Section 83 Transfers of Property PowerPoint PPT Presentation

1 / 19

Title: Section 83 Transfers of Property

1

Section 83 Transfers of Property

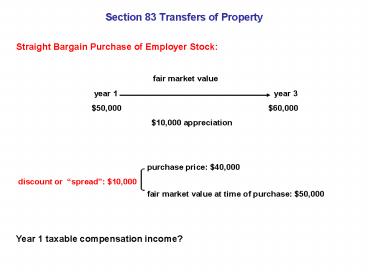

Straight Bargain Purchase of Employer Stock

fair market

value year 1

year 3

50,000

60,000

10,000 appreciation

purchase price 40,000

discount or spread 10,000

fair market value at time of purchase

50,000 Year 1 taxable compensation

income?

2

- 1012 Cost Basis in Stock

- purchase price (actual cost) 40,000

- tax cost

- (amount previously taxed) 10,000

(yr. 1 compensation income) - Total adjusted basis 50,000

- Year 3 Gain from Stock Sale for 60,000

- Amount Realized (AR) 60,000

- less Adjusted Basis (AB)

50,000 - 10,000

3

Amount, Character, and Timing

of Taxable Income

Taxable Income

Character year 1 purchase

10,000 ordinary

(salary) year 3 stock sale 10,000

capital gain (stock sale)

total taxable income

20,000

10,000

10,000 year 1 compensation

income appreciation in stock

value from bargain purchase

60,000 less 50,000 basis

4

Conditional Bargain Purchase of Employer Stock

fair market

value year 1

year 3

50,000

60,000

10,000 appreciation

purchase price 40,000

discount or spread 10,000

fair market value at time of purchase

50,000 CONDITION Stock not transferable

until year 3. Employee must sell stock back to

employer at 400 per share (40,000) is she

leaves employer prior to year

3 Substantial risk of forfeiture? Year

1 taxable compensation income? Year 3 taxable

income?

5

- 1012 Cost Basis in Stock

- purchase price (actual cost) 40,000

- tax cost

- (amount previously taxed) 20,000

(yr. 3 compensation income) - total adjusted basis 60,000

- Year 3 Gain from Stock Sale for 60,000

- Amount Realized (AR) 60,000

- less Adjusted Basis (AB)

60,000 - 0

6

Amount, Character, and Timing

of Taxable Income

Taxable Income

Character year 1 purchase

0 N/A year 3 risk lifted

20,000 ordinary

(salary) year 3 stock sale

0 capital gain (stock sale)

total taxable income

20,000 Result 10,000 bargain and

10,000 appreciation treated as compensation

60,000 less 60,000

basis

7

- With and Without Risk of

Forfeiture Compared - simple bargain purchase

with risk of forfeiture - year 1 purchase 10,000

(ordinary)

0 - year 3 - risk lifted N/A

20,000

(ordinary) - year 3 stock sale 10,000 (capital)

0 - total taxable income 20,000

20,000 - Impact of 83 risk of forfeiture rules

- advantage 3 year deferral

8

Tax Consequences to

Employer 83(h) simple

bargain purchase with risk of

forfeiture year 1 employee

purchase 10,000 deduction

no deduction year 3 - risk lifted

N/A

20,000 deduction year 3 stock sale

N/A

N/A total deductions

10,000 20,000

Impact of 83 risk of forfeiture

rules disadvantage delayed

deduction

9

83(b) Election

(assumes risk of forfeiture)

Taxable Income Character year 1

purchase 10,000

ordinary (salary) year 3 - risk lifted

-

- Taxpayer can elect to report 10,000

income in year 1 (difference between year 1

50,000 fmv and year 1 40,000 purchase price)

rather than wait until risk of forfeiture is

lifted in year 3 Why would taxpayer choose to

be taxed in year 1 rather than year 3??

10

1012 Cost Basis in Stock purchase price

(actual cost) 40,000 tax cost (amount

previously taxed) 10,000 (yr. 1

compensation) total adjusted basis 50,000

per 83(b) election Year 3 Gain from Stock

Sale for 60,000 Amount Realized (AR)

60,000 less Adjusted

Basis (AB) 50,000 10,000

11

- 83(b) Election

- (assumes risk

of forfeiture) - Taxable Income Character

- year 1 purchase 10,000

ordinary (salary) - year 3 - risk lifted 0

0 - year 3 stock sale

10,000 capital gain (stock

sale) - total taxable income 20,000

- Impact of 83(b) election

12

83(b) election - taxpayer must weigh

disadvantage of early taxable at

ordinary income rates

against advantage of

lower capital gains rates on sale Factors

1. What is the amount that would be taxed in

year 1? i.e. how much of a

discount did employee get? 2. How much

appreciation is expected? 3. What is the

likelihood that property will later be forfeited?

13

Section 83(b)

Stock Options Option with a

Readily Ascertainable Fair Market Value

total net

profit to employee 27 (35 less 8 cost) Stock

fmv 20

25

35 time

grant of option

exercise of option sale

of stock (exercise

price 8) (purchase for 8)

(sale for 35 fmv)

discount/spread 17

year 1

year 5

year 10 Assume exercise price 8 Assume

that option has a readily ascertainable fmv

12 Year 1 taxable compensation income?

14

- 1012 Cost Basis in Stock

- purchase price (actual cost) 8

- tax cost

- (amount previously taxed) 12

(yr. 1 compensation income fmv option) - total adjusted basis 20

- Year 10 Gain from Stock Sale for 35

- Amount Realized

(AR) 35 - less Adjusted Basis (AB)

20 -

15

15

Option with a Readily

Ascertainable Fair Market Value

Amount, Character, and Timing of Taxable Income

Taxable Income Character

year 1 (grant of option) 12 (fmv

option) ordinary

(salary) year 5 (exercise of option)

0

N/A year 10 (sale of stock) 15

capital

gain total taxable income

27 35 less 20 basis

16

Alternative Tax Treatment Tax at

Time of Exercise year 1

(grant of option) no tax

year 5 (exercise)

tax on spread

25 fmv less 8 purchase 17

17

1012 Cost Basis in Stock purchase price

(actual cost) 8 tax cost (amount

previously taxed) 17 (yr. 5

compensation income spread) total adjusted

basis 25 Year 10 Gain from Stock Sale

for 35 Amount

Realized (AR) 35 less

Adjusted Basis (AB) 25

10

18

- Alternative Tax Treatment Tax at

Time of Exercise - Taxable Income Character

- year 1 (grant of option)

0 N/A - year 5 (exercise of option) 17

(spread) ordinary (salary) - year 10 (sale of stock) 10

capital gain - total taxable income 27

19

Stock Option

Alternatives Compared 83 tax

grant of option tax option exercise ISO

- 422 year 1 (grant) 12

(ord) 0

0 year 5 (exercise) 0

17 (ord)

0 year 10 (stock sale) 15

(cap) 10

27 (cap) total taxable income

27 27 27 35 sales price

less 8 basis 27

Recommended