Topic Flow Chart PowerPoint PPT Presentation

1 / 25

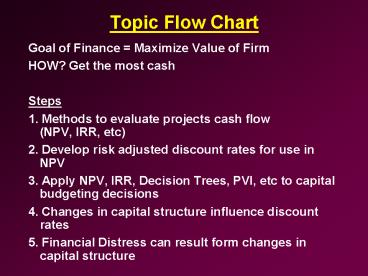

Title: Topic Flow Chart

1

Topic Flow Chart

- Goal of Finance Maximize Value of Firm

- HOW? Get the most cash

- Steps

- 1. Methods to evaluate projects cash flow

(NPV, IRR, etc) - 2. Develop risk adjusted discount rates for use

in NPV - 3. Apply NPV, IRR, Decision Trees, PVI, etc to

capital budgeting decisions - 4. Changes in capital structure influence

discount rates - 5. Financial Distress can result form changes in

capital structure

2

Efficient Capital Markets

- Switches gears

- Past lectures decided how to spend money (invest)

- Todays lecture deal with raising money

(financing decisions) - Fisher Separation Theorem

3

Efficient Capital Markets

- Market Efficiency Theory sez

- Capital markets reflect all relevant information.

You can not consistently earn excess profits.

4

Efficient Capital Markets

Cost of Capital Price of Money

R

D

S

Qty

5

Type of Market Efficiency

- Weak Form Efficiency

- Semistrong Form Efficiency

- Strong Form Efficiency

6

Efficient Market Theory

Announcement Date

7

Efficient Market Theory

Average Annual Return on 1493 Mutual Funds and

the Market Index

8

Efficient Market Theory

IPO Non-Excess Returns

Year After Offering

9

Efficient Market Theory

Strong-Form Efficiency Test Historical performance

10

Random Walk Theory

11

Random Walk Theory

12

Efficient Market Theory

- Fundamental Analysts

- Research the value of stocks using NPV and other

measurements of cash flow

13

Efficient Market Theory

- Technical Analysts

- Forecast stock prices based on the watching the

fluctuations in historical prices (thus wiggle

watchers)

14

Market Efficiency Theory

- Conflicts in Theory

- Stock market crash of 1987

- Daily fluctuations

- Culprits?

- Arbitrage

- Computers

- Institutions

15

Efficient Market Theory

1987 Stock Market Crash

16

Efficient Market Theory

1987 Stock Market Crash

17

Efficient Market Theory

2000 Dot.Com Boom

18

Lessons of Market Efficiency

- Markets have no memory

- Trust market prices

- Read the entrails

- There are no financial illusions

- The do it yourself alternative

- Seen one stock, seen them all

19

Corporate Financing

- Types of Financing

- 1 - Equity

- 2 - Debt

- 3 - Hybrids

20

Corporate Financing

- READ TEXT FOR TERMINOLOGY

21

Initial Offering

- Initial Public Offering (IPO) - First offering of

stock to the general public. - Underwriter - Firm that buys an issue of

securities from a company and resells it to the

public. - Spread - Difference between public offer price

and price paid by underwriter. - Prospectus - Formal summary that provides

information on an issue of securities. - Underpricing - Issuing securities at an offering

price set below the true value of the security.

22

General Cash Offers

- Seasoned Offering - Sale of securities by a firm

that is already publicly traded. - General Cash Offer - Sale of securities open to

all investors by an already public company. - Shelf Registration - A procedure that allows

firms to file one registration statement for

several issues of the same security. - Private Placement - Sale of securities to a

limited number of investors without a public

offering.

23

Rights Issue

- Rights Issue - Issue of securities offered only

to current stockholders. - Example - Lafarge Corp needs to raise

1.28billion of new equity. The market price is

60/sh. Lafarge decides to raise additional funds

via a 4 for 17 rights offer at 41 per share. If

we assume 100 subscription, what is the value of

each right?

24

Rights Issue

Example - Lafarge Corp needs to raise

1.28billion of new equity. The market price is

60/sh. Lafarge decides to raise additional funds

via a 4 for 17 rights offer at 41 per share. If

we assume 100 subscription, what is the value of

each right?

- Current Market Value 17 x 60 1,020

- Total Shares 17 4 21

- Amount of funds 1,020 (4x41) 1,184

- New Share Price (1,184) / 21 56.38

- Value of a Right 56.38 41 15.38

25

Rights Issue - example

- YRU Corp currently has 9 million shares

outstanding. The market price is 15/sh. YRU

decides to raise additional funds via a 1 for 3

rights offer at 12 per share. If we assume 100

subscription, what is the value of each right? - Current Market Value 9 mil x 15 135 mil

- Total Shares 9 mil 3 mil 12 mil

- Amount of new funds 3 mil x 12 36 mil

- New Share Price (136 36) / 12 14.25/sh

- Value of a Right 15 - 14.25 0.75

Recommended