000)

- Operating income 3,000

- Gain on investments 300

- Loss on equipment (2,000)

- Net income 1,300

- Many firms provide this subtotal but it is not

required and GAAP does not define operating

income.

27

Continued

- 9. (Last transaction) Dividends of 300 were

declared and paid at year-end. - Retained earnings -300 (OE)

- Cash -300 (A)

- Dividends are a distribution of earnings, not an

expense. - This transaction reduces net assets 300.

28

Continued

- Balance Sheet (Final)

- Assets Liabilities

- Cash 27,200 Salaries payable

7,000 - Accounts rec 10,000

- Investments 800 Owners' Equity

- Equipment 10,000 Common stock 40,000

-

Retained earns 1,000 - Total assets 48,000 Total Liabs OE

48,000 - No effect on income statement.

29

Group Example 2

- On 4/1/x1, a publishing firm received 60,000

from various customers for subscriptions to

magazines covering the year beginning 4/1/x1. - TJE 4/1/x1 Cash 60,000

- Unearned revenue

60,000 - AJE 12/31/x1 Unearned revenue 45,000

- Subscriptions revenue

45,000 - Unearned revenue is a liability end balance

15,000 - 45,000 60,000(9/12)

30

Group Example 3

- On 9/1/x1 a firm prepaid rent for the year

beginning on that date by paying 24,000. - TJE 9/1/x1 Prepaid rent 24,000

- Cash

24,000 - AJE 12/31/x1 Rent expense 8,000

- Prepaid rent

8,000 - 8,000 24,000(4/12)

- Ending prepaid rent (asset) balance is 16,000

31

Group Example 4

- A firm incurs 4 million of R D cost during the

current year. If the project is successful, it

is expected to provide benefits for 10 years. - Provide the JEs for the two alternative

accounting approaches discussed (expense

capitalize and amortize).

32

Group Example 4

- Current yearexpense immediately

- R D expense 4 million

- Cash, materials etc 4 million

- Current yearcapitalize and amortize

- Deferred R D (asset) 4 million

- Cash, materials etc 4 million

33

Continued

- Each year for 10 years

- R D expense .4 million

- Deferred R D .4 million

Recommended

CrystalGraphics Presentations