Chapter Four - PowerPoint PPT Presentation

1 / 12

Title: Chapter Four

1

Chapter Four

Consolidation with Outside Ownership

Reporting Options (Income Statement)

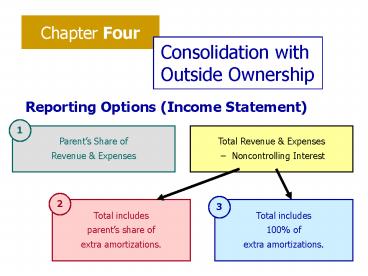

1

Parents Share of Revenue Expenses

Total Revenue Expenses Noncontrolling

Interest

2

3

Total includes parents share of extra

amortizations.

Total includes 100 of extra amortizations.

2

Reporting Options (Balance Sheet)

1

Parents Share of Assets Liabilities

Total Assets Liab. Noncontrolling Interest

2

3

Total includes parents share of extra assets.

Total includes 100 of extra assets.

3

Econ Unit

Proportion.

Parent Co.

Example, p.159

4

Prob 4-39

60

Parent Co

100

Econ Unit

(400,000 ? 0.60) - 470,000

5

Econ. Unit 380,000 250,000 378,000

252,000

Entry (S)

Parent Co. R/E 380,000 Common Stock 250,000 Invs

t in Houston 378,000 NC int Hstn 1/1/05 252,000

Both methods treat book values of subsidiary the

same.

6

Econ. Unit 124,000 14,000 51,667 21,

000 101,200 67,467

Entry (A)

Parent Co. Buildings 74,400 Bonds

Payable 8,400 Goodwill 31,000 Equipment 12,600

Invst in Houston 101,200 NC int Hstn 1/1/05

Buildings 93,000 3 x 6,200 Bonds

Payable 12,000 3 x 1,200 Goodwill 31,000 Equipm

ent (18,000) 3 x (1,800)

155,000 3 x 10,333 20,000 3 x

2,000 51,667 (30,000) 3 x (3,000)

60

100

7

Econ. Unit 36,400 36,400

Entry (I)

Parent Co. Equity in Hstn inc. 36,400 Invst in

Houston 36,400

The parents share of subsidiary income is the

same under both methods 60(70,000) - 5,600

36,400

Econ. Unit 24,000 24,000

Entry (D)

Parent Co. Invst in Houston 24,000 Dividends

Paid 24,000

8

Econ. Unit 7,333 2,000 3,000 10,333

2,000

Entry (E)

Parent Co. Deprec Expense 4,400 Interest

Expense 1,200 Equipment 1,800 Buildings 6,200 B

onds Payable 1,200

60

100

9

Econ. Unit 24,266 319,467 16,000 3

27,733

Noncontrolling Interest Entry

Parent Co. NCint in Hstn

inc. 28,000 NCint Hstn 1/1/05 252,000 Dividends

Paid 16,000 NCint Hstn 12/31 264,000

40 (70,000 - 9,333)

252,000 67,467

10

Prob 4-27

156,000 (80 x 140,000) 44,000

Part (e) Purchase took place on July 1, 2004

Entry (S) R/E (1/1/04) 95,000 Preacq

Income 4,000 Common Stock 40,000 Invst in

Goldm 112,000 NC int Gldm 1/1/04 27,000

11

Part (e) Purchase took place on July 1, 2004

(E) 800

(S) 4,000

(2,000)

(I) 3,200

½ year amortization

20 x 10,000

12

(No Transcript)

Recommended

CrystalGraphics Presentations