Currency Options PowerPoint PPT Presentation

1 / 37

Title: Currency Options

1

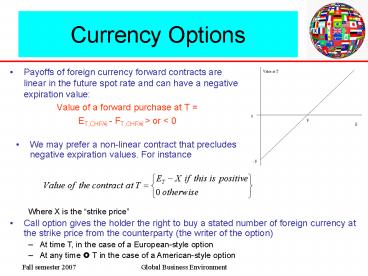

Currency Options

- Payoffs of foreign currency forward contracts are

linear in the future spot rate and can have a

negative expiration value - Value of a forward purchase at T

- ET,CHF/ - FT,CHF/ gt or lt 0

- We may prefer a non-linear contract that

precludes negative expiration values. For instance

- Where X is the strike price

- Call option gives the holder the right to buy a

stated number of foreign currency at the strike

price from the counterparty (the writer of the

option) - At time T, in the case of a European-style option

- At any time ? T in the case of a American-style

option

2

Example

- You buy a call on one at CHF/ 1.6 expiring at

T October 30, 2007. Hence, X 1.6 - If, on Oct 30 ECHF/ 1.58, you will not

exercise the option - If, on Oct 30 ECHF/ 1.62, you will exercise

the option, buy 1 for 1.6CHF and then sell 1

for 1.62CHF, making a profit of 0.02CHF - A European call option will be exercised at T iff

ECHF/ - X gt 0

- The value of the call option at T is

- CT Max (ET,CHF/ - X, 0)

3

Put options, American options, etc

- Put option gives the holder the right to sell a

stated number of foreign currency at the strike

price from the counterparty (the writer of the

option) - The value of a put option at T is

- PT Max (X - ECHF/, 0)

- Early exercise at t lt T of an American call

option is rational if - (Et,CHF/ - X) gt 0, a positive value dead

- The option market value is no higher than the

value dead - Example You buy an american call on one at

XCHF/ 1.6 expiring at the end of October. If

today E 1.58, you wait. If E 1.62 but market

price Ct0.04, you are better off selling than

exercising - A call can be used to insure a foreign currency

debt against a high (depreciated) exchange rate - You pay an insurance premium (up front) to buy

the option

4

Money Supply

- Money Supply (Ms)

- Ms Currency Checking Deposits

- This is the monetary aggregate called M1

- M1 in Switzerland in July 2007 262348 mil CHF.

This is roughly 23 of GDP - An economys money supply is controlled by its

central bank - How does the central bank conduct monetary

policy? - A look at the SNB

- Hence, most central banks set directly the

reference nominal interest rate (three-month

Libor for the SNB, the federal fund rate for the

FED, etc) - So, how is money supply controlled?

5

Aggregate Money Demand

- The aggregate demand for money can be expressed

as - Md P x L(R,Y)

- where

- P is the price level

- Y is real national income

- L(R,Y) is the aggregate real money demand

- We write it as

- Md/P L(R,Y)

- -

6

Equilibrium in the money market

Interest rate, R

If the CB raises R

If the CB leaves R unchanged

Real money holdings

7

Price stickiness

- In the short run, the price level P is given. It

does not adjust instantaneously - Why?

- Some prices adjust instantaneously agricultural

goods traded in markets, commodities (oil, raw

materials, etc.) - Other prices do not adjust instantaneously wages

are negotiated periodically, prices on catalogues

(IKEA) - Wages are a large fraction of the cost of

producing goods and services

8

Equilibrium exchange rate

ECHF/

Return on CHF deposits

Expected return on deposits

0

Rates of return (in CHF terms)

CHF real money holdings

9

Domestic monetary expansion, M2 gt M1

ECHF/

The CHF/ exchange rate depreciates

Return on CHF deposits

1'

Expected return on deposits

E1

0

U.S. real money holdings

10

Foreign monetary expansion

The CHF/ exchange rate appreciates

1'

Increase in European money supply

2'

E2

0

1

11

The /Yen Exchange Rate

12

The / Exchange Rate

13

The CHF/ exchange rate

14

The Exchange Rate in the Long Run

- Long-run analysis

- The price level is perfectly flexible

- Prices and wages have enough time to adjust to

their market-clearing levels - Output is at its full employment level Y Yf

- Price level in the long run

- Long-run neutrality of money An increase in a

countrys money supply causes a proportional

increase in its price level

15

The Law of One Price

- Law of one price (LOP)

- Identical goods sold in different countries must

sell for the same price when their prices are

expressed in terms of the same currency. - This law applies only in competitive markets free

of transport costs and official barriers to trade - PiCHF (ECHF/) x (Pi)

- PiCHF is the CHF price of good i when sold in

Switzerland - Pi is the corresponding euro price in Europe

16

Purchasing Power Parity

- Theory of Purchasing Power Parity (PPP)

- The exchange rate between two counties

currencies equals the ratio of the countries

price levels - ECHF/ PCHF/P

- PCHF is the CHF price of a reference commodity

basket sold in Switzerland - P is the euro price of the same basket in Europe

17

Purchasing Power Parity

- By rearranging, one can obtain

- PCHF (ECHF/) x (P)

- PPP asserts that all countries price levels are

equal when measured in terms of the same currency - The law of one price applies to individual

commodities, while PPP applies to the general

price level - If the law of one price holds true for every

commodity, PPP must hold automatically for the

same reference baskets across countries

18

Relative PPP

- Take percent deviations of PPP

- (ECHF/,t - ECHF/, t 1)/ECHF/, t 1 ?CHF, t

- ?, t - where ?t inflation rate

- It states that the percentage change in the

exchange rate between two currencies over any

period equals the inflation differential - If ?CHF, t gt ?,t the CHF/ exchange rate should

depreciate in the long run

19

Long-Run Effects of a Permanent Change in Money

Supply

- A permanent increase in a countrys money supply

causes a proportional long-run depreciation of

its currency against foreign currencies - In the long run

- A permanent increase in Ms raises PCHF which

raises ECHF/ in the long run

20

Short-Run Effects

Long-Run Effects of a Permanent Change in Money

Supply

- Take P and Y as given

- Suppose MCHF rises. Then

- RCHF falls while R unchanged

- By the IPC

- RCHF R (EeCHF/ - ECHF/)/ECHF/

- it follows that (EeCHF/ - ECHF/)/ECHF/ falls

- EeCHF/ depreciates proportionally to MCHF

- This implies that the spot exchange rate ECHF/

depreciates more than the expected future

exchange rate EeCHF/ - This is the Exchange-Rate Overshooting the

short-run response is greater than the long-run

response

21

Exchange Rate Volatility

22

Subsequent Adjustment Process

- In the long run, PCHF rises, MCHF/PCHF goes back

to its initial level - RCHF increases over time

- EeCHF/ is unchanged

- By the IPC

- RCHF R (EeCHF/ - ECHF/)/ECHF/

- it follows that (EeCHF/ - ECHF/)/ECHF/

increases, which implies that ECHF/ falls

(appreciates) - In the long run, the exchange rate has

depreciated proportionally to the increase in the

money supply

23

Short- and Long-Run

CHF return

E2

E4

E1

1'

M2CHF P1CHF

24

A Long-Run Exchange Rate Model Based on PPP

- IPC

- RCHF R (EeCHF/ - EeCHF/ ) / EeCHF/

- Relative PPP

- (EeCHF/ - ECHF/)/ECHF/ ?eCHF - ?e

- This implies the Fisher relationship

- RCHF - R (EeCHF/ - ECHF/)/ECHF/ ?eCHF

- ?e - The international interest rate differential is

the difference between expected national

inflation rates

25

Empirical Evidence on the Fisher Relationship

Switzerland

26

Empirical Evidence on the Fisher Relationship

The United States

27

Empirical Evidence on the Fisher Relationship

Switzerland and the United States

28

Empirical Evidence on the Fisher Relationship

29

Empirical Evidence on PPP and the Law of One

Price

- Big Mac Currencies, published by The Economist

- Started in 1986 it is a survey of Big Mac

hamburger prices at McDonalds restaurants around

the world - It is a homogeneous good. Hence the Law of One

Price would apply - Evidence The Economist

30

(No Transcript)

31

Big Mac

- Column 1 Big Mac price in local currency Px

- Column 2 Px multiplied by E/x, the U.S.

dollar/local currency price exchange rate. This

is the dollar price of the Big Mac in country X - Column 3 Px/ PUS. This is the implied PPP of

the U.S. dollar, EPPP/X - Column 3 (EPPP/X - E/X)100 / E/X

- This is the under(-)/over() valuation of

currency X against the U.S. dollar - The CHF is 53 overvalued relative to the US

Dollar

32

Big Mac (cont.)

- China most undervalued, Iceland the most

overvalued - If you can keep the Big Mac fresh, buy it in

China for the equivalent of 1.45 and sell it in

Iceland for 7.6! - Trade barriers, transport costs and differences

in taxes - Use of non-traded goods and services, like labor

and rent contribute about 60 of the price of the

Big Mac - Most expensive Big Mac Iceland, Norway,

Switzerland, Denmark - Least expensive Big Mac Sri Lanka, Indonesia,

Hong Kong

33

Explaining the Problems with PPP

- The failure of the empirical evidence to support

the PPP and the law of one price is related to - Trade barriers and transport costs

- Nontradable goods

- Departures from free competition

- International differences in price level

measurement

34

Trade Barriers and Transport Costs

- Transport costs and governmental trade

restrictions make trade expensive - Equivalent to 170 tariff in advanced economies

35

Non-tradable goods

- The domestic prices of non-tradable goods can be

very different when expressed in the same

currency - Example housing price in Lausanne and in New

Delhi - No arbitrage

- Non-tradable goods account for about 50 of GNP

and hence 50 of the CPI - Non-tradable goods are more expensive in richer

countries

36

Balassa-Samuelson Model

- In poorer countries, productivity in tradable

goods and therefore wages are lower - Prices of non-tradable goods are lower

- PN gt E PN

- Where PN is the foreign price of non-tradable

goods - Because non-tradable goods account for almost 50

of the CPI (consumer price index) - P gt E P

37

Explaining the Problems with PPP

Recommended