The Duration Model PowerPoint PPT Presentation

1 / 21

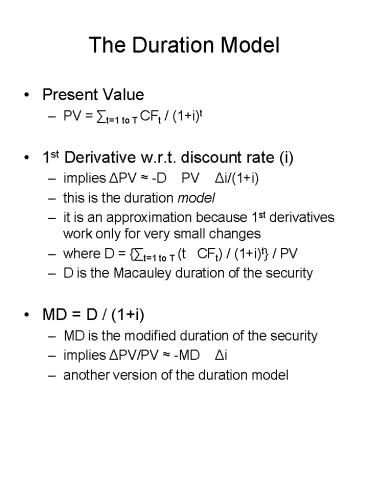

Title: The Duration Model

1

The Duration Model

- Present Value

- PV ?t1 to T CFt / (1i)t

- 1st Derivative w.r.t. discount rate (i)

- implies ?PV -D PV ?i/(1i)

- this is the duration model

- it is an approximation because 1st derivatives

work only for very small changes - where D ?t1 to T (t CFt) / (1i)t / PV

- D is the Macauley duration of the security

- MD D / (1i)

- MD is the modified duration of the security

- implies ?PV/PV -MD ?i

- another version of the duration model

2

Meaning(s) of Duration

- Weighted-Average Maturity

- Weights are the relative contribution to the

total value of the security or PVcashflow/PVsecuri

ty - Better way of measuring (and matching) maturity

than date of receipt of last cash flow - Measure of Interest Rate Risk

- MD is an elasticity w.r.t. changes in the

discount rate. - ?PV/PV -MD ?i

3

Calculating Duration

4

Duration Model vs. Reality

- Duration is a linear approximation of a

non-linear world. - The approximation gets worse as the interest rate

change grows larger - The difference between the actual change in value

and the duration prediction is due to convexity

5

Duration of a Portfolio

- The duration of a portfolio is the

weighted-average duration of the individual

securities. - MDportfolio ?j1 to J wj MDj

- The weights equal the contribution of the

security to the value of the portfolio - wj PVj/PVportfolio

- As required, the weights sum to one

- ?j1 to J wj 1

- Example Portfolio with 3 securities

- 10K of Bond A (MD 6.3 years)

- 55K of Bond B (MD 2.7 years)

- 35K of Bond C (MD 0.4 years)

- weight of Bond A 10/(105535) 0.10

- MDportfolio (0.10 6.3) (0.55 2.7) (0.35

0.4) 2.26 years

6

Convexity

- The duration model (?PV/PV -MD ?i) is only an

approximation. - As ?i gets larger, the error grows.

- Can we improve on this? Yes.

- ?PV/PV -MD ?i ½C ?i²

- C is the convexity of the security

- Calculated in a manner similar to MD (more

complex formula) - based on 2nd derivative w.r.t. discount rate

7

Convexity

- Positive Convexity

- for the typical bond, C gt 0

- gains are bigger for decrease in rates than loss

for same increase in rates - when Cgt0 the duration model is conservative

- actual gains and losses are less than predicted

by duration model - Negative Convexity

- for some securities, C lt 0

- we call this negative convexity

- BAD gains are smaller for decrease in rates than

loss for same increase in rates - when Clt0 the duration model underestimates losses

and overestimates gains - only happens when CFs change with changes in

interest rates - mortgage portfolios act this way

8

Convexity

- Why isnt convexity used in practice?

- Impractical

- Cannot calculate the convexity of a portfolio

from the convexity of its individual securities.

9

Duration of Equity

- According to the balance sheet identity

- Assets Liabilities Equity

- Equity Assets Liabilities.

- Using this identity to reflect PV rather than

Book Value - PVequity PVassets PVliabilities

- a.k.a. the Economic Value of Equity or EVE

- Not the same as market value

- Equity is a portfolio containing positive assets

and negative liabilities. - MDequity (PVassets/PVequity)MDassets

(PVliabilities/PVequity)MDliabilities

10

Duration of Equity Examples

- Example 1

- PV Assets of 500 million (MD 3.5 years)

- PV Liabilities of 450 million (MD 2.5 years)

- EVE 50 million

- MDequity (500/50)3.5 (450/50)2.5 12.50

years. - What happened?

11

Duration of Equity Examples

- Example 2

- PV Assets of 500 million (MD 2.5 years)

- PV Liabilities of 450 million (MD 3.5 years)

- EVE 50 million

- MDequity (500/50)2.5 (450/50)3.5 -6.50

years. - Negative Duration?

12

Advantages of Duration Model

- Single Number easy to interpret

- bigger riskier

- positive implies hurt by rising interest rates

- Easy to Explain

- Senior management

- Easy to Calculate

- Spreadsheet technology

- Unambiguous

- Set targets or limits

- Rough but consistent

- For small interest rate changes

13

Disadvantages of Duration Model

- Assumes Parallel Interest Rate Shocks

- All rates move by same amount

- Instantaneously and permanently

- What is short and long rates move differently?

- Linear Model

- Non-linear world cant translate convexity to

portfolio level - Embedded Options

- Model only considers promised cash flows (can be

adjusted to expected cash flows) - Does not capture changing cash flows

- Off-Balance Sheet Activities

- Fee income sources may be sensitive to changing

market rates

14

Improvements on Duration Model

- Quasi-Assets

- solution for ignoring OBS activities

- estimate future cash flows and appropriate

discount rate and calculate value/duration - treat fee-based activity as an asset with

predictable, periodic cash flows.

15

Improvements on Duration Model

- Effective duration

- used when cash flows are known to change when

interest rates change (e.g. embedded options are

present) - manipulate ?PV/PV -MD ?i

- to get EMD -(?PV/PV) / ?i

- EMD is the effective (implied) modified duration

- Employ complex ( accurate) valuation model

- measure value under current interest rates

- measure value for fixed increase in interest

rates use that ?PV to measure EMD() - measure value for (same) fixed decrease in

interest rates use that ?PV to get EMD(-) - EMD average of EMD() and EMD(-)

- not precise but better than strict duration model

which assumes cash flows dont change

16

Improvements on Duration Model

- Effective duration example

- portfolio of asset-backed securities

- value under current conditions is 5.00 million

- value if interest rates increase by 0.25 is

estimated at 4.40 million - EMD() -(-0.60/5.00)/0.0025 48.0

- value if interest rates decrease by 0.25 is

estimated at 5.35 million - EMD(-) -(0.35/5.00)/-0.0025 28.0

- EMD (48.0 28.0) / 2 38.0

17

Improvements on Duration Model

- Key Rate Duration

- solution to problem of assuming parallel interest

rate shocks (all rates change permanently by same

amount at same time) - measure the sensitivity of each asset to

- short-term riskless yield

- a set of differences between the short-term

riskless yield and riskless yields associated

with different maturities - An Example measure independent sensitivities to

- 3-month CMT

- 1-year CMT - 3-month CMT

- 5-year CMT - 1-year CMT

- 20-year CMT - 5-year CMT

- these should be independent of one-another

- CMT constant maturity Treasury

18

Scenario Analysis

- Requires accurate valuation model

- (1) Identify key inputs to valuation model

economic factors - various interest rates

- volatility of rates

- default expectations/credit spreads

- (2) Select a set of predetermined alternative

future conditions - example of one scenario rates rise, interest

volatility increases, rising default/credit

spreads - pick other representative sets of input values

- focus on interest rates

- parallel shocks

- tilts

- twists

19

Scenario Analysis

- (3) Measure the value of the portfolio or

institution for each scenario using the

valuation model - (4) Look for unacceptable losses

- identify cause(s)

- fix problems

- Advantage compared to duration

- allows more complex valuation

- considers additional sources/causes of risk

- Disadvantages compared to duration

- less clear

- cant tell if an important scenario is missing

20

Simulation Models/Analysis

- Requires accurate valuation model

- (1) Identify key inputs to valuation model

- various interest rates

- volatility of rates

- default expectations/credit spreads

- (2) Identify the probability distribution of each

key input, including parameters - example joint normal distribution assumption

requires estimates of mean, standard deviation,

and correlations for each variable - other distributions can be more complex with more

parameters - (3) Randomly select a set of values for the key

inputs to the valuation model - based on distributional assumptions in (2)

21

Simulation Models/Analysis

- (4) Using the key input values

- for each security (face value, coupon rate,

maturity, contractual features known), determine

a value - (5) Repeat (3) and (4) a lot!

- 1,000 times

- (6) Study the results of this simulation

- dont worry about gains or small losses

- big losses? ask why? how many? too many?

Recommended