RELIANCE CAPITAL LTD., - PowerPoint PPT Presentation

1 / 18

Title:

RELIANCE CAPITAL LTD.,

Description:

Company Outlook Reliance Capital (RCAP), a non banking financial company, is the financial service arm of the Anil Dhirubhai Ambani Group (ADAG) ... – PowerPoint PPT presentation

Number of Views:71

Avg rating:3.0/5.0

Title: RELIANCE CAPITAL LTD.,

1

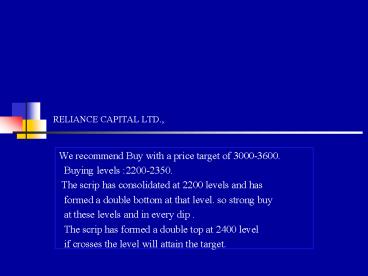

RELIANCE CAPITAL LTD.,

- We recommend Buy with a price target of

3000-3600. - Buying levels 2200-2350.

- The scrip has consolidated at 2200 levels and

has - formed a double bottom at that level. so strong

buy - at these levels and in every dip .

- The scrip has formed a double top at 2400 level

- if crosses the level will attain the target.

2

Company Outlook

- Reliance Capital (RCAP), a non banking financial

company, is the financial service arm of the Anil

Dhirubhai Ambani Group (ADAG) which has varied

interests in areas like telecom, energy,

entertainment. Reliance Capital is one of India's

leading and fastest growing private sector

financial services companies and ranks among the

top 3 private sector financial services and

banking companies, in terms of net worth. Through

the companys subsidiaries, it offers products

and services like mutual fund, life insurance and

general insurance. It has sizable private equity

and proprietary investments and is pursuing new

ventures like stock broking, consumer financing

and the asset recovery business as well. Reliance

Capital, initially focused on the asset

management business, has recently expanded its

presence in life insurance, general insurance

space and ebroking business as well. Reliance

Capital launched Reliance Money, a retail broking

and distributor of a range of financial service

products. It has a network of over 2,200 outlets

(Indias largest retail network by a non banking

financial services company). Reliance Capital has

100 economic interest in all the business units.

3

(No Transcript)

4

Valuation Summary

SECTOR OVERVIEW Indias recent economic growth

has been led by the dynamism of its services

sector particularly the high-end,

knowledge-intensive services. Service sector has

been consistently growing at a faster pace than

the economy since the liberalisation of the

economy took place in 1991. According to the

economic survey of 2007, the services sector

contributes to nearly 55 per cent of Indias

GDP. The financial sector consists of banking,

insurance, consumer finance, NBFCs. According to

Indian Brand Equity Foundation (IBEF), the

financial sector contributed around 5 of the

GDP in FY 2007. Indias banking and insurance

sectors have been significantly opened to private

sector since 1993 and 2000 respectively. With the

deregulation of the Mutual fund industry as well

in 1993, the sector has seen a spate of new

private and foreign players.

5

BANKING The scenario in the Indian banking

industry is changing rapidly. Traditionally, it

was characterised by poor performing public

sector banks which employed outdated practices

and technology. The liberalisation process

resulted in the number of private sector

scheduled commercial banks increasing to 61,

including 31 foreign banks. Private sector banks

had increased their share of total assets to 24.7

per cent and foreign banks to 6.6 per cent share.

By September 2004, the total number of foreign

bank branches in India was 217. The penetration

of banking services and products in rural India

is particularly low, with only 42 per cent of

rural households having bank accounts of which 21

per cent having access to credit from a formal

source and only one percent relying on a loan

from a financial intermediary. Improved access to

banking products would greatly benefit rural

businesses and households, and help to raise

living standards across the rural sector as a

whole.

6

INSURANCE Indias insurance sector, like its

banking system, has an important role to play in

enhancing financial intermediation, creating

liquidity and mobilising savings in the economy.

The opening of the life and non-life insurance

sectors to foreign investment in the year 2000

spurred increased activity by foreign investors.

In spite of the growing awareness of insurance

products, the penetration of the Industry is

abysmally low at 2.5 as compared to the matured

markets. This would augur well for the growth of

Insurance sector. In the life insurance sector,

there are currently 15 private insurers plus the

government-owned Life Insurance Corporation

(LIC). According to the Insurance Regulatory and

Development Authority (IRDA), first year (i.e.

new business) premium income of the private

insurers for 200607 was Rs 19, 500 Crs. In the

space of just six years from FY 2002, private

insurers have secured a 26 per cent share in new

business segment.

7

(No Transcript)

8

(No Transcript)

9

(No Transcript)

10

VALUATION

11

(No Transcript)

12

VALUATION

APE (Annualised Premium Equivalents) is sum of

FYP and 10 of Single Premium Valuation-NBAP

Multiple We believe that Reliance Life Insurance

will be among the top players in this segment by

year 2008 due to its reach and the growth rates

shown in the previous years. Its reach will help

to penetrate the under-penetrated markets. Due to

its focus on distribution and its rapid

scaling-up plans we believe the FYPs should grow

by 150 in FY08 and in the subsequent year a

growth rate of 85. Single Premiums should grow

by 60 in FY08 and 50 in FY09.The NBAP multiple

is expected to increase from 22 to 25 in FY09.

13

LIFE INSURANCE

Currently around 80 of the countries population

is without a life insurance policy. With the

economy booming, the disposable incomes are set

to increase which will increase the number of

policy holders dramatically. Life

insurance industry recorded a growth of 110 in

premium collection FY07. Reliance life

Insurance (RLI) is the fastest growing insurance

company in India with a market share of 4

amongst private insurers. The AUM is Rs. 12 bn.

It already has a reach of 217 branches and may

scale up to 400 by FY08 .Its agent force would

increase to nearly 2, 00,000 agents in FY 2008 up

from 1, 06,000 agents in FY 2007. Reliance Life

grew by 381 in FY07. Reliance expects its growth

from rural areas. It will need a capex of around

1200-1500 crs for this segment of the business.

Of the total premium earned, 88 is from ULIP

plans and 12 from others. This trend is likely

to be seen in the future years as well.

Currently banks are allowed to sell insurance

policies of only one Insurance Company. Banks

have a tie up with the insurance company for a

period of three years. Since Reliance Capital is

a late entrant in this business it does not have

a tie up with any of the banks to sell its

insurance products. However, it has the

opportunity to enter into contracts with banks as

and when they come up for renewal after a period

of every three years.

14

VALUATION

15

GENERAL INSURANCE

As per industry estimates penetration (as a

percentage of GDP) of general insurance in India

has improved marginally from 0.53 to 0.64 over

the 5 year period FY 2003-07. General insurance

industry in India has grown at 15 CAGR in the

past five years in terms of gross premium

collection. Given the low penetration of general

insurance and a CAGR of 22 , Reliance General

Insurance is expected to cash in on these

opportunities. Reliance General Insurance (RGI)

is the fastest growing general insurance company

and the 4th largest in India with a market share

of 10 amongst private general Insurers. In

FY07, the General Insurance business posted a

growth of 22, driven by private players

phenomenal growth of 60. Reliance General

Insurance has improved its retention ratio from a

35 in FY 06 to 55 in FY 07. The retail segment

accounts for 55 of Reliances General Insurance

business. There was a marked shift towards motor

insurance, which accounted for a whopping 50 of

all retail business. Reliance General Insurance

has expanded its distribution network to 85

branches and regional offices in FY 2007 from 34

branches and regional

16

GENERAL INSURANCE

17

BUSINESS UNIT VALUATION

18

Disclaimer This report has been

prepared solely for information purposes and the

information contained herein may not be deemed to

be an investment advice. Such information is

impersonal and not tailored to the investment

needs of any specific person. The information

contained herein is not a complete analysis of

every material fact representing any company,

industry or security. The views expressed may

change. While the information contained herein

has been obtained from sources believed to be

reliable, no responsibility (or liability) is

accepted for the accuracy of its contents.

Investors are advised to satisfy themselves

before making any investments and should consult

with and rely upon their own advisors whether and

how to use such information in making any

investment decision. Neither the author nor his

firm accepts any liability arising out of use of

the above information/ article. This report is

exclusively for the clients of Venkataraman Co.

only. VENKATARAMAN CO., Stock Share

Brokers, New No.2 (Old No.52) Dr. Ranga Road,

Mylapore, Chennai 600 004. Web www.venkataraman

.com E-mail vnkco_at_vsnl.com

Recommended

CrystalGraphics Presentations