Business Case in Focus African sugar industry - PowerPoint PPT Presentation

1 / 3

Title:

Business Case in Focus African sugar industry

Description:

Business Case in Focus African sugar industry a rising star Introduction Sugar is the only commodity that is produced from two very different crops sugarbeet ... – PowerPoint PPT presentation

Number of Views:100

Avg rating:3.0/5.0

Title: Business Case in Focus African sugar industry

1

Business Case in FocusAfrican sugar industry a

rising star

- Introduction

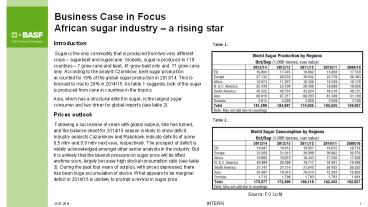

- Sugar is the only commodity that is produced

from two very different crops sugarbeet and

sugarcane. Globally, sugar is produced in 119

countries 7 grow cane and beet, 41 grow beet

only and 71 grow cane only. According to the

analyst Czarnikow, beet sugar production

accounted for 19 of the global sugar production

in 2013/14. This is forecast to rise to 20 in

2014/15. As table 1 suggests, bulk of the sugar

is produced from cane in countries in the

tropics. - Asia, which has a structural deficit in sugar, is

the largest sugar consumer and key driver for

global imports (see table 2). - Prices outlook

- Following a succession of years with global

surplus, tide has turned, and the balance sheet

for 2014/15 season is likely to show deficit.

Industry analysts Cazarnikow and Rabobank

indicate deficits of some 0.5 mtrv and 0.9 mtrv

next year, respectively. The prospect of deficit

is widely acknowledged amongst other senior

analysts in the industry. But it is unlikely that

the bearish pressure on sugar price will be

lifted anytime soon, largely because high

stocks/consumption ratio (see table 3). During

the past four years of surplus, with prices

depressed, there has been huge accumulation of

stocks. What appears to be marginal deficit in

2014/15 is unlikely to prompt a revival in sugar

price.

Table 1.

Table 2.

Source FO Licht

2

Table 3.

The probable drivers on price development in the

foreseeable future include the following Bearis

h Replenished stocks dampening minor supply

shocks Sugar production from new build projects

coming online adding to global output Speculators

maintaining a large net short position in New

York sugar futures. In the week ending August 12,

speculators increased their net short position by

15,042 lots, bringing it to 56,432. In a review

of impact of speculative trading activities by

Commonwealth Bank of Australia in October 2013,

the bank found correlation between speculative

trader positions and prices to be an

exceptionally strong 92. EU sugar producers

expanding production to wrest a larger market

share come the abolition of quotas in

2017 Currency markets have a significant impact

on global prices.

According to a study by the Commonwealth Bank of

Australia (CBA), depreciation of the Brazilian

Real (BRL) again the US dollar softens the impact

of declining US denominated sugar values.

Since 1st January 2011, the BRL has depreciated

38 against the US, while the Indian Rupee has

depreciated 40. The correlation between US

sugar prices and the US/BRL over the period is

negative 78, according to CBA. With elections

looming in Brazil, economy in recession,

uncertainty over the weak BRL remains.

Bullish Weather is the biggest joker in pack.

Drought and floods were responsible for reducing

sugar output by some 10 million tonnes in 2009

which subsequently triggered the 30 year high in

sugar prices. With precipitation 40 below in

Brazils main cane growing region Centre South,

some analysts have revised down sugar output as

cane quality has been adversely affected by

drought. 2014/15 campaign may end a month

earlier. In India, rainfall deficit since the

start of monsoon season is 18 (as of

June). Brazilian mills diverting more cane to

produce ethanol in preference over

sugar Consumption demand in Asia remaining

strong, and rising in emerging economies

Barring no game-changing incidents in the

foreseeable future, it appears that next few

years may see stabilization of sugar prices,

probably hovering in the 18-24 cents/lb range.

3

- Competitiveness of the African Sugar Industry

- In a recently published study in International

Sugar Journal, looking at investment in the

global sugar industry reported in the press over

the past year, 14 sugar producing countries in

Africa have received the lions share greater

than investment in all the sugar producing

regions combined. These are Sudan, Ghana, Kenya,

Nigeria, Tanzania, Ethiopia, Angola, South

Africa, Swaziland, Mozambique, Malawi, Zambia,

Algeria and Egypt. There are multiple projects in

several countries, for example, in Angola, two

factories with capacities of over 250,000 tonnes

sugar are planned, in Ethiopia, seven new

factories are scheduled to come online in

2015.This is a superb vote of confidence by

investors convinced of the potential of Africas

sugar market and the competitiveness of the

individual countries sugar industries. - As table 1 suggests, Africa currently plays a

cameo role in the global sugar sector. But

despite this, it boasts some of the lowest cost

sugar producers in the world. In a study by LMC

International and Overseas Development Institute

couple of years ago, the following countries had

sugar production costs ltUS 400 Swaziland,

Mozambique, Ethiopia, Malawi, Sudan, Tanzania,

Zambia and Zimbabwe. Add to this South Africa.

Most of the companies operating factories in the

low cost countries are owned by large private

groups, e.g. Illovo, Tongaat-Hulett, Kenana. - Factors informing the competitiveness of these

industries include - Suitable climate and fertile soils for growing

cane along with availability of water for

supplementary irrigation - Availability of relatively low cost labour to

support agricultural operations - A long, dry season facilitates a long campaign

lasting up to at least 180 days which supports

high throughput in sugar factories and spreads

overheads - Shift towards large-scale agro-industrial

enterprises - factories with capacities well over

100,000 tonnes and attaching these with

biorefineries to produce co-products such as

ethanol - Supportive government policy structure that

includes protection of local industries from any

dumping of sugar from global market and thereby

investing confidence in private sector investors

and allaying any fears of risk of their

investment. There have been exceptions, where

through alleged corruption, smuggled sugar has

damaged industries in Tanzania and Kenya - An established collaborative structure between

millers, growers and researchers to support high

productivity and production of quality cane. This

is largely true of mostly corporate farming

(e.g.Kenana in Sudan) and or plantation

agriculture (e.g. Illovo in southern Africa). The

challenge remains in those countries where cane

to factories is supplied from small scale

growers.

Recommended

CrystalGraphics Presentations