Most Developing Countries Are Deemed Marginally Creditworthy - PowerPoint PPT Presentation

1 / 16

Title:

Most Developing Countries Are Deemed Marginally Creditworthy

Description:

... boom of the 1990s was similar to earlier episodes in terms of its size; but ... All past episodes of surges in capital flows to emerging markets have ended in ... – PowerPoint PPT presentation

Number of Views:45

Avg rating:3.0/5.0

Title: Most Developing Countries Are Deemed Marginally Creditworthy

1

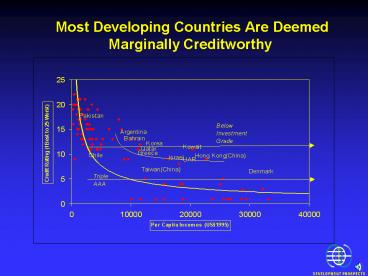

Most Developing Countries Are Deemed Marginally

Creditworthy

2

Aid flows rose in 1998 End of donor fatigue?

Billions of U.S. dollars

Percent

Percentage of GNP of DAC countries

3

Few countries reached the aid target

UN Target 0.7

Average country effort

4

Reduced aid flows but more efficient allocation

5

The Enhanced HIPC Framework

6

Official non-concessional flows declined in 1999

- Official non-concessional flows, including those

from the IMF, fell to negative levels in 1999

from unusually high levels in 1998 related to

rescue packages for crisis countries. - The role of such financing is changing in

response to concerns about moral hazard and the

need to bail-in the private sector.

7

Short-term lending to developing countries rose

rapidly in the 1990s

8

Short-term debt is pro-cyclical to economic growth

9

The pro-cyclical response is worse during adverse

shocks

10

Excessive short-term borrowing (relative to

reserves) has a strong association with crises

11

Safeguarding against crisis the near-term agenda

- Safeguard measures are needed in the near-term,

alongside longer-term measures, to reduce the

risks of crisis - An analysis of recent proposals suggest three

main conclusions - First, all such measures impose costs, but these

costs are likely to be less than those of a

full-fledged financial crisis, and especially for

the poor. - Second, none of these measures can substitute for

the need for better macroeconomic fundamentals. - Third, all such measures have their limitations

and may need to be combined and adapted to each

countrys circumstances

12

Safeguards come with costs

- Chilean-style taxes on short-term borrowing

require comprehensive coverage of all short-term

inflows - Prudential capital controls on the banking

sectors international exposure raise costs for

borrowers and may be difficult to implement - Restrictions on capital outflows are even more

difficult to implement - Increasing the amount of international reserves

imposes significant fiscal costs - Privately contracted contingent credit lines

require expensive collateral, may be offset by

reduced lending, and are likely to be available

only to the relatively creditworthy

13

One hundred (and thirty) years of capital flows

- The past 130 years have seen at least four surges

in private capital flows to emerging markets - 1870 to WW-I

- Post-WW-I recovery to the Great Depression

- 1973-1982

- the 1990s

14

Capital flows and crises were linked even before

the gold standard era

15

Four messages from history

- Capital surges to emerging markets occur when

communication is improving, growth and world

trade is expanding, financial innovation is

rapid, and the political climate is supportive. - The capital flows boom of the 1990s was similar

to earlier episodes in terms of its size but was

different in the variety of financial

instruments used and the variety of recipients - All past episodes of surges in capital flows to

emerging markets have ended in severe

international financial crises. - The next decade may well see another capital boom

to emerging markets, accompanied again by high

volatility of capital flows and potential crises.

Countries need to adopt better policies and

safety nets for the poor.

16

Technology will provide one impetus to capital

flows

Recommended

CrystalGraphics Presentations