Market Overview - PowerPoint PPT Presentation

1 / 12

Title:

Market Overview

Description:

Case Study: Commonwealth of Massachusetts Series 2003 ... Case Studies (continued) Case Study: Colorado Department of Transportation Series 2001A (continued) ... – PowerPoint PPT presentation

Number of Views:33

Avg rating:3.0/5.0

Title: Market Overview

1

Market Overview

Current Market Conditions and Trends

4

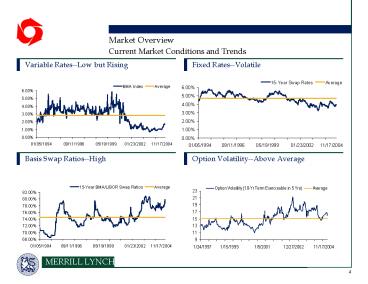

2

Market Overview

Rates

The current yield curve is steeper than average.

Swaps may offer a lower cost of funds.

____________________ Rates as of 11/17/2004.

5

3

Market Overview

Interest Rate Forecast

Research Commentary

Forecast Rates

- Current Fed Funds 2.00

- Current 10-year Treasury Note 4.18

- The Federal Reserve raised the Fed Funds target

rate 25 basis points to 2.00 at the November

10th meeting. - The Fed believes that accommodative policy

coupled with robust growth in productivity is

providing ongoing support to economic activity. - The Committee perceives the upside and downside

risks to sustainable growth and price stability

in the near future to be roughly equal. - The next Fed meeting is on December 14th, 2004.

- Merrill Lynch economists predict long-term rates

falling through the end of 2004, then continuing

a steady descent until Q2 2005. - October non-farm payrolls showed a 337,000 jump,

twice the 169,000-job growth that Wall Street

economists had forecast, - However, the unemployment rate edged up to 5.5

from 5.4 in September.

6

4

GARVEEs (Grant Anticipation Revenue Vehicles)

Geographic Diversity

States that have issued GARVEE Bonds States that

have authorized the issuance of GARVEE Bonds

Montana

Michigan

Massachusetts

Rhode Island

Nevada

New Jersey

Ohio

Colorado

Maryland

California

Virginia

Arizona

Oklahoma

Arkansas

New Mexico

Georgia

Louisiana

Alaska

Alabama

Florida

Mississippi

Virgin Islands

11

5

GARVEEs (Grant Anticipation Revenue

Vehicles) Highway GARVEE Transactions

22

6

GARVEEs (Grant Anticipation Revenue Vehicles)

- Direct vs. Indirect Structure

- Direct GARVEEs

- Must be approved by FHWA

- Fund specific FEDERAL aid project or projects

- Proceeds only used on preapproved projects

- Principal/interest payment approved and paid on

schedule by FHWA - Indirect GARVEEs.

- Can be issued without any prior FHWA approval

- Funds can be used on STATE and FEDERAL projects

- Determination on what to use funds for can be

made after reimbursement

7

GARVEEs (Grant Anticipation Revenue

Vehicles)Direct vs. Indirect Structure

- Used to finance a specific project or projects

- State submits the debt service schedule for

approval (this is called programming) - All proceeds need to be spent on the specific

project or projects that were approved leaving no

spending discretion or flexibility - State submits for reimbursement before each

principal/interest payment and State receives a

reimbursement (three days) before the payment is

actually made

8

GARVEEs (Grant Anticipation Revenue

Vehicles)Direct vs. Indirect Structure

- No restrictions on the usage of bond proceeds -

treated as any other State funds - can spend on

either Federal or State projects - Issued without FHWA approval

- Backed by future federal reimbursements of future

federally eligible expenditures - State continues its federal aid program, seeking

annual reimbursements for eligible expenses - Reimbursements used to amortize the GARVEE bonds

9

GARVEEs (Grant Anticipation Revenue

Vehicles)Direct vs. Indirect Structure

10

GARVEEs (Grant Anticipation Revenue Vehicles)

Case Study

Merrill Lynch senior managed the Commonwealth of

Massachusetts 408 million Federal Highway Grant

Anticipation Note Refunding Program transaction

in June 2003.

- Crossover Structure Merrill Lynch developed the

Refunding Notes innovative crossover feature,

believed to be the first crossover refunding in

the GARVEE marketplace, utilizing U.S. Agency

securities and an innovative escrow structure

designed to defease the prior bonds and pay

interest on the Refunding Notes through the call

date. - Indirect GARVEE Structure The Massachusetts

GANs program was not dependent on reimbursements

from a specific project, but rather allowed for

the use of all federal highway monies received,

thereby decreased risks associated with specific

project reimbursements. - Double-Barreled Pledge Additional bondholder

protection is provided through a double-barreled

security structure that pledges 0.10 of the

Commonwealths gas tax in the event of severe,

unprecedented declines in federal highway

funding. - Bond Document Constraints The governing bond

documents contain a number of constraints on GANs

issuance, including, - A limit on the issuance of additional notes

- New money proceeds capped at 1.5 billion (all of

which have been issued) - 216 million of annual debt service and 108

million of semi-annual debt service - Debt service funded from federal highway

reimbursements one year in advance - Advance construction balance covenant

- Capital Commitment During Volatile Market

Merrill Lynch successfully priced the Refunding

Notes during a volatile market environment

characterized by heavy supply and growing

indecision regarding the Feds impending

announcement on June 25th

13

11

GARVEEs (Grant Anticipation Revenue Vehicles)

Case Studies (continued)

- TRANs are CDOTs version of GARVEE bonds

- Secured by a pledge of the Colorado

Transportation Commissions annual allocation of

funds to the TRANs - Repayment sources for the TRANs include

- CDOTs FHWA monies

- Sales and use tax funds

- Highway user tax funds

- Other miscellaneous revenues

- Very strict requirements approved by the voters

to authorize the TRANs

14

12

GARVEEs (Grant Anticipation Revenue Vehicles)

Case Studies (continued)

- The structuring work included

- Crafting the additional bonds test around the

voter approved requirement - Working with FHWA to develop a master project

reimbursement agreement - Mitigating risks associated with CDOTs Southeast

Corridor, a jointly financed project with Denver

RTD (the area transit district), and FTA - The initial transaction garnered ratings of

Aa3/AA/AA by Moodys, Standard Poors, and

Fitch, respectively. - Recent Credit Implications

- CDOTs revenue streams have been impacted by both

the economic downturn as well as legislative and

initiative-driven changes - Despite this uncertainty and CDOTs reduced

revenue stream, CDOT has been able to maintain

its ratings - Merrill Lynch was able to secure bond insurance

at a premium 1.6 basis points lower than the

initial Series 2000 TRANs - This occurred despite a new voter referendum

requiring an additional transfer of monies away

from CDOT

15

Recommended

CrystalGraphics Presentations